What Will End the 34-Year US Treasury Bond Bull Market?

March 26, 2015

I see #1 and #4 as the most likely triggers of a rise in Treasury yields.

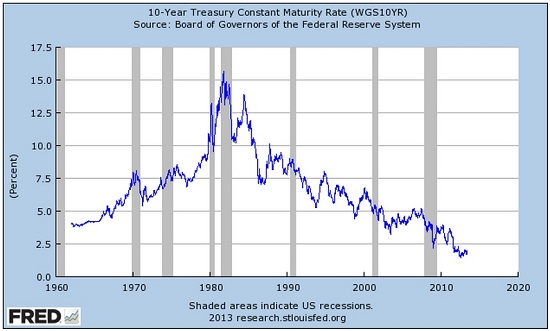

U.S. Treasury bonds (10-year and 30-year) topped out above 15% in late 1981, and have traced a sawtooth pattern down ever since. The 10-year bond now yields 1.92% and the 30-year yields 2.51%.

Daily Treasury Yield Curve Rates.

Correspondent Mark G. recently asked a question that is on many minds: what might finally produce an end to the 34-year US Treasury Bond bull market? Here is Mark's commentary on the question:

10 Year T-Bond interest rates are falling again after a minor rally. This leaves me pondering a nearly 20-year old question: what might finally produce an end to the 34-year US Treasury Bond bull market? Neither the beginning or end of three different US QE programs, plus Japanese and ECB QE programs, have served to do this. Nor did oil price booms to $140/bbl, or price crashes to $42/bbl WTI with threats of further decline. Or any other commodity or possible index of commodities. Various FOREX levels so far have also been only correlated over the very shortest of terms. Stock market bull bubbles and bear crashes have also come and gone without lasting effect. War, peace, Cold War, Cold Peace ditto.

My background education and experience says that before this T-Bond bull market can end the US T-Bond sellers will have to routinely overwhelm the buyers.

As Mark observed, the price of bonds (along with all other securities) is established by supply and demand. For prices of any financial security to fall, sellers have to routinely overwhelm buyers.

Demand is one factor; supply is the other. If the security is scarce, then even modest demand can push the price up. If the security is in surplus, demand can be overwhelmed by supply.

So the only way that the yield on Treasuries (or any other security) can rise is if supply overwhelms demand. If there are no buyers of bonds at a low price, the yield must rise to entice buyers to part with their cash.

If demand soaks up the initial issuance but more issuance hits the market, the yield will rise as demand for more bonds simply isn't present at low yields.

The central banks have manipulated the market for sovereign bonds by creating new money out of thin air and buying bonds. The goal is to suppress interest rates. And since central banks can create as much money as they want, whenever they want, there is no limit to how many bonds they can buy.

Rising yields once acted as a limiting factor on governments' issuing more bonds to fund their fiscal deficits. But since central banks have created trillions of dollars out of thin air to buy as many bonds as the Treasury issues, rates can be suppressed for as long as central banks are free to create trillions out of thin air.

If we put these dynamics together, we can sketch out a few possible conditions that would have to be met for U.S. Treasury yield to rise:

1. The Federal Reserve (the central bank of the U.S.) would have to be restrained from printing money to buy Treasuries. This could be informal political constraints (i.e. widespread public distrust of the Fed based on its role in exacerbating wealth inequality) or it could be the Federal Reserve's charter and powers are limited by acts of a Congress that is hostile to its counter-productive money-printing and financial repression.

2. The supply (issuance) of new bonds rises to levels that overwhelm demand. Were the U.S. government to run enormous deficits, the supply might well overwhelm demand, especially if the Fed were no longer free to print up another $3 trillion to buy bonds.

3. Other sovereign-debt markets that are currently being sold in favor of U,S. Treasuries would have to become more attractive in yield, liquidity and safety than Treasuries. Right now, oligarchs around the world have already suffered losses of 15% to 25% on their wealth not held in U.S. dollars.

The rush to sell other currencies and assets to buy dollars and Treasuries has enabled the Fed to end its quantitative easing/bond buying programs; the demand from overseas buyers has been strong enough to push yields down to historic lows, even without any Fed purchases.

This trend would have to reverse for Treasuries to be sold in favor of some other sovereign bonds.

4. The phantom wealth in risk-on assets would have to dissolve on a global scale, forcing owners of unleveraged assets such as Treasuries to dump their Treasuries en masse to raise cash to pay down U.S.-denominated debt and to to fund their lavish lifestyles.

Once the markets for yachts, super-sports cars, etc., dry up, these assets go bidless: nobody wants a costly-to-maintain yacht or super-car at any price. Real estate may retain more of its value than oligarch toys, but real estate is famously illiquid; the margin call must be paid in days, and finding a buyer for luxe real estate takes longer than days.

That leaves precious metals and the amazingly liquid Treasury bonds as assets that can be sold in a hurry to cover debts being called due to the collapse of risk-on bubbles in equities, junk bonds, real estate, art, yachts, super-cars, etc.

I see #1 and #4 as the most likely triggers of a rise in Treasury yields. The collapse of phantom-wealth bubbles could occur in the next year or two, or be delayed for another 5 to 6 years. But the implosion of phantom-wealth bubbles is assured by the internal dynamics of bubbles.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Steve W. ($50), for your superbly generous contribution to this site-- I am greatly honored by your steadfast support and readership. |