| |

The New Road to Serfdom: A Negative-Equity Mortgage

(May 9, 2006)

The current issue of Harper's features a lead article entitled "An Illustrated Guide to the Coming Real

Estate Collapse" by Michael Hudson. Here is a precis of the piece.

The current issue of Harper's features a lead article entitled "An Illustrated Guide to the Coming Real

Estate Collapse" by Michael Hudson. Here is a precis of the piece.

Thanks to Marinite, proprietor of the

Marin Real Estate Bubble blog, I read a lengthy 2003 interview of economist Michael

Hudson on Alexander Cockburn's always-provocative website Counterpunch:

The Coming Financial Reality. Hudson is a big-picture guy with a non-standard view

of our economic system and the housing bubble.

Hudson identifies several key points in all great speculative bubbles: a government which

fosters the conditions for a bubble, and a speculative mindset which eschews actual

investment for "making money with money."

Referring to the classic South Seas Stock Bubble, he says:

Every stock market bubble in history, starting with the South Sea and Mississippi bubbles

in the 1710s in Britain and France, has been sponsored by government. The driving force has

been the government's attempt to cope with debt obligations beyond its foreseeable ability

to pay. Creating a bubble has been a way to solve their public debt problem--and to pay off

political insiders at the same time, thereby killing two birds with one stone.

Modern governments are not politically able to simply default on their debts--at least, not

debts owed to their own bondholders in their own currency. The problem has to be solved

through "the marketplace."

Stocks in the South Sea and Mississippi Companies were issued in tranches, permitting people

to buy on margin with only a small proportion as down payment, so that they could quickly

double their small initial payment as the stocks were engineered upward in price. It seemed

that money could be made off money itself. This is a basic illusion that is necessary for

bubbles to take off.

Saving, stock and bond speculation and real estate speculation do not by themselves lead to

new investment. In fact, the higher speculative and financial returns are, the less incentive

there is to actually tie down money in building new factories and expanding business.

Hudson makes many other fascinating points in the interview, but for now, let's focus on

the connection to the housing bubble. What can be gleaned from his analysis?

The Federal Reserve engineered the housing bubble by lowering interest rates to an

inflation-adjusted rate of zero.

With legitmate investments earning low returns compared to housing, the mindset of money

for nothing, i.e. a "free lunch," became embedded in the real estate market.

In the euphoria of profiting from high leverage, i.e. putting no or low money down

and leveraging the value of real estate with an interest-only mortgage, people have forgotten

that the borrowed money has to be paid back.

As housing values decline, they fall below the amount due on mortgages--negative

equity, in which the hapless homeowner owes more than his house is worth.

The Federal Reserve engineered the housing bubble by lowering interest rates to an

inflation-adjusted rate of zero.

With legitmate investments earning low returns compared to housing, the mindset of money

for nothing, i.e. a "free lunch," became embedded in the real estate market.

In the euphoria of profiting from high leverage, i.e. putting no or low money down

and leveraging the value of real estate with an interest-only mortgage, people have forgotten

that the borrowed money has to be paid back.

As housing values decline, they fall below the amount due on mortgages--negative

equity, in which the hapless homeowner owes more than his house is worth.

Here is a list of the article's 20 illustrated points:

1. Mortgages account for most of the net growth in debt since 2000

2. A $1,000 monthly payment can carry different levels of debt

3. Interest rates have been falling since 1981

4. Corporations hide their real estate profits behind depreciation

5. The tax burden has shifted from property to labor and consumption

6. Real estate prices have far outpaced national income

7. Capital gains are taxed at a lower rate than ever

8. Housing prices have far outpaced consumer prices, even as monthly payments remain affordable

9. Mortgage debt is rising as a proportion of GDP

10. The production/consumption economy

11. The Keynesian economy

12. The FIRE economy

13. The miracle of compound interest

14. The rentier economy

15. Rich people are getting a bigger share of overall economic rent

16. The miracle of compound interest will inevitably confront the S-curve of reality

17. In Japan, real estate prices fell as quickly as they rose

18. Interest rates are on the rise

19. The annual sale of existing homes has more than doubled since 1989

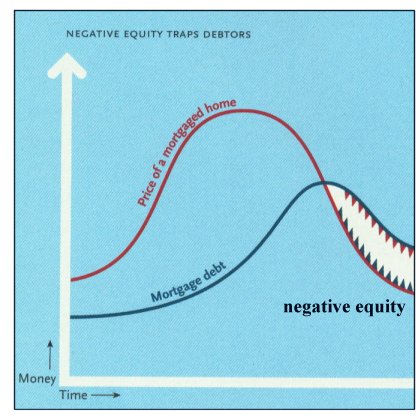

20. Negative equity traps debtors

This is the conclusion to the great housing bubble Hudson foresees: millions

of indebted households paying interest on mortgages which are greater than the value of

their homes. The interest will be collected by a new "rentier" class of mortgage holders

who are not even capitalists, in the sense that they are not creating value or wealth with

their capital and knowledge, but living off the "new serfs" who will struggle for decades

to pay off their massive mortgages.

Bleak, it's true--especially if it turns out to be true.

For more on this subject and a wide array of other topics, please visit

my weblog.

copyright © 2006 Charles Hugh Smith. All rights reserved in all media.

I would be honored if you linked this wEssay to your site, or printed a copy for your own use.

|

|