What Few Expect: Inflation Will Surge, Destabilizing the Status Quo

October 4, 2017

Few seem to ponder what global shortages in key commodities might do to prices.

If there is any economic truism that is accepted by virtually everyone, it's that inflation is low and will stay low into the foreseeable future. The reasons are numerous: technology is deflationary, globalization is deflationary, central banks will keep interest rates near-zero essentially forever, and so on.

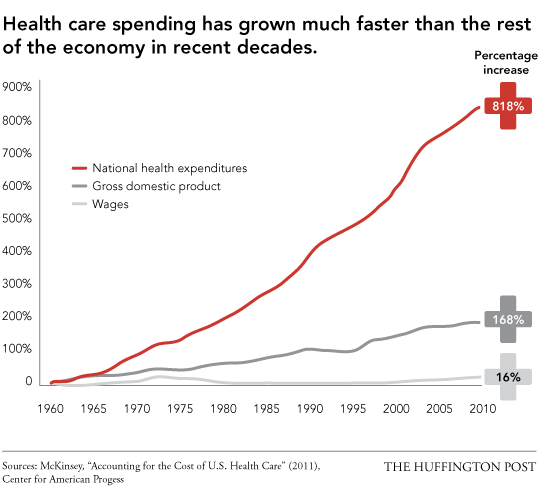

Just for laughs, let's look at healthcare, almost 20% of America's entire economy, as an example of low inflation forever. If being up over 200% in the 21st century is low inflation, I'd hate to see high inflation.

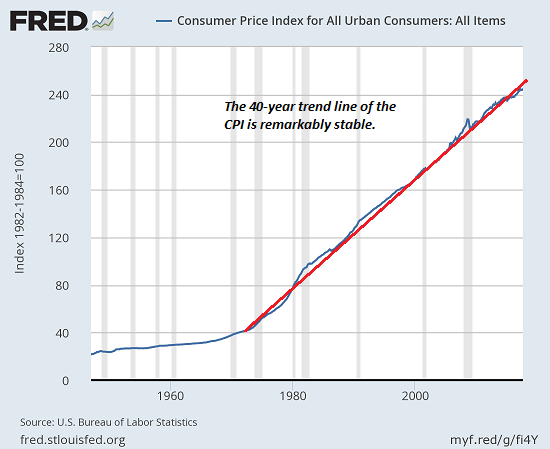

Here's the official Consumer Price Index (CPI), which as many have noted, severely distorts real-world inflation by claiming big-ticket items such as college tuition and healthcare are mere slivers in household budgets.

Note the remarkably stable trend line in CPI over the past 40 years. This certainly doesn't shout "inflation is near-zero and will stay low indefinitely."

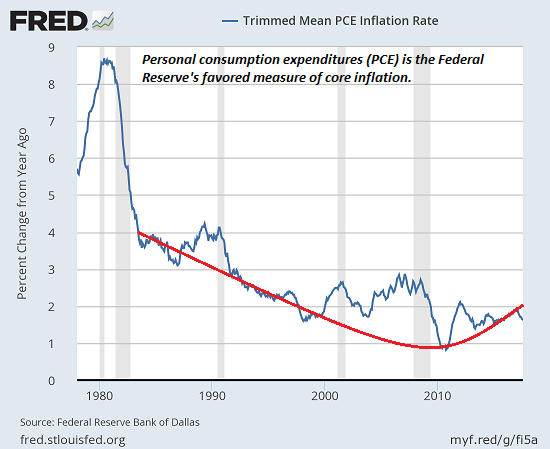

Here's the PCE, Personal Consumption Expenditures, the Federal Reserve's favored measure of core inflation. Let's put it this way: either the PCE is real and the CPI is false, or vice versa; they can't both be accurate measures of real-world inflation.

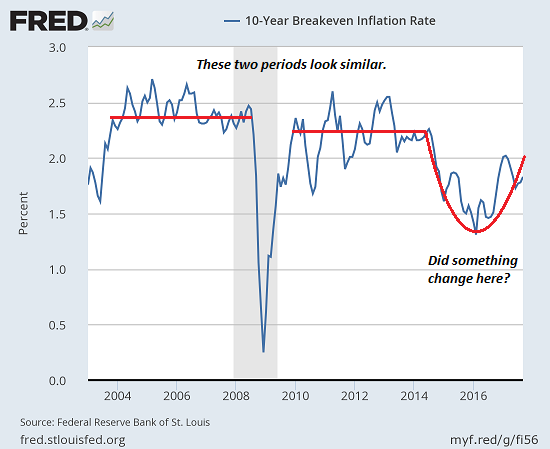

Here's a look at the annual rate of inflation. The go-go years prior to the Global Financial Meltdown of 2008-09 and the years of "recovery" 2010 to 2014 look very similar: some modest volatility between 1.7% and 2.5% annually.

But something changed in 2015-2017. The wheels fell off and then inflation turned up. Maybe it was nothing, maybe not. Let's turn to a chart of asset inflation for a different perspective.

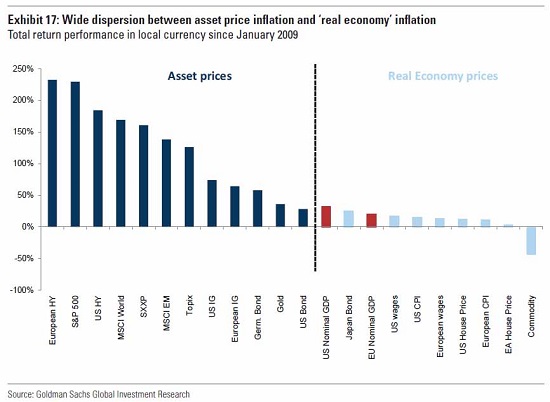

Courtesy of Goldman Sachs, here is a chart comparing asset inflation with real-world inflation. Note how assets have soared while real-economy measures have barely edged higher--commodities actually fell in price.

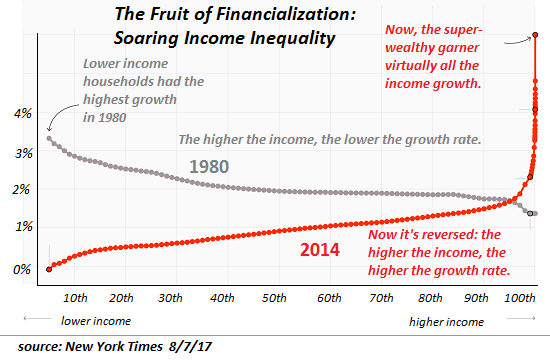

Now let's look at where the gains of the "recovery" were concentrated: in the hands of the few in the top .5%. This chart depicts the unprecedented concentration of income gains in the very apex of the wealth-power pyramid. Needless to say, very little trickled down to the bottom 90%, and even the top 9.5% received mere crumbs.

So what do these charts tell us about future inflation prospects? To the conventional punditry, they suggest more of the same: higher asset valuations, low real-world inflation and near-zero interest rates (courtesy of central bank purchases of bonds and other financial assets).

I beg to differ. To me, these charts suggest real-world inflation is about to take off in the next 5 years, surprising everyone who expected more of the same. My reasoning is simple:

The leadership of the Status Quo has a simple choice: continue with more of the same, enriching the top .5% at the expense of everyone else, and face a political firestorm of upheaval, instability and insurrection, or start funneling the trillions of dollars, yen, yuan and euros that have been channeled into the hands of the few into the hands of the many.

The policy of funneling fresh cash into the hands of households has a number of variations: negative tax rates (lower income households get a hefty tax rebate annually), Universal Basic Income (UBI--every adult gets a monthly cash stipend), QE for the people (the central bank buys special government bonds that eliminate all student loan debt), and so on.

Where virtually all central bank monetary stimulus over the past 8 years went into assets, QE for the people would go right into household bank accounts where most of it will be spent in the real economy.

The incomes of the bottom 90% have gone nowhere for 8 long years. No wonder real world inflation has been capped outside of housing, healthcare and higher education. (Never mind these are the dominant expenses for the majority of households.)

So what happens when fresh trillions start flowing into the real world economy instead of into assets? If history is any guide, inflation picks up. Toss in some global shortages in key commodities and the fuel for inflation will be ready to ignite.

One part of the inflation will stay low indefinitely story is there's an abundance of everything: grain, oil, natural gas, copper, bat guano--you name it, the world is awash in the stuff.

Few seem to ponder the possibility that this surplus of everything might be temporary, a brief run of extraordinary luck rather than a permanent abundance. Few seem to ponder what global shortages in key commodities might do to prices.

Whether you call soaring prices inflation or not, the result is the same: the purchasing power of currency declines. Every unit of currency buys less of whatever is no longer in surplus.

The funny thing about inflation is that it's not a problem that can be solved by creating trillions more dollars, yuan, yen and euros out of thin air. Issuing mountains of new currency actually increases inflation.

Oops. Our only "fix" is to issue trillions more in new currency and credit. If that

doesn't fix the problem, the toolbox is empty.

If you found value in this content, please join me in seeking solutions by

becoming

a $1/month patron of my work via patreon.com.

Check out both of my new books, Inequality and the Collapse of Privilege ($3.95 Kindle, $8.95 print) and Why Our Status Quo Failed and Is Beyond Reform ($3.95 Kindle, $8.95 print, $5.95 audiobook) For more, please visit the OTM essentials website.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Barney S. ($50), for your outrageously generous contribution to this site -- I am greatly honored by your steadfast support and readership. |

Thank you, Charles D. ($5/month), for your superbly generous pledge to this site -- I am greatly honored by your support and readership. |

Discover why Im looking to retire in a SE Asia luxury resort for $1,200/month. |