|

|

|

||||||||||||

|

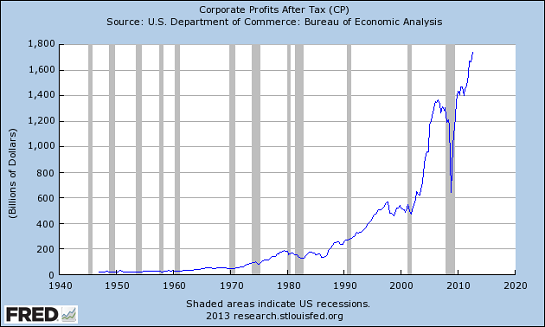

Cheap, Abundant Credit Creates a Low-Return, Bubble-Prone World (February 12, 2013) By bailing out banks and targeting equity prices, the central banks are exacerbating the misallocation of savings/financial capital to historically overvalued corporate equity. What happens when central banks make credit cheap and abundant? All that cheap money chases scarce productive assets. The yields on assets drop, and speculative "risk-on" assets are boosted into bubbles. Even as corporate profits have skyrocketed, equity valuations have risen apace, keeping yields at historically low levels.

Just to state the obvious: does that trajectory strike you as sustainable? Up almost 300% in less than four years? In a debt-burdened global economy, where are the next $1.75 trillion in corporate profits going to come from? Anyone who claims "stocks are cheap" would do well to study these charts, which are courtesy of longtime correspondent B.C.:

Another measure of the S&P 500 yield using corporate bond yields (Baa):

In response to my observation that this looked like too much cheap credit chasing too few productive assets, B.C. added these explanatory comments:

This is characteristic of the liquidation/hoarding of a debt-deflationary Long-Wave Trough depression. The financial media and economists want us to believe that the Fed printing is "stimulus" when in fact it is part of the "liquidation" of Fed member banks' balance sheets of bad assets. Thank you, B.C. for placing the charts in context. B.C. also passed along this investment-bank report on the same topic, The Low-Return World (Credit Suisse).

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:  1. Debt and financialization

1. Debt and financialization

2. Crony capitalism and the elimination of accountability 3. Diminishing returns 4. Centralization 5. Technological, financial and demographic changes in our economy Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of

the same coin: once we accept responsibility, we become powerful.

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

NOTE: gifts/contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Subscribers ($5/mo) and contributors of $50 or more this year will receive a weekly email of exclusive (though not necessarily coherent) musings and amusings. At readers' request, there is also a $10/month option. What subscribers are saying about the Musings (Musings samples here): The "unsubscribe" link is for when you find the usual drivel here insufferable.

All content, HTML coding, format design, design elements and images copyright © 2013 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I am honored if you link to this essay, or print a copy for your own use.

Terms of Service:

|

Add oftwominds.com

Oftwominds.com #7 in CNBC's

#25 in the top 100 finance blogs

|