Three Crazy Things We Now Accept as "Normal"

February 9, 2018

How can central banks "retrain" participants while maintaining their extreme policies of stimulus?

Human habituate very easily to new circumstances, even extreme ones. What we accept as "normal" now may have been considered bizarre, extreme or unstable a few short years ago.

Three economic examples come to mind:

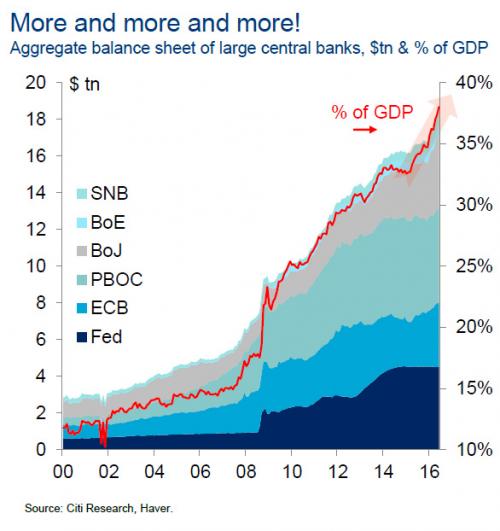

1. Near-zero interest rates. If someone had announced to a room of economists and financial journalists in 2006 that interest rates would be near-zero for the foreseeable future, few would have considered it possible or healthy. Yet now the Federal Reserve and other central banks have kept interest rates/bond yields near-zero for almost nine years.

The Fed has raised rates a mere .75% in three cautious baby-steps, clearly fearful of collapsing the "recovery."

What would happen if mortgages returned to their previously "normal" level around 7% from the current 4%? What would happen to auto sales if people with average credit had to pay more than 0% or 1% for a auto loan?

Those in charge of setting rates and yields are clearly fearful that "normalized" interest rates would kill the recovery and the stock bubble.

2. Massive money-creation hasn't generated inflation. In classic economics, massive money-printing (injecting trillions of dollars, yuan, yen and euros into the financial system) would be expected to spark inflation.

As many of us have observed, "official" inflation of less than 2% does not align with "real-world" inflation in big-ticket items such as rent, healthcare and college tuition/fees. A more realistic inflation rate is 7%-8% annually, especially in the higher-cost regions of the US.

But setting that aside, there is a puzzling asymmetry between low official inflation and the unprecedented expansion of money supply, debt and monetary stimulus (credit and liquidity). To date, most of this new money appears to be inflating assets rather than the real world. But can this asymmetry continue for another 9 years?

3. Stock markets are soaring but sales and profits are stagnant. Everyone knows central banks are still pumping billions of dollars per month into the financial system, and this (coupled with central bank purchases of stocks and bonds) has been pushing stocks sharply higher for the past 9 years, with only a few hiccups along the way.

This is pushing valuations out of alignment with traditional metrics of valuing assets such as sales and profits--a process known as "price discovery." In essence, traders and investors have habituated to central banks driving private-sector markets higher, not because the assets are generating more value or profits. but simply as a function of centralized money creation and asset purchases.

All of these extremes generate mal-investment, diminishing returns and perverse incentives for ramping up unproductive and risky speculation, leverage and debt. Yet the central banks have trapped themselves in this risky trajectory because they've pushed the accelerator to the floorboard for 9 years. Any extreme held in place for 9 years has long slipped from "temporary" to permanent.

Participants have now habituated fully to central banks extreme stimulus of financial markets, and in a sense they've forgotten how to price assets based on real-world private-sector measures.

How can central banks "retrain" participants while maintaining their extreme policies of stimulus? The only possible answer is: they can't.

This essay was drawn from Musings Report 2018:1. The Musings Reports are emailed weekl to constributors, subscribers and patrons.

Than you for your financial support of my work.

My new book

Money and Work Unchained is $9.95 for the Kindle ebook and $20 for the print edition.

Read the first section for free in PDF format.

If you found value in this content, please join me in seeking solutions by

becoming

a $1/month patron of my work via patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Sam F. ($50), for your extremely generous contribution to this site -- I am greatly honored by your steadfast support and readership. |

Thank you, Tony K. ($50), for your marvelously generous contribution to this site -- I am greatly honored by your support and readership. |

|