If You Don't See Any Risk, Ask Who Will "Buy the Dip" in a Freefall?

April 17, 2021

Nobody thinks a euphoric rally could ever go bidless, but as Greenspan belatedly admitted,

liquidity is not guaranteed.

The current market melt-up is taken as nearly risk-free because the Fed has our back,

i.e. the Federal Reserve will intervene long before any market decline does any damage.

It's assumed the Fed or its proxies, i.e. the Plunge Protection Team, will be the buyer in any

freefall sell-off: no matter how many punters are selling, the PPT will keep buying

with its presumably unlimited billions.

If this looks risk-free, ask who else will be "buying the dip" in a freefall? Former Fed Chair

Alan Greenspan answered this question in his post-2008 crash essay

Never Saw It Coming: Why the Financial Crisis Took Economists By Surprise (Dec. 2013 Foreign

Affairs):

"They (financial firms) failed to recognize that market liquidity is largely a function of the degree of investors'

risk aversion, the most dominant animal spirit that drives financial markets.

But when fear-induced market retrenchment set in, that liquidity disappeared overnight, as buyers

pulled back. In fact, in many markets, at the height of the crisis of 2008, bids virtually disappeared."

For the uninitiated, bids are the price offered to buyers of stocks and ETFs and

the ask is the price offered to sellers. When bids virtually disappear, this means

buyers have vanished: everyone willing to buy on the way down (known as

catching the falling knife) has already bought and been crushed with losses, and so there's

nobody left (and no trading bots, either) to buy.

When buyers vanish, the market goes bidless, meaning when you enter your "sell" order

at a specific price (limit order), there's nobody willing to buy your shares at the current price.

The shares remains yours all the way down.

If you decide to just get out at any price and place a market order (sell at whatever the bid is

offered), your $100 per share stock might sell for $5 a share. This is known as a flash crash,

and astute punters have observed that these are becoming more common.

When markets go bidless, the predictable order flow of low-volume days goes out the window.

On a typical low volume day (and all days are low volume recently), the spread between bid and

ask is modest in heavily traded issues and sellers can be confident their sell order will execute

in a few seconds. In a freefall sell-off, sell orders pile up and the bid plummets to levels that

were considered "impossible" in low-volume days.

What Greenspan didn't discuss is the trading bots that do most of the trading

have been programmed to be risk averse. In a real sell-off, why catch the falling

knife by hitting the bid on the way down? That's a guaranteed way to either lose money

or ending up a bagholder.

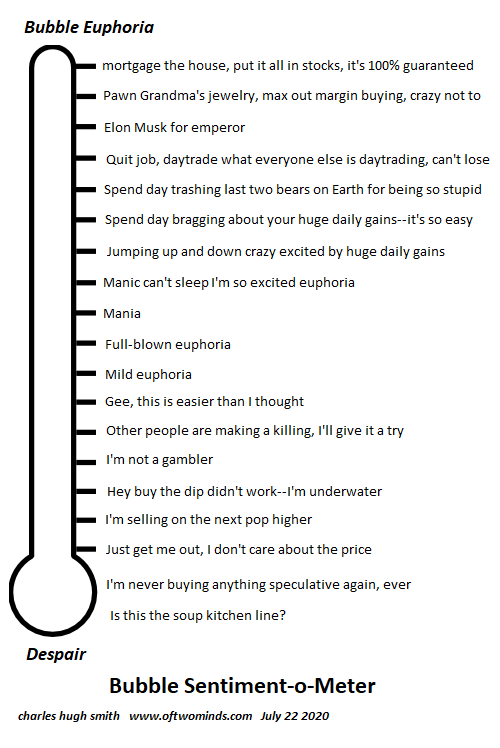

Humans have a default setting for risk aversion: it's called panic. Once the euphoric

comnfidence that the Fed will never allow the market to fall by more than a few percentage points

is broken, it's not replaced by rational risk assessment; it's replaced by full-blown just-get-me-out

panic.

The Plunge Protection Team works just fine on low-volume days, but it fails when a tsunami of

selling washes away the bid. Though few seemed to notice, massive selling volume begets more

selling as the bots' risk aversion kicks in.

Ironically, the mass migration of retail punters into the market has introduced a heightened

potential for panic selling. The wild swings in Gamestock (GME) earlier in the year were

a sneak preview of what can happen as panicked newbies enter market sell orders.

Euphoric punters forget that many of the players are leveraged, meaning that they're using

borrowed money (margin debt) to buy more stocks. Should the market drop instead of rebounding,

their account will fall below minimum requirements and they will have to add cash or sell stocks.

When buy the dip fails, those with margin calls add to the selling.

Other limits can manifest in cryptocurrency trading. When most trades are buys, few notice

the fine print on exchange sell orders in crypto wallets and exchanges. Prices may be guaranteed

for a limited time (for example, 10 minutes), and there may not be an option for limit orders.

If the order doesn't execute before the time limit expires, then the order to sell executes at

whatever bid is offered.

There's also no guarantee that your sell order will execute in a timely manner. A reader

recently sent me a screenshot of an exchange of a top 100 (by market cap) cryptocurrency for Bitcoin

that took almost 2 hours to execute. (The reader passed on using the Lightning Network after reading the

disclosures.)

Exchanges may limit the number of coins per exchange. In other words, the implicit assumption

that punters can unload their entire position at the current bid may prove unfounded in heavy sell volume

days.

The point here is bottlenecks can emerge in heavy sell volume days that traders did not

anticipate. The possibility that markets, brokerage platforms and exchanges could break

and simply cease to function isn't on anyone's radar, despite various bits of evidence that

a breakdown isn't as farfetched as punters currently assume.

Ten minutes is more than enough time for supreme, euphoric confidence to crumble into panic,

and trading bots can pull their buy orders in 10 milliseconds.

This is why the big players distribute their shares to overly confident retail punters

over many weeks. Big players know there is no way they can dump their entire position without

crushing the bid, so they sell in bits and pieces all the way up the euphoric melt-up.

The issue isn't just the price you get when you sell--it's being able to get out of your position

at all. A strange phenomenon occurs in freefall sell-offs: the exit door (i.e. the liquidity

that allows you to liquidate your entire position at the current bid) suddenly shrinks from

a barndoor to a mouse-sized hole in the baseboard.

Nobody thinks a euphoric rally could ever go bidless, but as Greenspan belatedly admitted,

liquidity is not guaranteed. In a real tsunami of trading-bot selling, the

Plunge Protection Team's card table is no match for the sea of selling.

Risk aversion can go from zero to 200 faster than overconfident punters believe possible.

If you found value in this content, please join me in seeking solutions by

becoming

a $1/month patron of my work via patreon.com.

My new book is available!

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet

20% and 15% discounts (Kindle $7, print $17,

audiobook now available $17.46)

Read excerpts of the book for free (PDF).

The Story Behind the Book and the Introduction.

Recent Podcasts:

AxisOfEasy Salon 41: Can't get you out of my head (58 min)

Disconnects between the Economy and the Financial Markets (FRA Roundtable, 41 min)

My COVID-19 Pandemic Posts

My recent books:

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet

(Kindle $8.95, print $20,

audiobook $17.46)

Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook)

Read the first section for free (PDF).

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic

($5 (Kindle), $10 (print), (

audiobook):

Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake

$1.29 (Kindle), $8.95 (print);

read the first chapters

for free (PDF)

Money and Work Unchained $6.95 (Kindle), $15 (print)

Read the first section for free (PDF).

Become

a $1/month patron of my work via patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Mark S. ($5/month), for your monstrously generous pledge to this site -- I am greatly honored by your support and readership. |

Thank you, Alan S. ($5/month), for your magnificently generous pledge to this site -- I am greatly honored by your support and readership. |

|