|

|

|

||||||||||||

|

Why Central States/Banks Inflate Asset Bubbles, and Why They Implode (February 28, 2013) Inflating phantom assets to collateralize expanding debt is failing due to diminishing returns on stimulus, zero-interest rates, money-printing and monetization of Federal debt. That the policies of central states and banks have led to one disastrous asset bubble after another over the past 15 years is undeniable. This poses the question: is this serial bubble-blowing intentional, or are the bubbles merely unintended consequences of the neoliberal, neofeudal model of financialization that dominates global finance? The answer boils down to this: inflate assets or die. The only way to support consumption in an era of declining wages is to enable more borrowing, and the only way to enable more borrowing is to: 1. Lower interest rates to near-zero so stagnant income can leverage higher debt 2. Inflate assets to create phantom collateral that can then support additional debt. Central states live off taxes skimmed from wages and profits. If wages are stagnant, the state needs profits and capital gains to rise to support higher tax revenues. In other words: inflate assets or die. The entire scheme of generating GDP with more and more debt now yields diminishing returns. Unfortunately for the central states and banks, though their unprecedented fiscal stimulus and money-printing has doubled the stock market off its 2009 lows, efforts to reflate housing have been tepid at best. This matters because only the top 10% own enough stocks and bonds to make a difference in household net worth, while two-thirds of households own a home. Inflating another asset bubble in stocks was nice for the financial Aristocracy and their technocrat-class, but it didn't do much to boost the net worth of the bottom 90% or enable more borrowing. Let's look at some charts that reflect the failure of massive money-printing and credit expansion to actually boost wages and household borrowing. First up: real income (adjusted for inflation) has been flat to down since 2000:

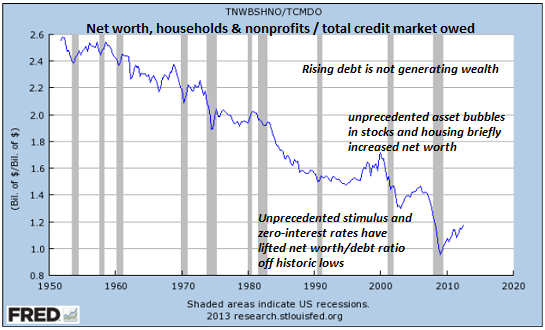

Meanwhile, the ratio of household net worth to total credit market debt owed has plummeted, meaning that debt is rising much faster than net worth. This is called debt saturation: adding more debt generates less and less expansion of wealth.

Cheap credit and financialization has boosted stock valuations far above the real economy, as reflected by the GDP. This chart shows just how disconnected stocks have become from the real economy.

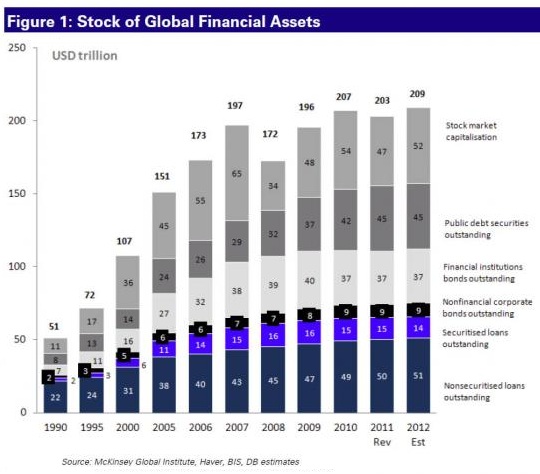

We can see this same expansion of asset valuations in global assets, which quadrupled in a mere 17 years (1990 - 2007) of financialization and bubble blowing:

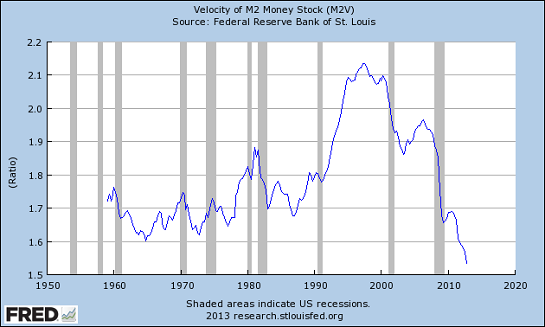

The diminishing return on stimulus and credit expansion is revealed by money velocity, which has fallen off a cliff:

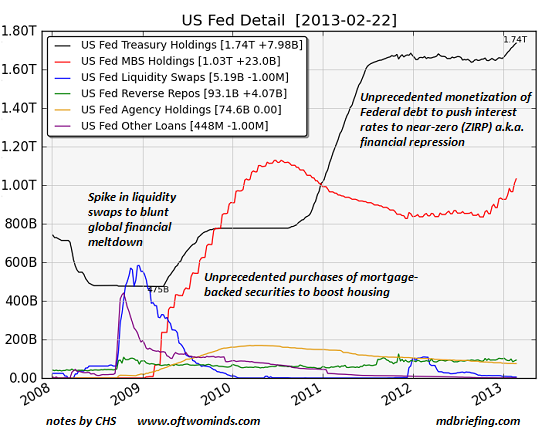

The Fed has gone all-out to lower interest rates to near-zero and mortgage rates to historic lows, as well as monetize Federal borrowing via purchasing Treasury bonds (Chart courtesy of mdbriefing.com):

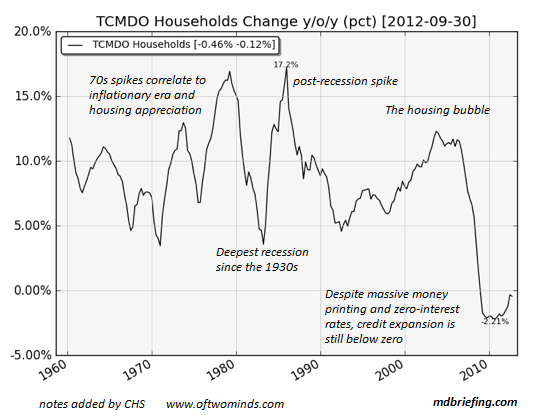

Despite these unprecedented measures to boost asset valuations and borrowing, household debt expansion remains below zero: debt is declining faster than it is being created, i.e. deleveraging.

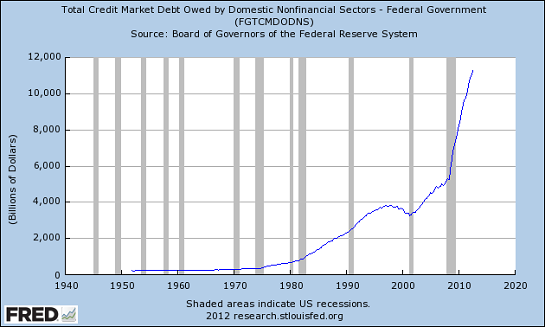

The central state has tried to prime the debt pump by taking up the slack left by private-sector deleveraging by ramping up massive public-sector borrowing:

This has created structural deficits as tax revenues--despite the tailwind of highest-ever corporate profits and a stock market that more than doubled in four years-- are far below spending.

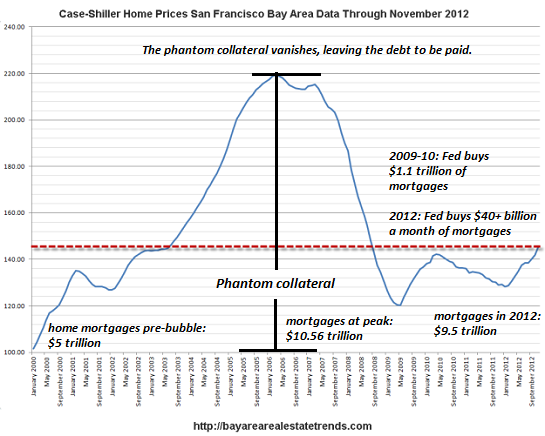

Unfortunately for Central Planners, all their unprecedented efforts to reflate the housing bubble's phantom assets are not getting much traction. What did they expect in an economy with 19 million vacant dwellings and declining real income for 90% of households?

Bottom line: inflating phantom assets to collateralize expanding debt is failing

due to diminishing returns on stimulus, zero-interest rates,

money-printing and monetization of Federal debt. Once debt stops expanding, the

house of cards that is dependent on ever-expanding debt collapses.

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:  1. Debt and financialization

1. Debt and financialization

2. Crony capitalism and the elimination of accountability 3. Diminishing returns 4. Centralization 5. Technological, financial and demographic changes in our economy Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of

the same coin: once we accept responsibility, we become powerful.

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

NOTE: gifts/contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Subscribers ($5/mo) and contributors of $50 or more this year will receive a weekly email of exclusive (though not necessarily coherent) musings and amusings. At readers' request, there is also a $10/month option. What subscribers are saying about the Musings (Musings samples here): The "unsubscribe" link is for when you find the usual drivel here insufferable.

All content, HTML coding, format design, design elements and images copyright © 2013 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I am honored if you link to this essay, or print a copy for your own use.

Terms of Service:

|

Add oftwominds.com

Oftwominds.com #7 in CNBC's

#25 in the top 100 finance blogs

|