The Global Problem: Monetary Policy Can't Fix an Economy's Structural Problems

March 5, 2015

When we look back from 2025, it will be painfully obvious that central bank policies exacerbated the systemic crises that brought down the global financialization machine.

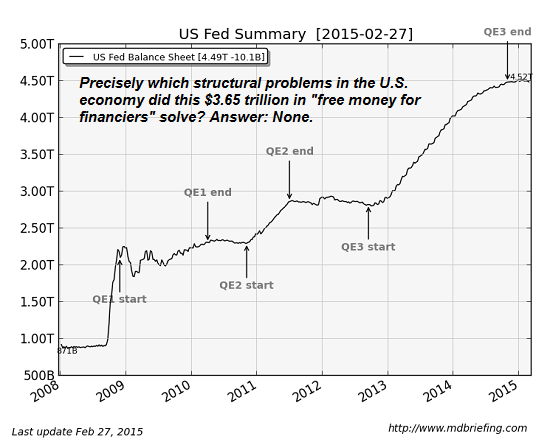

What with all the praise being heaped on central banks for "saving" the world from economic doomsday in 2008, it's only natural to ask which structural problems their unprecedented policies solved in the past 6 years. After all, "saving" the world from financial collapse was relatively quick work; so what problems beyond imminent implosion did the central banks policies solve in the past 6 years?

Answer: none. zip, zero, nada. The truth is central bank policies of zero-interest rates and free money for financiers have made many structural problems worse.

Did central bank policies resolve the structural problem of unfunded pension and retiree healthcare liabilities? No, they made it worse, as zero-interest rates have reduced the yields on pension funds, 401Ks and IRAs to mere pittances. This destruction of safe yields has driven pension funds into risky investments in junk bonds and stocks, leaving them vulnerable to devastating losses when the current credit bubble bursts.

Did central bank policies resolve the structural problem of corporate wealth buying political influence? No, they made it worse, by encouraging corporations to borrow vast sums to use on whatever they fancied--for example, lobbying and share buybacks.

Did central bank policies resolve the structural problem of rising dependence on credit for weak "growth"? No, they made it worse, as cheap money enabled the re-emergence of subprime loans to marginal borrowers. The deterioration of credit quality guarantees a credit crisis and bubble pop as marginal borrowers default.

Did central bank policies resolve the structural problem of low investment in new assets that boost productivity, enabling widespread advances in wealth? No, they made it worse, as near-zero interest rates for financiers and corporations and limitless liquidity have incentivized debt-based speculation and highly leveraged bets on completely unproductive projects such as share buybacks, which boost the value of corporate insiders' stock options while producing no new goods or services.

Did central bank policies resolve the structural problem of rising wealth/income inequality? No, they made it worse, by boosting the value of assets owned by the super-wealthy .01% and to a lesser degree, the top 5%.

Did central bank policies resolve the structural problem of moral hazard, the separation of financial risk from consequence? No, they made it worse, as monetary policies were designed not to help Main Street but to recapitalize Wall Street banks by diverting tens of billions of dollars that were once paid in interest to depositors straight into the banks' coffers.

Nothing has changed: private banks are free to make risky bets, knowing that if the bets go sour the state or central bank will make good their losses.

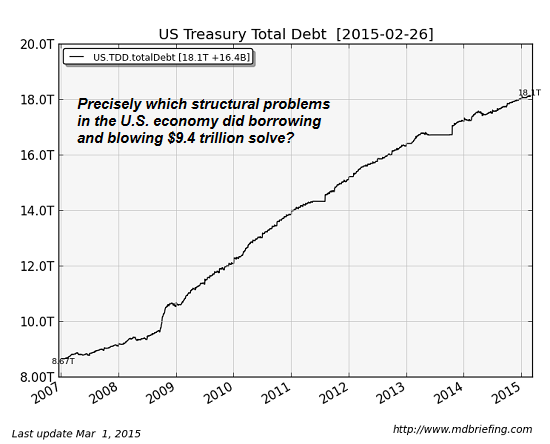

Did central bank policies resolve the structural problem of sovereign debt, i.e. central states overborrowing and saddling future generations with crushing debt loads? No, they made it worse, as zero-interest rate policies have enabled central states to borrow gargantuan sums without the interest due on the debt squeezing out other spending.

When credit is nearly free, there's no need to make hard choices or face the costs of systemic corruption, waste, fraud, cronyism and inefficiency; just borrow another trillion dollars, yen, euros or yuan to prop up parasitic elites and vested interests.

When we look back from 2025, it will be painfully obvious that central bank policies exacerbated the systemic crises that brought down the global financialization machine. Extend and pretend only increases the power and amplitude of the crises that will eventually burst forth from the monetary dysfunctions and distortions that are currently praised as financial genius.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Helen S.C. ($10), for your gloriously generous contribution to this site-- I am greatly honored by your steadfast support and readership. |