|

|

|

Summary, reader comments and additional information can be found at the end of the

essay.

What Sort of Retirement Will $1,294/Month Buy in the U.S.?Retirement is an increasingly pressing issue for two reasons: rising financial uncertainties and the 75 million Baby Boomers entering retirement. In the U.S., there are already 38 million retirees drawing Social Security benefits. That number will soar as the Boomer Generation (born 1946 - 1964) retires en masse. Meanwhile, financial certainties are eroding. The Social Security System is not as rock-solid as boosters claim; the Trust Fund is illusory, and benefits will increasingly be paid with borrowed dollars as benefits exceed the system's payroll tax revenues. The worker-to-retiree ratio is rapidly approaching an unsustainable 2 workers for every retiree. Zero interest rate policies (ZIRP) have gutted retirees' income from conventional safe investments, traditionally the bulwark of retirees who can't afford to risk their nest egg. Most analysts agree zero-interest rates are here to stay--unless inflation takes off, and that will create another problem: eroding purchasing power. The financial rules are being changed without warning. As the global financial system buckles under all the pressures I've discussed for years--demographics, excessive debt and leverage, stagnant earnings, etc.--authorities change the rules overnight to keep the system afloat. What can we count on? Not much. Governments are raising taxes on retirement incomes, slashing benefits, and imposing an array of capital controls--broad;y speaking, what's known as financial repression. ZIRP and other policies have pushed investors into risk assets such as stocks and junk bonds, markets that inevitably suffer sharp downturns. Everyone expects these assets to bounce back, but we're in uncharted waters globally and we may find the next downturn doesn't bounce back. In essence, the risks have been offloaded onto retirees. Defined-benefit pensions are only available to government employees, and as government deficits soar and yields on risk assets plunge, even these might not be as safe as many believe. The Social Security Administration estimates that roughly 60% of the Boomer generation will have less than 75% of their pre-retirement income once they retire. Given that this projection is based on wildly optimistic assumptions about global growth and investment yields, the reality is likely to be far worse. Let's ask a simple question: what sort of retirement does $1,294 a month buy in the U.S., Canada or Europe? That's the average Social Security monthly retirement benefit. Of course most people have savings, annuities, IRAs or other pensions to supplement Social Security, but let's start with this question: what sort of retirement does $1,294 a month buy in the U.S., Canada or Europe? We all know the answer is, not much. Perhaps something along these lines:

OK, so it still buys a bit more than this--but not by much once we factor in the costs of three meals a day, routine medical expenses, rent or mortgage/property tax payments and some activities/entertainment. If a retiree owns their home free and clear, lives in a region with low property taxes, has adult children nearby to help, is in good health and has multiple pensions and substantial retirement savings, then retirement in North America/Europe can be relatively comfortable. But what about everyone who doesn't fit this profile? And how about everyone who retires early, or is forced to retire early? What sort of retirement options are open to them if money is tight? These are pressing issues not just for Americans, but for everyone in high-cost economies earning near-zero yields on their savings while costs for essentials keep rising: that includes Canada, many European nations and other developed-world economies. One solution--retiring overseas--was amusingly explored in the film The Best Exotic Marigold Hotel. The plot of the movie is real-life for millions of people in Europe, Japan and the U.S., for what they can afford in retirement at home is miserable: an institutional warehouse for the elderly, a trailer park, a tiny room, and little money for actual living. Overseas--in the film, India--their limited income goes a lot farther. How much farther? Here's the sort of retirement that $1,294 a month buys in Southeast Asia:

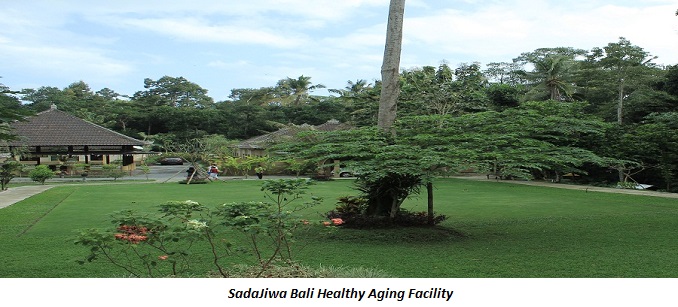

It may seem unbelievable, but these retirement resorts/care facilities cost very little when measured in U.S. dollars. The monthly fee for Sadajiwa in Bali is 17 million rupiah. That sounds like a princely sum until we divide it by 14,620-- the current rupiah/dollar exchange rate. The monthly fee is $1,163 per person, and $1,846 for a couple. This includes three meals a day, various activities, routine medical services (nurse's visits, etc.) and spacious accomodations. In Chiang Mai (northern Thailand), 37,000 baht a month works out to $1,028/month to stay in the Care Resort Chiang Mai, which offers more extensive medical care. Many of you know I have studied Asian culture for over 40 years, and traveled in a variety of Asian countries, specifically China, Japan, South Korea and Thailand. We have friends in these and other East/Southeast Asian countries. Yes, the food can be spicy, the bugs large, the streets noisy, the tropic air heavy and the languages difficult to learn. But on the other hand, there are the immensely rewarding joys of new cultures, new experiences, new friendships and new landscapes to explore. I have established a relationship with my longtime colleague Gordon T. Long's company, Financial Repression Authority, to seek out retirement opportunities in Southeast Asia. If you're interested in exploring this option, visit the FRA Retirement Solutions site, which currently lists three retirement facilities in Indonesia (Bali) and Thailand.

I'd like to share an option that I am exploring: active retirement in Southeat Asia. It has long been popular for Japanese retirees to retire in Thailand; the largely Buddhist culture is familar to Japanese, and their yen buys so much more in Thailand than it does in high-cost Japan. So in a sense, we're simply following a path that is already familar to developed-world Asians: retiring (or spending part of the year) in culturally diverse, low-cost Southeast Asia.

Cost/Benefit ComparisonsAs with retirement facilities in the U.S., there is a wide spectrum of services offered in Southeast Asian facilities. This makes it somewhat difficult to make apples-to-apples comparisons. In the U.S., retirement facilities generally break down into three basic types: -- Assisted living, for people who are able to live independently in their own room or apartment. The facility provides meals, nursing care, housekeeping and activities. According to the U.S. Department of Health & Human Services' Agency for Healthcare Research and Quality (AHRQ), "assisted living denotes a type of residential long-term care setting known by nearly 30 different names." -- Nursing home, which provides skilled nursing home care for those with chronic conditions such as dementia. -- Continuing care retirement community (CCRC) which provides a continuum of care so the residents don't have to move when they need skilled nursing home care. In researching costs in the U.S., I've found the industry is very cagey about the costs of their facilities. I have yet to find a U.S.-based facility that posts its prices online. Various surveys from organizations such as longtermcare.gov have found the average cost for care in an assisted living facility (for a one-bedroom unit) in the U.S. is $3,293 per month. AARP (American Association of Retired Persons) hosts a state-by-state data base of costs for Assisted Living (Private Room); the average cost is around $45,000 per year ($3,750). Other studies have found the national average is $3,600/month, with a range of $2,525 to $5,745 per month. Nursing homes and CCRCs either cost more per month or require a significant buy-in of cash that can range from $50,000 to $500,000 per retiree. Undoubtedly there are U.S.-based bargain facilities out there, but the available data shows that the SE Asian assisted-living facilities listed on the FRA Retirement Solutions site cost about one-third of equivalent care facilities in the U.S. As with assisted living facilities in the U.S., the two facilities in Indonesia (Bali) do not cover hospitalization/medication costs. One offers a close relationship with a nearby modern hospital. (Some insurance plans reimburse overseas medical expenses; you may want to research how your current healthcare insurance addresses overseas care.) In general, medical care is paid in cash in Asia, but the costs are a fraction of healthcare in the U.S. In many case, what costs $10,000 in the U.S. might cost a few hundred dollars in Southeast Asia, often using the exact same equipment (MRI, etc.) as in the U.S. Many people visit Thailand for medical tourism; my wife has had dental work and skin care performed in Thailand for a fraction of the cost of equivalent services in the U.S. We've found the facilities and staff are top-notch--and many others have had similarly positive experiences. The care facility in Chiang Mai (Thailand) offers the equivalent of skilled nursing care for those with dementia and other chronic conditions. One European commenter on a forum estimated that the equivalent care in Europe would cost about 6,000 euros a month. Equivalent care in the U.S. ranges from a low of $4,800 to $6,000 and up per month. The difference is the cost of living and labor in SE Asia. For all the reasons I've covered for years, labor costs continue marching higher in North America and Europe when we look not at wages but at total compensation costs paid by employers.

Though I haven't visited these facilities personally, one reason why they're attractive is that they offer short stays (daily or weekly rates) so anyone who's interested can check them out while on vacation in the region. Please note I am not recommending any particular facility--I am simply presenting the option of retirement (or partial retirement) in Southeast Asia. As we all know from reading Yelp reviews, three people can go to the same place at the same time and share the same experience, and come away with three completely different views. The only way you can find out if this option is on the table for you personally is to go visit the region, country and facility for yourself. This is easy to do, as these areas are well-developed tourist destinations. Longtime readers will know my preference for hybrid work. These options open the door to hybrid retirement: a low-cost retirement that enables travel that would otherwise be unaffordable, and perhaps living part of the year in Asia and part of the year in the U.S. or Europe.

Hybrid RetirementBy hybrid retirement I mean a mix-and-match of various retirement strategies and options. The best way to explain it is to offer some examples: 1. Retire in SE Asia to save a nest egg. Let's say a person has a total retirement income of $3,200/month--enough to pay for assisted living in the U.S., but little else: no travel, no visits to adult children and their kids, no money to help grandkids with university expenses--it's a spartan existence when one's income barely covers the basics. If that person retires in SE Asia for 10 years of their total retirement, they can save roughly $2,000/month, since retirement in SE Asia can cost less than $1,200/month. Over 10 years, this adds up to roughly $24,000/year X 10 years = $240,000. This is a strikingly substantial sum that can be saved in retirement. These savings enable a set-aside for future medical costs, travel, visits to the family, and if the person wants to end their retirement in the U.S., the down payment to buy into a continuing care retirement community (CCRC). 2. A flexible retirement in SE Asia. Since there's no buy-in (as with CCRCs), a person could spend a year or two in Bali and then move to Thailand for a year or two. 3. An elderly retiree and his/her adult offspring could spend quality time together. Given that many people are living into their 90s, it's easy to foresee adult children who are retired at 65 wanting to spend time with their aging parents (85+) but without being burdened with day-to-day care (not easy when you yourself are of retirement age). Since the cost of retirement and skilled nursing care is so much less in SE Asia, this option becomes possible for families of limited means. 4. Part-time retirement in SE Asia enables extended global travel. Many people would love to travel in their retirement years, but travel is expensive. Living in SE Asia frees up funds for extended travel. 5. Two retirees who have lost their spouses retiring in the same SE Asian community, without having to sell their homes in North America/Europe. One of the great difficulties with high retirement costs is the either/or decision forced on retirees who own their homes: to afford the buy-in to a continuing care retirement community (CCRC), the retiree must often sell their home. Alternatively, the retiree is stuck at home--they can't afford to retire elsewhere and keep their home, as the expenses for maintaining both are too much. By retiring in SE Asia, a retiree can keep their own home and return to it whenever they want. Consider two old friends whose homes are quite some distance apart. They'd like to see more of each other, but neither wants to sell their home and move. By retiring to the same community in SE Asia, they can keep their homes and all future retirement options open, while being able to enjoy their friendship in a affordable, no-strings-attached SE Asian retirement community. 6. The low cost of SE Asia enables a retiree to bring their family over for a vacation that would otherwise be unattainable. Rather than fly home, a retiree could bring the family to SE Asia for a vacation of a lifetime. There are a wealth of other scenarios that are enabled by affordable retirement in SE Asia. Being able to retire for $1,200 or less per month opens up a variety of options that simply don't exist for retirees of limited means in high-cost countries.

Other ConsiderationsAs we all know, everything in life is a series of trade-offs. No region, nation or facility is perfect. Everyone has to assess and select the trade-offs that make sense for them. Those who can afford to retire virtually anywhere in the world (for example, those with a net monthly of $10,000 or more) have more choices than those with limited income and savings. What we're discussing here are options that are affordable to anyone with an average Social Security pension--a modest sum in the developed world that limits options but is more than enough for a variety of options in Southeast Asia. The first concern for many people is the distance from family and friends at home. This is a legitimate issue, as it takes roughly 10 to 15 hours to reach SE Asia from Europe or North America. But we need to put this in the perspective of time and money required to make the trip. It takes 10+ hours to drive 500+ miles in the U.S., so spending a day on an airliner isn't much more of a commitment than driving all day. As for cost, long-haul flights to SE Asia are cheaper than many people imagine. Depending on the season, air fares are not much more than the cost of lightly traveled routes in the continental U.S. (Try flying to Missoula, Montana, from a distant non-hub airport. After multiple plane changes and time spent waiting for connecting flights, it's can be easier to take a flight to Asia.) Air travel to Asia benefits from keen competition with a variety of international carriers, and low-cost airlines within SE Asia. The psychological distance can be bridged with technologies such as Skype video calls. This technology has dropped in cost (to near-zero) while becoming simple enough for techno-phobic elders to use with a bit of practice. SMS-texting, email and video clips all enable close connections. Unlike CCRCs and other costly retirement options, there's no financial limits on freedom of movement in SE Asian retirement choices. If a retiree decides they want to spend time at home, they buy a ticket and fly home. For those interested in exploring the idea, there are plenty of resources online. For example, here's an excerpt from a recent U.S. News & World Report article: Southeast Asia is a remarkably beautiful and diverse region that is becoming much more welcoming to Western retirees. Southeast Asias big appeal for foreign retirees is the cost of living. Several countries here are among the worlds cheapest places to retire. Your money goes much further in this part of the world than in the United States or any other Western country, but that does not mean that the standard of living is necessarily lower. It is possible to stretch your retirement nest egg to enjoy a better lifestyle in Southeast Asia than you could afford anywhere else in the world. English is widely understood throughout the region, and it is an official language of the Philippines and parts of Malaysia. The majority of people you come into contact with in these two countries are fluent in English. Additionally, English is a required subject at schools in every country in Southeast Asia. Urban areas and many small towns have enough English speakers that communication rarely presents a significant barrier. Going to a retirement resort/care facility is a lot easier than sorting out all the issues yourself. The resort has English-speaking staff (at least some, perhaps not all), and can help you with issues such as visas, etc. While it's certainly possible to rent a flat and start living in SE Asia on your own, it's less hassle to live in one of these facilities that are Westernized islands in a culture which remains quite different from North America and Europe. The retirement facilities listed on the FRA website are located in favored tourist districts such as Bali and Chiang Mai. The local people are accustomed to dealing with foreigners; many depend on tourism for their livelihoods. Meeting other Westerners is easy in these locales.

In most locales, Americans of every ethnicity will be in the minority. Asian-Americans may well pass for local residents, at least until they start speaking. My wife is Asian-American(born in Hawaii), and people in Asia invariably start speaking to her in their language: Mandarin, Vietnamese, Thai, etc. Though she may look local, she is still a minority culturally. Having been the only haole (Hawaiian for Caucasian) in a variety of settings, I can reassure you that you get accustomed to it relatively quickly. If you're gracious and spend a bit of money in local shops, you'll quickly become part of the local landscape. As a general rule, the cultures of Southeast Asia respect and cultivate restraint, patience, a ready smile, graciousness, politeness and a calm demeanor. Making loud demands, expressing anger or impatience, refusing to pay for goods rendered, crumpling up money and throwing it at clerks, etc., are all extremely rude and counter-productive. While there are disagreeable people and situations everywhere, living in a culture where the default setting is public politeness and a smile is generally a pleasure.

One of the great advantages of Southeast Asia is the low cost of transport: air, rail and bus are all very cheap by Western standards. Hong Kong, Japan, India and other Asian destinations are much closer once you're based in SE Asia. Outside the oasis of the resort, you can expect to experience occasional uncertainties when you're not quite sure what's going on (for example, is the bus late, or has it been canceled, etc.), having to wait for services, being asked for small money for services you assumed were free, and a variety of other things that are typical in places where customs are different from those in Western countries and visitors are typically much wealthier than the locals. Adapting is largely a matter of aligning expectations with these realities. Typically, a smile, a bit of patience and small money moves things along in the desired direction. Political unrest is a possibility in some SE Asian nations. Pitched protests in Thailand's capital a few years ago made many tourists think twice about visiting Thailand, but as a general rule, political/civil unrest is limited to specific districts in the capitals. If you avoid those districts, you're unlikely to have any direct experience of unrest.

Unlike other regions in the world, Americans and Westerners are rarely viewed as the source or cause of domestic political conflicts. Political unrest is typically the result of longstanding fault lines in the political structure, society and economy of the nation. Areas outside the capital that depend on tourism are rarely affected. Most people are anxious to go about their normal business and make visitors feel welcome. Though the region experienced terrible turmoil in the 1960s (the Vietnam War, coups, revolutionary movements, etc.), its recent history has been remarkably peaceful. As for crime, most visitors and foreign residents report they feel safer on the streets in Southeast Asia than they do in many Western cities. SE Asian nations prohibit the ownership of firearms, and while petty theft is a fact of life everywhere, the usual common-sense precautions are generally sufficient to avoid crime in SE Asia. Southeast Asia is easily one of the most diverse regions on Earth, in terms of national boundaries, ethnicities, faiths, cuisine and cultures. Yet it is bound by cultural mores that favor social politeness and tolerance--values that appeal to us all.

SummaryI'd like to summarize a few key points in this discussion: 1. What we've been told are financial certainties are melting into thin air. 2. Financial repression--zero interest rates, capital controls and higher taxes on retirement income--are realities that are more likely to get worse than vanish. 3. Medical costs are soaring in the West due to rising labor costs and cartel pricing (pharmaceuticals and hospital chains in the U.S.). Co-pays are increasing and options for those with limited means are declining as the government slashes fees paid via Medicaid and other programs. 4. Medical tourism to SE Asia is growing as costs are a fraction of prices in the U.S. and the staff and equipment are on par (or better) than Western facilities. 5. The cost of retiring to an assisted living facility in SE Asia is roughly one-third the average cost of assisted living facilities in the U.S. 6. This enables options for limited-means retirees that would not be open to them were they to retire in the U.S./Canada/Europe. 7. Western currencies (especially the U.S. dollar, for all the reasons I have covered for many years) will likely increase their purchasing power at the expense of emerging-market currencies such as those of SE Asia. As the USD strengthens, it buys more in SE Asia. In effect, retirees with USD will be earning more even if their income in USD remains the same as the USD appreciates against local currencies.

Reader Comments

From Derek, who leads a hybrid life, working part of the year in California and

living the rest of the time in Thailand:

As I learn more about specific options for retiring in Southeast Asia, I will post more here. For more detailed information on the five current retirement community options, visit the FRA Retirement Solutions site.

Noble Care - Malaysia Our major focus is to support elderly people with extreme and multiple disabilities, who need special treatment and experienced services. We provide independent living, assisted living and total nursing care. If you're interested in receiving a quarterly newsletter of additional information on retiring in SE Asia, here's the sign-up form. Your name and email will remain confidential and will not be given to any other individual, company or agency.

|