Oil, Inflation and Recession

April 6, 2026

It's not the price of oil per se that triggers recession, it's the underlying vulnerabilities that have been cloaked with happy story narratives to keep the game going.

Thank you, Smooth Ryda ($70), for your monumentally generous subscription

to this site -- I am greatly honored by your support and readership.

Thank you, Benjamin B. ($7/month), for your marvelously generous subscription

to this site -- I am greatly honored by your support and readership.

Thank you, David C. ($7/month) for your superbly generous subscription

to this site -- I am greatly honored by your support and readership.

Thank you, Anthony R. ($3/month) for your most generous subscription

to this site -- I am greatly honored by your support and readership.

Recessions don't require a spike in the price of oil/gasoline, but spikes in energy prices trigger recessions.

This makes sense, as hydrocarbons are the foundation of every industry, from the so-called "green" industries to all the high-tech industries (SpaceX, AI data centers etc.) to transport, plastics and everything else.

Recessions have other causes, of course: the business cycle of over-indebtedness and speculative excesses leading to defaults and the contraction of credit and spending, the collapse of speculative asset bubbles, the inflationary spiral of overborrowing to fund "guns and butter," and disruptive events such as plagues and wars.

Inflation reduces discretionary income as a larger share of earnings must be devoted to essentials. In a consumer economy, this reduction of discretionary income leads to households borrowing more to fill the widening gap between what they reckon is their rightful lifestyle and the purchasing power of their earnings.

This increase in debt leads to a higher percentage of net earnings being devoted to interest and principal, further reducing discretionary income. The eventual retrenchment--reducing debt by reducing spending and default--leads to a contraction in consumption, i.e. recession.

Recessions occur when a happy story about the economy that doesn't reflect reality encounters reality. Before recessions, the happy story is always the same: corporate profits are solid and rising, consumer spending is rock-solid, employment is strong, unemployment is low, the household balance sheet is healthy, technology is increasing productivity, and so on.

According to the happy story, a recession is impossible, so borrow and buy, buy, buy--stocks, houses, experiences, cruises, buy it all because the good times are permanent.

The vulnerabilities generated by over-reliance on borrowing to fund spending and the corrosive effects of inflation are buried beneath statistical trickery: add all the wealthy households to the mix and then take the average, and voila: look how rich the average household is. All is well, borrow and buy to your heart's content. Mix in hedonic adjustments and pixie-dust and voila, 8% inflation is magically reduced to 2.5%.

The suspension of disbelief / confidence is the magic of the happy story narrative. As long as people are complacent and confident, they act on the belief that their income and wealth will continue rising, enabling more borrowing and spending.

That this is not necessarily in their best interests in the long term is what must be hidden, lest they curtail borrowing and spending because the whole point of the economy is to maximize profits and this is only possible if people who don't earn enough money to spend freely borrow to spend freely.

This is where the other magic in the happy story becomes essential: the wealth effect generated by credit-asset bubbles. If people see their house and stock portfolios rising in value, they feel wealthier and are more confident in borrowing and spending because they have this wealth piling up in the background.

It's like a savings account that increases without the sacrifice of deferring consumption: in credit-asset bubbles, we get to have our cake and eat it, too.

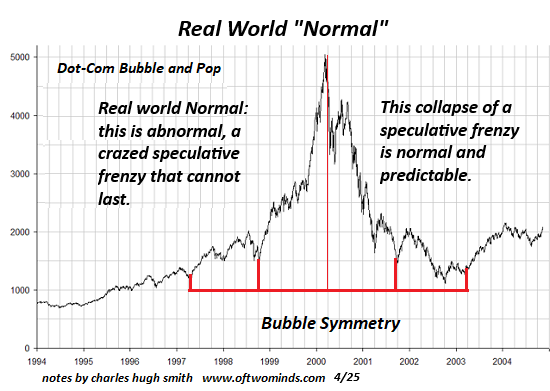

The problem that must be hidden by the happy story is that excessive debt and speculation are self-liquidating: the machinery that makes them work self-destructs by its very nature. Debt accrues interest which reduces discretionary income which sets up contraction of credit and consumption, and all credit-asset bubbles pop, regardless of the intensity of the propaganda / happy story that this isn't a bubble, it's "capitalism" or "technology" or "animal spirits."

It's not a specific price point or metric that causes recession: it's the decay of confidence and discretionary income that leads to recession. Confidence is fragile by its very nature. We've been selected to be wary of surplus suddenly becoming scarcity, and rising prices of energy cascading through the entire economy activates a reappraisal of our complacent confidence.

Every business is hammered by rising costs for literally everything they buy to operate, and since the discretionary income of the bottom 80% is already under pressure, they can't raise prices much without losing sales.

Households feel the pinch of rising utilities and fuel immediately, and for both enterprises and households, confidence in the future is at risk of eroding like a sand castle in a rising tide.

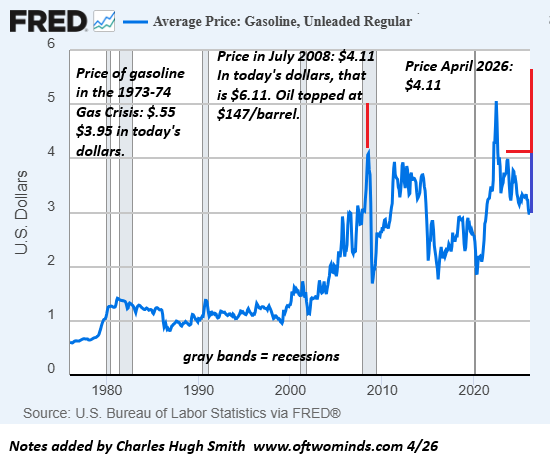

Here is a chart of the average price of gasoline in the US from 1976 to February 2026. I've added the recent spike to the current average price of $4.11 / gallon. Interestingly, this is pretty close to the inflation-adjusted price of gasoline in the 1973-74 Gas Crisis, and the nominal price in July 2008. Adjusted for inflation, $4.11 in July 2008 is $6.11 in today's dollars.

The point I want to make here is that there is no price trigger for recession, as it depends on the underlying fragilities and vulnerabilities of the economy. Put another way, it depends on the width of the gap between the happy story narrative intended to keep confidence and complacency high and the realities of higher costs and rising debt service reducing discretionary income.

Credit-asset bubbles pop for many reasons, but what we experience is a collapse of confidence that the bubble will continue inflating, making us richer every day, in every way. The core fragility of today's economy is the expansion of consumption now depends on the spending of the top 10%, who just so happen to own the lion's share of income-producing assets such as real estate, stocks, corporate bonds and enterprises.

Once the Everything Bubble pops, the confidence of the top earners and spenders will collapse, leading to a decline in their borrowing and spending.

Oil doesn't need to hit $147/barrel and gasoline doesn't need to reach $6/gallon to trigger a recession. (Gasoline is over $6/gallon in California and over $5/gallon in states with high fuel taxes.) There is no specific price-point, any more than there is some specific metric that enables us to predict an avalanche. It all depends on the underlying vulnerabilities and excesses of the economy at that moment in time.

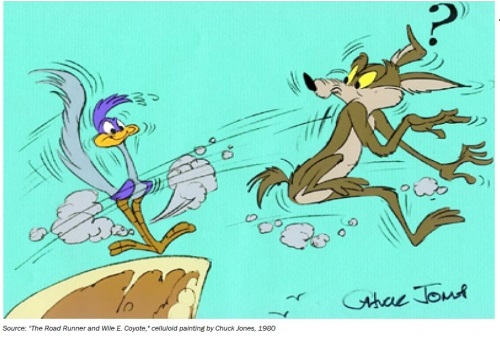

When he's confident, Wile can walk on air. It's when he suddenly discerns reality that his confidence vanishes. Recessions always catch conventional economists by surprise because the collapse of confidence triggers a sudden rise in unemployment and defaults and a sharp decline of credit and spending.

It's not the price of oil per se that causes a recession, it's the underlying vulnerabilities that have been cloaked with happy story narratives to keep the game going.

New Podcast:

Self-Liquidating Systems, Parallel Worlds, and AI Doesn't Live In A Moral Universe (Leafbox)

Apple podcast

My book Investing In Revolution is available at a 10% discount ($18 for the paperback, $24 for the hardcover and $8.95 for the ebook edition).

Introduction (free)

Check out my updated Books and Films.

Become

a $3/month patron of my work via patreon.com

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email

remain confidential and will not be given to any other individual, company or agency.