|

|

| weblog/wEssays archives | home | |

|

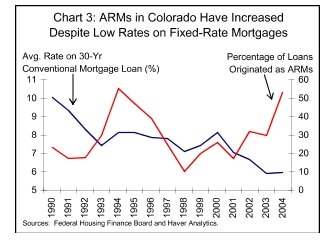

What About All Those Fixed-Rate Mortgages at Low Interest Rates? (August 14, 2006) What about all the people who didn't re-finance to the hilt or buy a home with an adjustable rate mortgage? What about those who secured low-interest fixed-rate mortgages? The housing bubble's demise will have no effect on them, so what's the big deal? Good point. At first glance, it would seem that the millions of homeowners who never re-financed at all, or who did so only to lower their interest rate with a fixed-rate loan, not pull equity out of their house, are utterly immune to the debilitating effects of the decline in current housing values. But beneath this apparently benign surface lies two forces which will affect homeowners, even those with fixed-rate mortgages: property taxes and a declining economy.

As you can see from this chart, significant property tax increases are being logged practically across the board. Those living in states with with "Prop 13" limits (like California) on how much existing property taxes can rise are protected, but some 35 states have no such limits on increases. And while I haven't found any statistics on this, it is fair to assume that waves of new county assessor's appraisals are washing over the land every month, raising property taxes to recent bubblicious valuations.  Here is a chart of an economy teetering on the edge of deep recession. Even if tens

of millions of prudent homeowners retained their fixed-rate mortgages and equity, millions

of other more desperate, profligate or deluded homeowners bought or re-financed with

adjustable rate mortgages which are already re-setting at much higher rates.

Here is a chart of an economy teetering on the edge of deep recession. Even if tens

of millions of prudent homeowners retained their fixed-rate mortgages and equity, millions

of other more desperate, profligate or deluded homeowners bought or re-financed with

adjustable rate mortgages which are already re-setting at much higher rates.

Buried within the many flavors of "exotic" loans lie uncounted quagmires. One of our friends bought a house a few years ago on a fixed-rate (good) interest-only (not good) loan. When the interest-only period expires in a year or so, then the payment jumps up not just to start paying the principle, but a little extra to cover all that principle which accrued during the interest-only "free ride" period. The jump in payments will be truly staggering to anyone on a tight budget or non-yuppie income.  And as everyone knows, the stalling out or decline of real estate values has effectively

ended the re-finance gravy train. How many homeowners with the desire or need to pull

equity out of their homes have not already done so? And of those with the need, how many

have any equity left to draw out? Judging by the rapid fall-off in re-finance mortgage

applications, not many.

And as everyone knows, the stalling out or decline of real estate values has effectively

ended the re-finance gravy train. How many homeowners with the desire or need to pull

equity out of their homes have not already done so? And of those with the need, how many

have any equity left to draw out? Judging by the rapid fall-off in re-finance mortgage

applications, not many.

Bottom line: as all these millions of interest-only and adjustable-rate mortgages re-set to much higher payments, millions of homeowners will have less to spend in the great consumer economy which accounts for 70% of the entire U.S. economy. This means that virtually everyone with a job or business, regardless of their secure mortgages, will begin feeling the effects of the bubble's consequences--the reduction in borrowing and spending which characterizes a recession. With household debt at record high levels (see chart) and U.S. savings rates at rather infamously negative levels, there is no other ready source of borrowing or pool of savings which can fuel further spending.  The sobering conclusion: while those with conventional fixed-rate mortgages are immune

to the direct ravages of declining housing values, they will still be negatively impacted by

the fall-out of the housing bubble:

The sobering conclusion: while those with conventional fixed-rate mortgages are immune

to the direct ravages of declining housing values, they will still be negatively impacted by

the fall-out of the housing bubble:

rising property taxes and/or a recessionary economy which will cut into everything from local government receipts to vendors to retail to you-name-it, even sectors and businesses seemingly far from the housing/furnishing/lending sectors which are already suffering declines in sales and employment. Thanks to polymath reader Wayne D. for raising this topic some time ago. For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2006 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |