Rent Bubble = Housing Bubble = Rent Bubble

August 3, 2015

Both bubbles (rents and housing) are vulnerable to popping.

Here is the conventional narrative about rents and housing valuations:

1. Rents have soared because people can't afford to buy a house and have to rent

2. Based on soaring rents, housing is fairly valued

In other words, rents and housing are tautological: rents are rational because housing values are rational, and housing values are rational because rents are rational.

Nice, but wrong: rents and housing are self-reinforcing bubbles: rents are soaring because housing is unaffordable, i.e. echo-bubble valuations. Soaring rents then justify bubblicious home prices.

Is the Echo Housing Bubble About to Burst?

One way to establish fair value of a home is to multiply the rental income the house can fetch in the open market. Multiply gross rents (before expenses, property taxes, etc.) by 8 to 15 (depending on the desirability of the locale and property) and you get an investment-based valuation.

So if a property earns $50,000 annually in gross rental income, the property is worth around $500,000, with premiums being added for low vacancy rates, desirable neighborhood, well-maintained home, etc.

Another approach is to calculate the net rent (total rent minus all expenses except mortgage) and base the value on the net rental income. Any property yielding 5% after expenses (i.e. 20 times net income) is an attractive investment in a world of negative short-term interest rates and 3% returns on 30-year bonds.

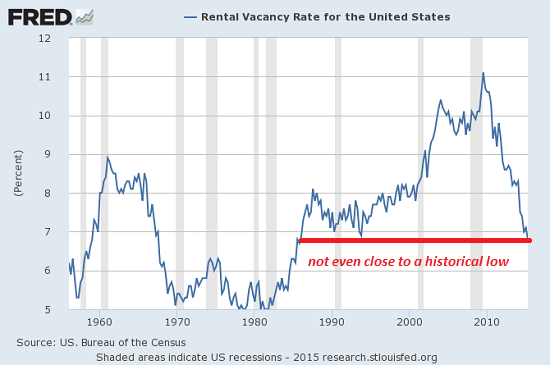

Rental demand is reflected by vacancy rates; low vacancy rates reflects high demand. Vacancy rates are low, but not at historic lows except in certain high-demand urban zones.

Vacancy rates were much lower in the stagflationary late 1970s - early 1980s. The claim that vacancy rates justify unprecedented rents is at odds with the data. (High-demand, limited-supply areas such as San Francisco are atypical; vacancy rates in these areas tend to be very low, in the 1% -2% range.)

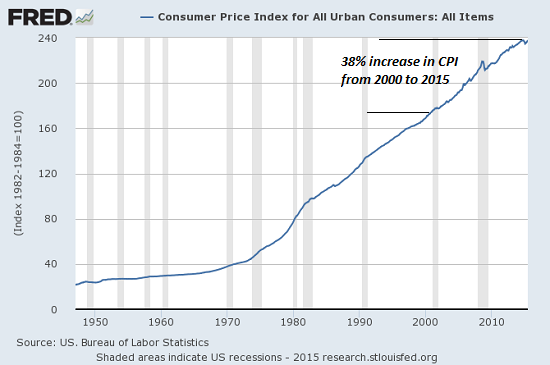

Here is the urban-area consumer price index: it's up 38% from 2000:

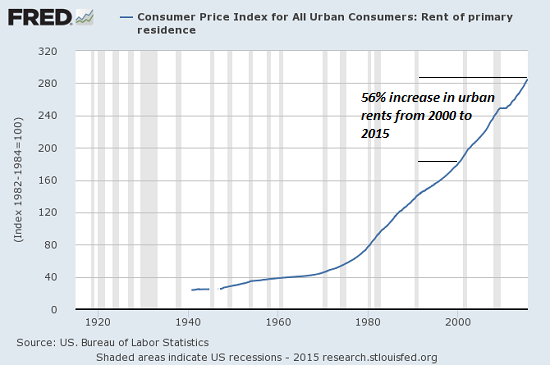

Here is the urban-area rent index: it's up 56% from 2000--much higher than the rest of consumer prices, and climbing fast.

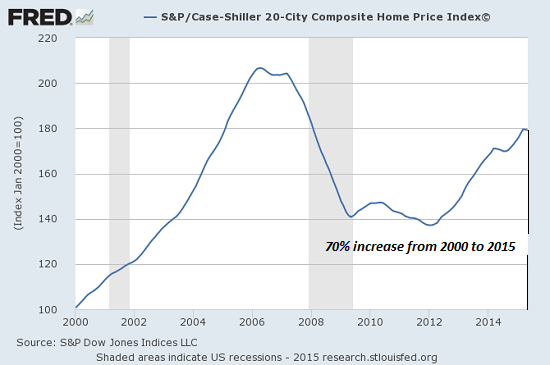

Here is the Case-Shiller home price index: it's up 70% from 2000:

Rents were soaring from 2010-2012, while housing prices stagnated. If housing valuations were based on rents, then they should have risen in lockstep with rents. They didn't.

Housing is in an echo bubble driven by overseas hot money flooding into North America to escape currency devaluations and crackdowns on corruption, and the easy-money policies of the Federal Reserve, which purchased $2 trillion of mortgages (20% of the entire U.S. mortgage market) to push mortgage rates to the floor.

Both bubbles (rents and housing) are vulnerable to popping. The real test of valuation is: what's it worth in a recession, after all the easy money and the jobs that depended on easy money have vanished?

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Wayne H. ($75), for your monumentally generous contribution to this site-- I am greatly honored by your steadfast support and readership. |