|

|

| weblog/wEssays archives | home | |

|

Sublime Subprime: Beyond The Credit Implosion (August 6, 2007)  To investment bankers packaging all those mortgage-backed securities and derivatives (CDOs),

subprime/exotic loans were indeed sublime. Despite daily exhortations by financial leaders

such as Treasury Secretary Paulson that the credit meltdown was "contained," we find that the

credit reactor core has in fact burned through its containment shield and is in full "China

Syndrome"--i.e., burning straight through the Earth to the Central Bank of China, who holds

$1.3 trillion in plunging dollars and billions in MBS and other rickety U.S. credit instruments.

To investment bankers packaging all those mortgage-backed securities and derivatives (CDOs),

subprime/exotic loans were indeed sublime. Despite daily exhortations by financial leaders

such as Treasury Secretary Paulson that the credit meltdown was "contained," we find that the

credit reactor core has in fact burned through its containment shield and is in full "China

Syndrome"--i.e., burning straight through the Earth to the Central Bank of China, who holds

$1.3 trillion in plunging dollars and billions in MBS and other rickety U.S. credit instruments.

Credit panics start like forest fires--at the periphery, or in a seemingly unimportant backwater. Thailand is not a giant of global trade, yet the meltdown of its currency triggered a global financial panic in 1997 that was eventually reinforced by Russia defaulting on its bonds in 1998. The resulting credit panic toppled Long-Term Credit Management (LTCM) and led to a dizzying 20% free-fall in the U.S. stock markets. Like drops of water falling, each mortgage default in the U.S. is a seemingly small amount of money. Yet as the defaults grow into the hundreds of thousands, they come together to form a mighty river of fear cutting straight through the soft sand of the global credit markets. The credit "dislocation"/panic doesn't stop with subprime. Take a look at this chart of total U.S. mortgages, and see how few are "safe" 30-year fixed-rate loans:

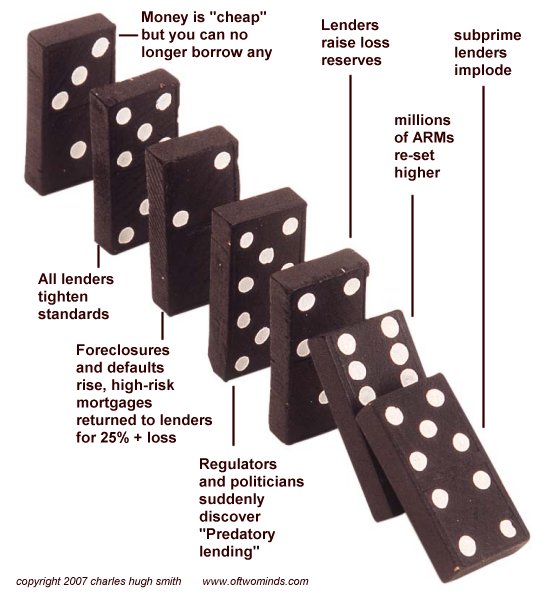

Add in all the other at-risk loans--FHA/VA, alt-A, no-down, adjustable-rate and HELOC--and you get a domino effect which is unstoppable:

This site and many others suggested that neither housing demand nor buyers/borrowers were as strong as the cheerleaders claimed. Please read these entries from late 2005 and May 2006: Housing Market Slips Toward Cliff (December 28, 2005) The Demographics Behind the Housing Market Decline (December 29, 2005) How Many Foreclosures Will Hit the Market? (May 1, 2006) The defaulting of tens of thousands of mortgages promises to topple dominoes far beyond the mortgage credit markets. Consider just this small sampling: Let's say the eventual "owner" of the property claims the house is worth $300,000, and tries to sell it for $280,000, telling potential buyers that they've dropped the price to reflect the $20,000 in property tax liens which have to be paid by the new buyer. Who will be dumb enough to think this is a good deal? Very few, I suspect, for everyone knows the house may well actually be worth $250,000--who even knows? Meanwhile, every 6 months the tax liens grows larger. Construction Defects: The Flood to Come? (June 1, 2006) and Construction Defects, The Flood to Come, Part II (June 3, 2006). BusinessWeek finally woke up and ran a story this week: You Call This A Home? The next boom for builders may be complaints from angry homeowners. It doesn't take an attorney to wonder: so what happens if owners are short of funds? Which one do they pay: their mortgage or their owners' dues? And what does the condo association do to owners who fall behind on their dues? Evict them? Sue them? Talk about a legal black hole. In 1986, Mr. Market missed its appointment; but that simply set up the October 1987 "appointment" which resulted in a 22% drop in a single day. Now the U.S. stock market has blown right past this 2006 "appointment"--but the appointment wasn't cancelled, it was simply re-scheduled for the future. That future is now:

Historically, a 20% decline is quite a normal occurrence. With this is mind, it is risible how market cheerleaders/pundits are screaming and shouting and shaking in terror now that the Dow Jones Industrial Average has declined a mere 6% from it's all-time high. Recall that stock market meltdowns aren't the result of some fundamental dislocation in business or the economy--they result from credit contractions/panics/dislocations. Which is exactly what we have right now. For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2007 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |