| |

The Price of Fear

(July 18, 2007)

Clarification/Correction:

Perceptive reader Keimpe B. offered the following clarification/correction to yesterday's entry

on retail space per capita:

The graph of 'Square feet retail space per person' you're displaying

in your blog is misleading. The

numbers refer to Shopping Center Retail Space per person, not Total

Retail Space per person. If anything it shows that Europe is more

cozy, featuring many smaller stores.

I did a quick search and only turned up a 2005 white paper

that mentions on page 5 that U.S. total retail space is about 3 times

larger than English total retail space per capita (wow, still really

high, but more believable). You might want to ask for better numbers

from your readers.

Thank you, Keimpe, for drawing a distinction between shopping center space and retail space

that was lost on me. In my defense, I can only say that if you drove through Fresno it seems

entirely plausible that the U.S. does indeed have 7-10 times the retail space of our Western

confreres.

On to the critically important topics of the day, which were suggested by astute reader Bob K:

(emphasis added)

I saw yet another headline today about the new DJIA record high. I may not be phrasing this

adequately, but I hope you get my drift...I am fortunate enough to have some 401K and IRA

investments but these new record highs do nothing for my daily cash flow, i.e. the cost of

gasoline, milk and orange juice alone are negatively impacting my budget but this new record

today helps not at all. So why should I care about the new index records? And how many people

are really positively impacted 'now' by the new record, i.e. who sees any benefit today in their

checkbook?

And then another thought occurred to me... As I glean from your sight, particularly this week,

it ain't all rosy out there, and your readership knows that. I apologize for my ignorance, but

here is the question: "Who is the "they" that are causing the index to rise? And why is the

market rising?" My fear is that all of this focus on the stock market, and the resultant

subliminal message to 'buy - buy - buy because the DJIA hit a new high' has absolutely nothing

to do with my daily economic reality.

I hate to sound like a conspiracy theorist, but are

'they' ignoring all the issues such as you have pointed out this week just to jack up the DJIA

and therefore 'they' must be benefiting from this run up somehow?....although it seems to me

like it is all a house of cards.

Excellent observations and questions, Bob. To start, let's put the Dow's "new high" in

perspective.

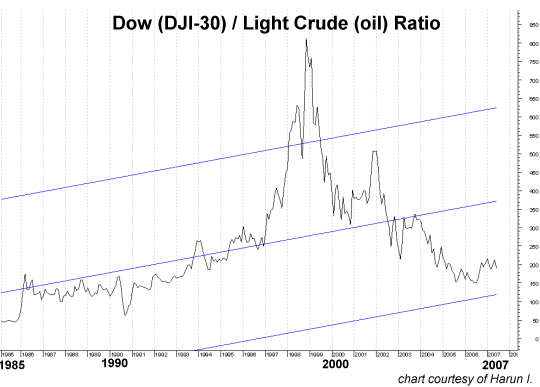

Frequent contributor Harun I. submitted a chart of the correlation between the Dow Jones

Industrial Average (DJI-30) and oil (light crude). The high spike at the market's 2000 top

means that a share of the DJI bought a great amount of oil. The low mark in 1985 meant that a share

of the DJI bought very little oil.

As you can see, the current "new high in the DJI" buys

far less of the most essential industrial commodity than it did in 2000.

By this measure--in terms of a tangible non-discretionary commodity, oil--the Dow's "new high" is

singularly unimpressive.

As for manipulation: knowledgeable reader David M. contributed an insider's understanding

of the incredibly shaky foundations of the CDO market. (emphasis added)

I used to be a programmer for one of the mega-investment banks - its a

household name, top 3 or 4. I did some work for the business unit

controllers (similar to accountants) for the CDS (credit default swaps)

at the company. This was 3 or 4 years ago and the business in CDS

trading was growing like crazy.

One of the controller's jobs was to

carefully watch the traders and that included marking (independently

pricing) their positions periodically, which was extremely difficult to

do. Unlike stocks and bonds, there is no public market for these

securities and no reliable service to mark the value of the securities.

For stocks and bonds, there are the public markets and services such as

Reuters and Bloomberg, which collect price information about stock and

bond prices and distribute it to subscribers.

The CDS market is illiquid and not public and the controllers at this

company subscribed to a service which provided CDS marks, but they were

extremely unreliable. Why? Because the CDS traders at the firm knew

the people that ran the CDS marking service! And I'll quote the

controllers: "they went out for beers together after work". In other

words, the marking service was getting their marks from our firm's

traders!

To summarize, the firm couldn't even confidently mark their own

positions in CDS. So it is impossible for anyone else that bought these

securities to reliably know their value. As a result, you will now

better understand the derivatives crack-up when it occurs.

In other words: the guys selling the CDS to unwary clients are telling

the guys who are supposedly establishing the value (mark to market) "objectively" what the

derivative is worth. Talk about the fox guarding the chicken coop. If this isn't

an informal conspiracy to defraud the unwary investors buying highly risky securities, then what

is?

So when the MSFM (mainstream financial media) trumpets the "free market" and derides

"conspiracy theories", feel free to gag, shred the paper or throw something at the TV.

The MSFM is in fact part of the conspiracy, for their glib assurances are part and parcel

of maintaining the illusions and lies at the very foundation of the CDS/CDO markets.

As to why would anyone join in such a deception--look no further than the record profits being

booked by Morgan Stanley, Merrill Lynch et. al. The fees being generated by cooking up and

selling CDOs and other derivatives are immense, in the tens of billions of dollars annually.

That's a powerful incentive to keep the game fixed and running. It's 3-card monte on a

trillion-dollar scale.

Correspondent/blogger

Fred Roper sent over a comment

by Winston Munn on the

Big Picture blog which suggests the "marks" (unwary investors) are

getting wise to the scam:

Underwriters are affected already, having to pony up for some of the riskier corporate bonds

no one is willing to buy.

"Those looking to raise money to finance the recent private-equity deals are getting a front-row

view of the turbulence. Just months ago, there were more than enough eager buyers of the bonds

and loans sold to support highly leveraged takeovers. But now investors are pushing back,

demanding higher rates and protections from risk.

In some cases, investors are asking for so much that the bond offerings never even make it to

market. ServiceMaster Co.'s underwriters called off a $1.15 billion sale of junk bonds earlier

this month after investors balked at provisions in the bonds that would have let the company

cover some of its interest expense by issuing more debt.

That forced the lawn-care and pest-control company to obtain a bridge loan directly from the

underwriters. A $2.85 billion loan issue still needs to get done as part of the $5.5 billion

takeover by private-equity firm Clayton, Dubilier & Rice and others, according to KDP Investment

Advisors Inc."

When the marks (institutional investors) stop buying, the merry-go-round abruptly stops.

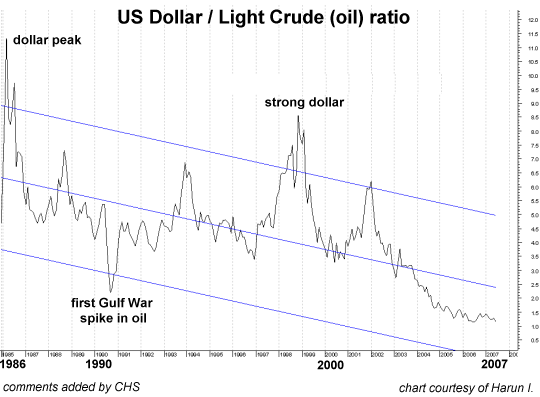

Harun also sent in a chart of the dollar/oil ratio, which reveals that in terms of purchasing

power, oil is far more expensive than it was at the (inflation-adjusted) nominal high in 1990.

Harun's commentary suggests another reason for the large-scale manipulation which is pushing the

stock market to nominal highs, even as the purchasing power of our currency (the dollar)

is plummeting to new lows: the great, abiding fear of our current political leadership and their

financial cronies that the

3-card monte fraud will blow up before they leave office. (emphasis added)

In 1998 it was thought that LTCM would bring the world financial system down due to a liquidity

crisis. But we have forgotten the lessons. LTCM thought it was well diversified against the risk

to which it was exposed, and in a normal market they were essentially correct.

What their models

couldn’t handle was the fact that during a crisis uncorrelated issues become perfectly correlated,

and so they watched all of their positions move against them during the Russian default as

everyone panicked. The last sentence of the above quote is simply the lesson LTCM taught us, a

lesson we will soon revisit.

The more I read and study, the more I am becoming convinced that hedge funds are effects and the

causality lies with fractional reserve banking and a fiat monetary system. Debt must be expanded

or the system implodes, but the growth in debt is not linear, it has to be exponential and

therefore is inherently unstable.

The efforts to maintain the appearance of stability are

unequivocally criminal. There is but a small number of people focusing on this but when things

go critical there may be greater focus by larger numbers (a central bankers worst nightmare).

For example, how is it that during the greatest bull market in our history the dollar has been

in a 22-year Bear market relative to Light Sweet Crude Oil? This is not a supply/demand issue

because prices of crude stayed in a relatively narrow band during this time up until 1999 (see

attached chart). The dollar has been losing its value but apparently few are interested as to

the “why”.

We had better awaken because implicitly, the dollar will go to zero. Personally, I speculate

there is a quiet panic going on at high levels of government. Panics arise when people are

fearful and don’t know what to do. I would also speculate that the current administration has

put the word out to not let things blow up on their watch, which means if the Democrats win,

they will get the blame.

One thing that bothers me terribly is that hedge funds are private placement, only the wealthy

“sophisticated” investor can participate. This regulation is required by law. Our government

feels that only the wealthy are smart enough to understand the risks involved in these funds

and because of their wealth can sustain a substantial or complete loss of their invested capital.

The general public cannot partake, but in a crisis it is the unsophisticated, not-so-wealthy

taxpayer that provides the relief needed to save the ‘system’. This (bailouts) runs contradictory

as to why the funds are regulated to wealthy investors.

This parasitic subsidization of the wealth's failed financial adventures by the middle class and

poor has not caused social unrest yet and perhaps never will but nevertheless it should cease

because in reality it results in a forced transfer of wealth (stealing?) from the middle class

and poor to the wealthy. The “Greenspan put” should be called the “taxpayer put”. If our financial

system can be destroyed by a few large firms then we must question who is really in control of

this systems, the government or banks and financiers?

Well said, Harun. Thank you, Keimpe, Bob, David, Fred and Harun for enlightening us all.

For more on this subject and a wide array of other topics, please visit

my weblog.

copyright © 2007 Charles Hugh Smith. All rights reserved in all media.

I would be honored if you linked this wEssay to your site, or printed a copy for your own use.

|

|