|

|

| weblog/wEssays archives | home | |

|

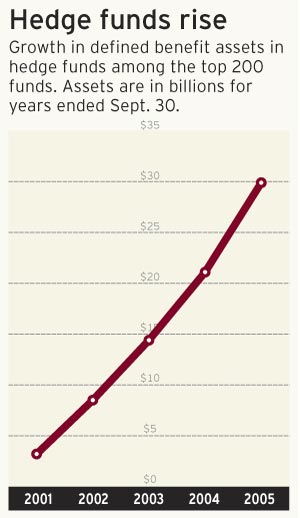

Who's Getting Alpha? (February 15, 2007) Hedge funds--those loosely regulated funds reserved for rich folks and institutions--like to claim they outperform the market (alpha). But is that true? It's an issue, of course, because of the enormous rise in the number of hedge funds and in the assets they manage:

First, let's consider what the hedge funds skim for themselves and churn in brokerage/trading fees. In the standard "2 and 20" structure, the managers receive 2% of the assets they manage as a management fee and keep 20% of the profits as incentive pay. How much does that add up to? For comparison, let's consider the Wall Street (non-hedge fund) bonuses: Wall Street executives hit $23.9 billion: (USA Today) This year's bonus pool for Wall Street executives hit $23.9 billion, the New York State Comptroller's office estimates. That's a 17% jump from last year's bonus pool of $20.5 billion, and it works out to an average bonus of $137,580 for every person employed in the financial services industry.Sounds cushy, but this pales in comparison to what the hedge fund managers pay themselves:

Wall Street giants’ compensation still pales in comparison with their hedge fund counterparts: (New York Times) In 2005, the top hedge fund manager took home $1.5 billion in pay while the price of entry to be on the list of the top 25 paid managers, compiled by Institutional Investor’s Alpha magazine, was $130 million. Here is the top 10 hedge fund managers' income: The full top 10 list of hedge fund earners according to Trader Monthly includes: 1. T. Boone Pickens - estimated 2005 earnings $1.5bn + 2. Steven A. Cohen, SAC Capital Advisers - $1bn + 3. James H. Simons, Renaissance Technologies Corp. - $900m - $1bn 4. Paul Tudor Jones, Tudor Investment Corp. - $800m - $900m 5. Stephen Feinberg, Cerberus Capital Management - $500 - $600m 6. Bruce Kovner, Caxton Associates - $500m - $600m 7. Eddie Lampert, ESL Investments - $500m - $600m 8. David Shaw, D.E. Shaw & Co - $400m - $500m 9. Jeffrey Gendell, Tontine Partners - $300m - $400m 10. Louis Bacon, Moore Capital Management - $300m - $350m 10. Stephen Mandel, Lone Pine Capital - $300m - $350m Here's an excerpt from Barron's Up and Down Wall Street: The average pay of the top 126 hedge fund managers last year was $363 million, up some 45% from the year before.Clearly, the hedgies pay themselves handsomely. But they also generate huge fees from "churning" or trading their immense holdings. The Great Unwinding Is Coming (Financial Times, Alphaville) Transaction costs run to 4 per cent of the $1,300bn of hedge fund assets under management. Manager salaries and performance fees take another 4-5 per cent, meaning hedge funds need to generate average annual returns of close to 20 per cent to keep everyone happy (including their investors).And here's an interesting piece passed on by contributor U. Doran on the high rate of churn in today's markets: Underreported, Understated And Certainly Not Understood.

So how much alpha is left for the hedge fund clients? Not all the clients are rich folks with too much money; as this chart shows, pension funds--"defined benefit plans"-- have been rushing into hedge funds, hoping for that illusive alpha. In fact, the "quant shop" hedge fund Barclays Global Investors (BGI) profiled in the BusinessWeek story below largely trades ETFs (exchange traded funds) for the benefit of its 2,800 institutional clients like pension funds. The firm manages $1.62 trillion. From Outsmarting the Market: (BusinessWeek) Over the last five years the S&P 500-stock index has outperformed 71% of large-cap funds, the S&P MidCap 400 has topped 83.6% of mid-cap funds, and the S&P SmallCap 600 has bested 80.5% of small-cap funds, according to Standard & Poor's, a unit of The McGraw-Hill Companies.So BGI--one firm--skims 15% of the entire global haul of alpha. How much of the remaining $25 billion is divvied up amongst the other 9,000 hedge funds? That's an awful lot of thin (or non-existent) slivers. In summary: Wall Street pulls down $23 billion in bonuses (not counting salaries and stock options, mind you--this is all cash), hedge fund managers pay themselves another $30 billion or so (the top 10 pulled down $7.5 billion themselves), and global investors got a grand total of $30 billion, or .1% --a meagre tenth of a percent--of the global market's value in alpha. Pardon me for being underwhelmed by the fantastic returns being generated by hedge funds and their Wall Street pals who execute the trades and arrange the lucrative buyouts. Meanwhile, back in the real world, as more and more Americans fall behind on their mortgages, Banks Try to Return High-Risk Loans To the Originators. For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2007 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |