|

|

| weblog/wEssays archives | home | |

|

How 4% of Mortgages Have Brought Down the Entire Market (August 21, 2007) Back on February 21, 2007, I invoked The Pareto principle to suggest that a mere 4% of U.S. mortgages going bad could bring down the entire U.S. housing and mortgage markets. Seven months later, that call appears to be playing out in spades. It now seems likely that the 64/4 (80/20) rule is playing out globally--the "limited" subprime meltdown is set to take down the global mortgage market and the trillions in derivatives which have been written on trillions in real estate-based debt. The list of non-U.S. banks, institutions and funds which are confessing huge losses in U.S.-based mortgage-backed securities is growing longer every day--to take but one example: French Bank Natixis has $1.4 billion exposure to U.S. subprime. Let's briefly revisit the Pareto principle.

In other words, "the vital few" (20%) influence effects more than the "trivial many" (80%). A subset of the principle is that 4% of the "very vital few" have an outsized influence on 64% of the "trivial many." Here is the Wikipedia link to The Pareto principle. This is a special case of the wider phenomenon of Pareto distributions. If the parameters in the Pareto distribution are suitably chosen, then one would have not only 80% of effects coming from 20% of causes, but also 80% of that top 80% of effects coming from 20% of that top 20% of causes, and so on (80% of 80% is 64%; 20% of 20% is 4%, so this implies a "64-4 law").The 64/4 law is playing out across multiple, mutually reinforcing meltdowns: 4% of the mortgages defaulting are bringing down the entire mortgage lending house of cards, even as 4% of the CDOs and other leveraged bets on all that debt come apart at the seams, re-writing risk on a global scale, triggering immense, catastrophic losses in 4% of the hedge funds who have over-extended leveraged bets on credit-swap and CDO derivatives--and so on, spreading ever widening circles of financial havoc. Keep this in mind: all those billions lost are in Hedge Fund Heaven. Loosening credit so speculators can borrow more money on easy terms is not going to bring those losses back. Despite months of suspiciously negative data--housing sales and starts sagging, cancellations of sales and foreclosures rising--housing apologists have maintained that the problems with subprime borrowers and lenders can be "contained." In other words, only those "few" who lose their homes will suffer any economic impact; Home Depot and Lowes sales will remain robust, construction activity will continue unchanged, employment in construction, home furnishings, remodeling, lending and real estate will continue to hold up with minimal declines, etc. This has now been revealed as fantasy. As the 4% subprime/no-doc "vital few" borrowers default, they have triggered an avalanche will will soon affect 64% of all mortgage holders. Eventually, the 20% "vital few" whose mortgages, equity lines of credit and other housing-based debt is affected will then have outsized influence on the values of fully 80% of U.S. and global real estate valuations.

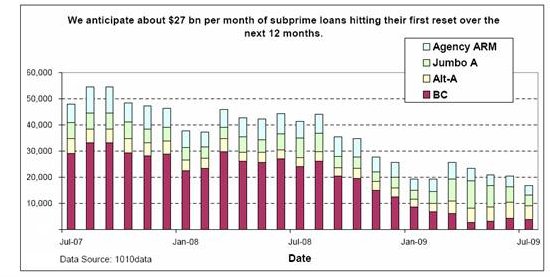

This chart reveals that fully 5% of recent home buyers are at great risk of default. Another 5% could not have qualified for a mortgage "in the good old days" (i.e. 15 years ago) so they too are vulnerable. In terms of the Pareto Principle, only 40% of that highly vulnerable 10% need fall behind on their mortgages for outsized effects to hit 64% of all homeowners. But if we dig a little deeper, this chart (courtesy of the FDIC) seems to understate the true scope of delinquencies and foreclosures. Here is the Financial Services Fact Book: Adjustable rate mortgages, loans in which the interest rate is adjusted periodically according to a pre-selected index, accounted for 31 percent of mortgage originations in 2005, up from 12 percent in 2001.The factbook also lists some very interesting charts of delinquencies: 12.9% of all FHA loans are delinquent. Are these listed as subprime? No. These are "conventional mortgages." The Factbook also states that 24.7 million homes are owned "free and clear," with no mortgage, and about 50 million have mortgages of one kind or another. About 10 million homeowners have equity lines of credit as well as a mortgage--in effect, second mortgages. Though rarely mentioned in all the hoopla about subprime ARM (adjustable rate) mortgages, it is important to note that equity lines of credit are adjustable-rate loans; they are not 30-year, fixed-rate "conventional" mortgages. The upshot: 10 million homeowners who statistically have "safe" conventional mortgages are at risk of their home equity line loans re-setting to higher rates. There's about $9 trillion in home mortgages on the books, and $500 billion is due to re-set higher. Various versions of this chart have been popping up, displaying the unsettling reality that re-sets will continue hitting consumers/homeowners all through 2008:

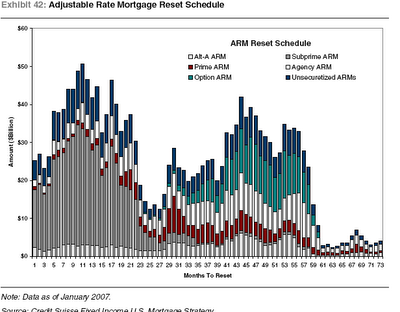

Here's another version compiled by Credit Swisse:

It's no secret that the number of delinquencies, defaults and foreclosures is rising: More Americans are losing their homes: Nothaft estimates that $500 billion in variable rate mortgages will reset, or rise, sometime this year, leaving many with a payment they can no longer afford. �Those would be the candidates for � delinquent status,� he said.Meanwhile, back at the ranch, Number of vacant homes for sale surges 34% The number of vacant homes waiting to be sold surged 34% to 2.1 million at the end of 2006 compared with the end of 2005, by far the fastest increase ever recorded, the Census Bureau reported Monday.According to the Financial Times, The inventory of new and existing homes waiting for buyers is now approaching 4m. The total value of US residential property is now around $19 trillion, according to the Joint Center for Housing Studies at Harvard University. The US Census Bureau calculates that there are around 123.9m housing units in the US. (ED: this includes condos and rental apartments)Total household debt is $11 trillion: $9 trillion in mortgages and $2 trillion in revolving credit (credit cards, etc.) That means net equity for all 75 million American homeowners is $8 trillion ($19 T - $11 T = $8 T)--including the 25 million households who own their homes free and clear. What if we subtract those folks? Since 1/3 of all homes are owned free and clear, let's assume about a 1/3 of the $19 trillion is represented by these mortgage-free homes. That's $6.5 trillion, which means all 50 million mortgage holders are left with a grand total of $1.5 trillion in net equity. If housing values decline 15%, that's a $2.85 trillion haircut off net equity. If we set 2/3 of that against mortgaged real estate, (the other 1/3 being a decline in the value of free and clear homes), then the decline collectively suffered by all mortgage holders is $1.9 trillion--enough to put them in a negative equity hole. This is a staggering conclusion, for it suggests just how a "mere" 4% delinquency/foreclosure rate could trigger a "modest" 15% decline in housing values, which would put the nation's mortgage holders (if taken in aggregate) under water: the nation's household debt would exceed the value of the mortgaged residential real estate. There are 50 million mortgages. If 4% is the magic number, that's 2 million mortgages. In other words, when 2 million mortgages enter delinquency / default, then according to the Pareto principle, that will affect the 64% "trivial many," i.e. those holding supposedly "low-risk" mortgages. According to USA Today, 2.1 million homeowners are already in trouble: Record foreclosures hit mortgage lenders: The reason many mortgage lenders are in trouble became alarmingly clear Tuesday. The Mortgage Bankers Association said more than 2.1 million Americans with a home loan missed at least one payment at the end of last year � and the rate of new foreclosures hit a record.In other words: the 4% "vital few" threshold has been breached. Also recall that 13% of FHA loans--"conventional fixed-rate mortgages"--are already in delinquency. (see Factbook link above for the chart) So while the foreclosure rate on those mortgages is still low--2% or so--the pool of potential foreclosures is large, and increasing. Here's a question that deserves to be asked: if everyone who can afford a house--even those who stretched their credit and stated incomes to the breaking point--has already bought a house, then who's left to buy 4 million empty dwellings? Please don't say someone who's selling their existing house--they're adding one unit of inventory even as they take one off. If you add up the facts presented above, it is difficult not to reach disturbing conclusions: there is no way buyers will emerge to snap up 4 million empty homes. Here's another way to consider possible Pareto effects: if 20% of the housing stock in the "hot markets" of Florida and the West and East coasts declines sharply in value, then will that cause a decline in 80% of the U.S. home market? Some other links of interest: Hedge Funds and The Pareto Principle (February 19, 2007) Pareto Principle: Causality and Patterns (February 22, 2007) Foreclosures and Financial Ruin: How Bad Will It Get? (April 26, 2006) How Many Foreclosures Will Hit the Market? (May 1, 2006) Thank you, Harun I. for recommending a re-visit to the Pareto Principle and mortgages. If anything rings true here, perhaps you will be moved to For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2007 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |