Here's Why Housing Must be Propped Up

October 15, 2015

If housing tanks, the last prop under the veneer of middle class wealth collapses.

The Powers That Be have gone to extraordinary lengths to prop up housing by whatever means are necessary since the collapse of the housing bubble in 2008: the Federal Reserve has pushed mortgages rates down by buying mortgage-backed securities, the federal housing agencies (FHA, VA) have issued millions of low-down payment loans, and the federal government has essentially taken over the mortgage industry, backing 90+% of all mortgage loans.

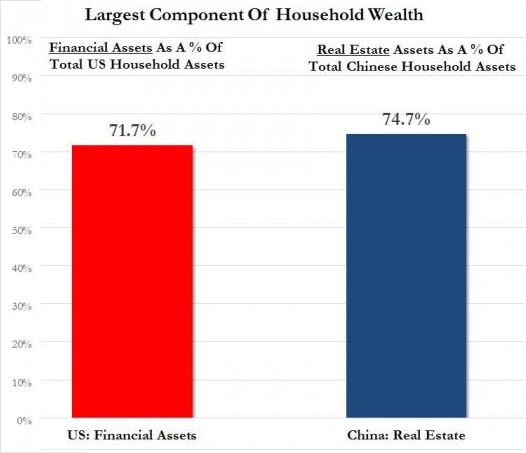

Why is the status quo so keen on propping up housing? If we examine this chart of U.S. and Chinese household assets, we understand why Chinese authorities would be keen to prop up housing values--75% of China's household assets are in real estate. Meanwhile, U.S. household assets are predominantly financial:

So why are U.S. authorities going all out to prop up housing if it represents such a modest share of total household wealth? I see two dynamics at work.

The majority of household assets are owned by the top 10%, and this includes the majority of financial assets. The top .1% own 22% of all U.S. household wealth, the top 1% own 35% and the top 10% own 75%.

Households below the top 10% may have financial assets such as insurance policies, 401K accounts or pensions funded by employers, but a house is typically the largest store of value the household owns.

If you want to make the top 1% and top 10% happy, you prop up stocks and bonds. if you want to make the 60% of the populace who own a home happy, you prop up housing.

2. Housing is the only real source of the wealth effect for households below the top 10%.

As earned income has stagnated for secular reasons (automation, rising debt service, stagnating productivity gains, advantages of capital over labor, globalization/ wage arbitrage, etc. etc.), the Status Quo has attempted to compensate for this decline in middle class earned income with gains in unearned income/wealth via asset inflation-- housing being the major component of middle class wealth, and stocks/bonds to a lesser degree.

Unfortunately for the Powers That Be, their mechanisms for boosting asset prices (with the goal of generatingthe wealth effect in the middle class) also generate credit/asset bubbles.

These boom/bust cycles actually reduce middle class wealth as people buy at the top and then see their paper wealth plummet in the next crash.

This has left many middle class households either 1) too cash-poor to save money to gamble in stocks or 2) wary of investing in stocks. That leaves housing as the only possible "fix" for stagnating middle class income/wealth.

Housing doesn't just create paper wealth; it can also boost income--via HELOCs (home equity lines of credit), cash-outs followed by a move to a lower-cost region, reverse mortgages, etc.

If housing tanks, the last prop under the veneer of middle class wealth collapses. No wonder the Powers That Be are so desperate to prop up housing. But the bubbles and busts they've engineered are integral to credit/asset booms; their goal--a steady, permanent rise in prices that never falters--simply isn't possible.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Lewis D. ($60), for your superlatively generous contribution to this site -- I am greatly honored by your steadfast support and readership. |

Thank you, Maurice K. ($5/month), for your most generous subscription to this site -- I am greatly honored by your support and readership. |

Discover why Im looking to retire in a SE Asia luxury resort for $1,200/month.