|

|

|

||||||||||||

|

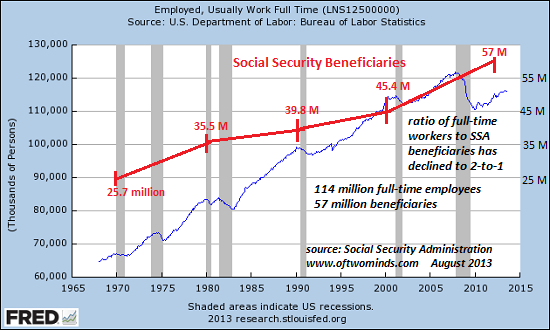

The Generational Injustice of Social (in)Security (November 6, 2013) Forcing young workers to pay into a Ponzi Scheme is generational injustice on a vast scale. Why should young workers pay into a retirement system that will give them nothing, a system that will dissolve in insolvency long before they're old enough to retire? This is a question that Max Keiser posed in our conversation on Peak Retirement, and I think it deserves an answer. I think the core issue here is the generational injustice of pay as you go social programs, which boil down to unsustainable Ponzi schemes. As I noted yesterday in The Problem with Pay-As-You-Go Social Programs (November 5, 2013), all pay as you go programs funded by payroll taxes--Social Security and Medicare in the U.S.--are only sustainable if the number of workers rises faster than the number of beneficiaries, because it takes multiple full-time workers' payroll taxes to fund each beneficiary. As I showed yesterday, it takes about ten low-wage (and hence low-payroll tax) workers to fund one retiree. At this rate, Social Security's 57 million beneficiaries (on its way to 70+ million as the Baby Boom retires en masse) would need 500 million workers paying into the system for it to be sustainable. It takes only a few high earners (those making $85,000 or more annually) to fund one retiree, but there are too few high earners to support the system (13 million workers earn $85,000 or more, while beneficiaries will soon top 60 million). While the number of beneficiaries will soar for the next decade as 60+ million Baby Boomers retire, the number of full-time jobs has stagnated, as this chart shows:

If the system doesn't change, the young workers currently paying payroll taxes to fund their elders' retirements will get little to nothing out of the system. This is ordained by two trends: demographics and the end of (paid) work. Global Reality: Surplus of Labor, Scarcity of Paid Work (May 7, 2012). A huge cohort of retirees requires an even larger cohort of workers to support its retirement in pay as you go systems. This is what renders Social Security a Ponzi Scheme: a Ponzi Scheme only works as long as the number of new marks is substantial enough to pay the promised riches. Once the number of marks declines below a threshold, the Ponzi Scheme implodes. The soon-to-be 70 million beneficiaries of Social Security would need roughly 210 million full-time workers earning decent money to sustainably fund their benefits. The U.S. economy is short about 100 million full-time jobs, and given the end of work realities I have often covered here (just type end of work into the custom search box on the main blog page), the number of full-time jobs with decent pay may well decline sharply, even in "good times," i.e. periods of expansion. We can expect widespread destruction of paid work as technology creatively destroys one sector after another. Why should young workers pay into a retirement system that cannot possibly offer them any benefit? The conventional answer is a lie: "Social Security is essentially eternal and will be here forever." The other conventional answer is pure self-serving, self-justification by retirees: "We wuz promised." Well guess what, Boomers (I am 59 and a Boomer), things change in pay as you go systems. When the number of full-time workers falls to 2-to-1 or less and the number of retirees drawing benefits skyrockets, the system is no longer sustainable, regardless of what was promised by feckless politicos and their toadies. The Social Security system could be made sustainable, but it would take radical reform. The constituencies that would oppose these reforms are among the most political powerful in the nation, so there is no chance these would ever be aired, much less approved: 1. Eliminate Social Security benefits for double and triple-dippers, i.e. those drawing pensions from other private or government sources. Re-engineer Social Security into a system for those with no other retirement benefits or pensions. 2. Tax all income, not just earned income. Lower the total Social Security tax from 12.4% to 10% but apply it equally to all income. Why should someone earning $1,000,000 pay less a percentage than someone earning $10,000? Why should I pay nothing on $100,000 I skimmed in a stock trade? Lower the tax but tax all income. Simple, fair, no loopholes. 3. Ditch the bogus Trust Fund of lies and set up a real Trust Fund that is outside the Federal Budget and Congressional avarice. Any surplus (i.e. when taxes collected exceed benefits paid in that year) would go into a true Trust Fund that uses the cash to buy Treasuries, other government bonds and AAA corporate bonds. This fund would thus help keep interest rates low, and the interest generated by the bonds would be real, not borrowed. Congress would not be allowed to appropriate the Trust Fund for any purpose (bridges to nowhere, discretionary wars, etc.). It would be managed by trustees elected by the citizenry. With a true Trust Fund, young workers would actually have some hope that the fund would still have real assets to liquidate to fund their retirement. Radical transformation is necessary if Social Security is to become something other than a massive wealth transfer scheme from the young to the elderly. Forcing young workers to pay into a Ponzi Scheme is generational injustice on a vast scale. Self-serving justifications of the status quo by those benefiting from this transfer of wealth should be outed for what they are: justifications of exploitation, avarice and injustice.

Keiser Report: State Sanction Profits Max, Stacy and guest CHS

cover a wide range of topics...

The Nearly Free University and The Emerging Economy: The Revolution in Higher Education Reconnecting higher education, livelihoods and the economy

With the soaring cost of higher education, has the value a college degree been turned upside down?

College tuition and fees are up 1000% since 1980. Half of all recent college graduates are jobless or underemployed, revealing a deep disconnect between higher education and the job market.

It is no surprise everyone is asking: Where is the return on investment? Is the assumption that higher education returns greater prosperity no longer true? And if this is the case, how does this impact you, your children and grandchildren?

The Nearly Free University and the Emerging Economy clearly describes the

underlying dynamics at work - and, more importantly, lays out a new low-cost model for

higher education: how digital technology is enabling a revolution in higher education

that dramatically lowers costs while expanding the opportunities for students of all ages.

The Nearly Free University and the Emerging Economy provides clarity and

optimism in a period of the greatest change our educational systems and society have seen,

and offers everyone the tools needed to prosper in the Emerging Economy.

Read the Foreword, first section and the Table of Contents.

Kindle edition: list $9.95

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify. We will cover the five core reasons why things are falling apart:  1. Debt and financialization

1. Debt and financialization

2. Crony capitalism 3. Diminishing returns 4. Centralization 5. Technological, financial and demographic changes in our economy Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Once we accept responsibility, we become powerful.

NOTE: gifts/contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Subscribers ($5/mo) and contributors of $50 or more this year will receive a weekly email of exclusive (though not necessarily coherent) musings and amusings. At readers' request, there is also a $10/month option. What subscribers are saying about the Musings (Musings samples here): The "unsubscribe" link is for when you find the usual drivel here insufferable.

All content, HTML coding, format design, design elements and images copyright © 2013 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I am honored if you link to this essay, or print a copy for your own use.

Terms of Service:

|

Add oftwominds.com

|