| |

Real Estate: Disconnect from Reality

(April 23, 2007)

Let's launch "Disconnect from Reality" Week with that perennial favorite, real estate.

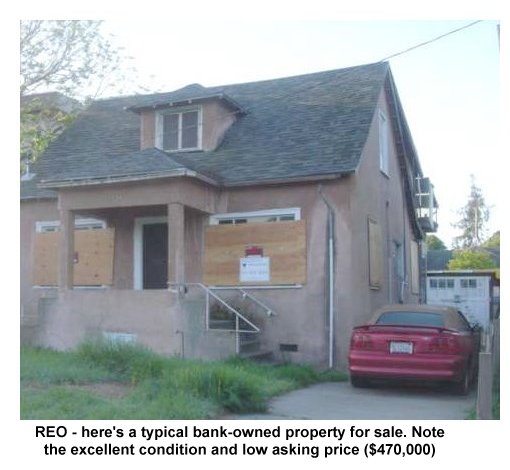

And as a poster child of that disconnect, how about a boarded-up 100-year old

"fixer-upper" in a mediocre neighborhood for $470,000?

Here are the vital statistics from the listing:

List Date: 04/16/07

Location: 1734 BANCROFT WAY, BERKELEY, CA 94703

Bedrooms: 3

Bathrooms: 1+

Price: $470,000

Approx Square Feet: 1315

Approx Lot Feet: 4120

Approx Lot Acres: .09

Approx age: 103

MLS#: 40258589 EBRDI

Disclosures: First Right of Refusal, Rent Control, REO/Bank Owned

Here's what this beauty would cost the proud new owner

(mortgage estimate as per the listing):

Assuming 10% ($47,000) down:

Mortgage of $423,000 at 6.2% fixed-rate 30-year term: $2,591/month

Insurance: ~ $110/month; subtotal = $2,700/month

Property taxes (high-tax Calif) $1,000/month, subtotal = $3,700/month

$100,000 equity line of credit to fund remodeling ($200K is a safer bet, but we'll

assume new owner is handy): $600/month until re-sets kick in

Total reasonable estimate of core monthly expenses: $4,300/month

total rental income (if house were to be rented out): $2,000/month

monthly cash loss: $2,300 (before depreciation, etc.)

(Note that the value of the building permit gets added on to the purchase price, so the

total assessed value after the renovation would be about $700,000. Oh, and don't even think about

lowballing the renovation cost--the building department will insert their own "estimate

of fair value" for you, regardless of the actual cost. Hint: it will be high, very high.)

As a business proposition, this is a lousy deal. Assets are supposed to generate

cash profits, not "tax shelter losses" and "gee, on paper, after depreciation, it's only..."

losses. I didn't even include maintenance.

Please note this is 103-year old structure on a crumbling brick foundation in an

earthquake zone. Just fixing the foundation and plumbing/electrical would cost

$100,000. Actually bringing this house up to modern standards would cost about $200,000.

I know this sounds insane to those living in areas where you can still buy a house for

$60,000, but the building permits alone will cost over $10,000. Yes, construction

and remodeling are now the "cash cows" of many California cities, and $10,000

might not be enough to cover all the permit fees.

An architect friend of mine tells me he's designing a modest addition in the Berkeley

Hills, and the budget is $300,000. Kitchen remodels in excess of $100,000 are now common.

Note that this is an REO: "real estate owned" by a lender. As this becomes more common

(see links below), we can anticipate more such "distressed properties" being listed at

absurd prices.

Frequent contributor Jed H. recently outlined the probable chain of events as reality

rudely intrudes on fantasy:

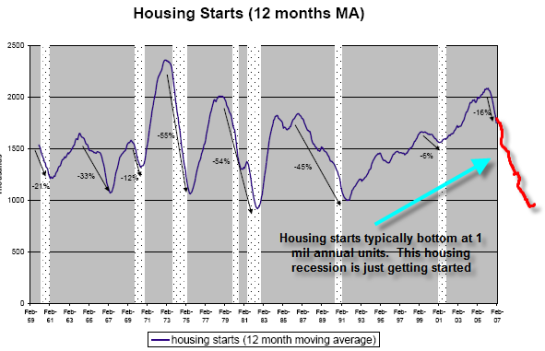

Just the "First Inning"--Very interesting Graph of Housing Starts:

source: California Housing Forecast

source: California Housing Forecast

original chart by Dr. Nouriel Roubini and Christian Menegatti, www.rgemonitor.com

The events would unravel like this:

A) Credit Crunch, from SubPrime Lending Meltdown;

B) Toxic ARMS etc, REFIs of underwater homeowners fail & "Mortgage Lending is Tight";

C) Defaults, REOs, Foreclosures Soar in '07;

D) For Sale Inventory Way UP, to over ~ 8 to 12 month supply;

E) With mostly SELLERS, Few BUYERS, Home Sales Crash;

F) With sky high Inventory, Falling Sales, Prices Slump ~ 10 %;

G) Consumers with Debts @ MAX, forced to CUT Spending, as House ATMs, Closed for Business;

H) With Auto sales down, House sales down, Home building Slow,

Durable sales down--USA GDP rate Tanks & goes Negative;

I) Last ASSETS to take the Big Hit--Stock Mkt , Hedgies/ Derivatives

"Blow Up", & DOW/S&P 500 sink by ~ 30 % or more, later this year;

J) FED & Uncle BEN have TWO very BAD CHOICES:

1) Loosen, Inflate the USD, via lower FedFunds--but Dollar Crashes &

Inflation Soars;

2) Fed Funds holds @ 5.25 % or Goes UP, USA Economic Depression

My "Best Guess" is that FED Holds Long as it can, US Economy Crashing,

then FED Opens the Spigots, like ~ 2000 to 2003 (again)

Excellent summary, Jed. Here are a number of recent links which bolster this

outlook:

34 percent of homeowners are clueless about their mortgage

Home Prices Worst Since '94

S&P Housing Index Shows Housing Prices Fall in January Year-Over-Year, Worst Since 1994

Homeowners hit with harsh realities when payments spike

Home equity delinquencies rise 7% in 4Q

Here are a selection of incisive comments drawn from

Credit Bubble Bulletin, by Doug Noland, 3/23/07: (Prudent Bear website)

March 22 – Bloomberg (Jody Shenn): “The subprime credit crunch is beginning to ensnare

even borrowers with good credit. Lenders are increasingly refusing to lend to homebuyers

who can't make a down payment of more than 5 percent, especially if they won't document

their income. Until recently such borrowers qualified for so-called Alt A mortgages,

which rank between prime and subprime in terms of risk. Last year the category accounted

for about 20 percent of the $3 trillion of U.S. mortgages, about the same as subprime

loans, according to Credit Suisse Group. ‘It’s going to be very difficult, if not

impossible, to do a no-money-down loan at any credit score,’ said Alex Gemici, president

of… mortgage bank Montgomery Mortgage Capital Corp. Companies that buy the loans ‘are

all saying if they haven’t eliminated them yet, they’ll eliminate them shortly.’”

March 19 – Bloomberg (Hui-yong Yu): “U.S. homeowners, lenders and investors may lose as

much as $112.5 billion through 2014 as mortgage payments go up on adjustable-rate loans,

triggering defaults and foreclosures, according to a study by mortgage-risk data provider

First American CoreLogic. An estimated $2.3 trillion of adjustable first mortgages were

originated from 2004 to 2006, many of which will begin to reset in two to three years.

As they reset at higher rates, about 1.1 million loans amounting to $326 billion may go

into foreclosure, the study said.”

According to Bear Stearns, subprime loan balances have grown to approach $1.5 Trillion. And

there is another $1.1 TN in “Alt-A” and another $1.4 TN of “Jumbo” loans that have

accumulated in the marketplace.

Much of this risky mortgage exposure now resides in

various securitizations and derivatives (including CDOs). It is, then, today fair to

ponder the facilitating role derivatives played in this huge and destabilizing Flow of

Risky Credit. How significantly did the capacity of Wall Street “structured finance”

to transform a large percentage of these weak Credits into highly-rated and liquid

securitizations (“Moneyness of Credit”) abet the boom in risky mortgage Credit?

Clearly, derivative market risk intermediation was integral to the flood of finance into the

subprime space. Marketplace risk perceptions were drastically distorted during the boom,

and we’re certainly seeing similar dynamics at play today throughout corporate and M&A

finance.

Excerpts from today’s Credit Symposium keynote address by Timothy Geithner, President of

the New York Fed: (worth reading)

Credit market innovations have transformed the financial system from one in which most

credit risk is in the form of loans, held to maturity on the balance sheets of banks, to

a system in which most credit risk now takes an incredibly diverse array of different

forms, much of it held by nonbank financial institutions that mark to market and can take

on substantial leverage.

U.S. financial institutions now hold only around 15 percent of total credit outstanding

by the nonfarm nonfinancial sector: that is less than half the level of two decades ago.

For the largest U.S. banks, credit exposures in over-the-counter derivatives is approaching

the level of more traditional forms of credit exposure. Hedge funds, according to one

recent survey, account for 58 percent of the volume in credit derivatives in the year

to the first quarter of 2006.

Financial shocks take many forms. Some, such as in 1987 and 1998, involve a sharp increase

in risk premia that precipitate a fall in asset prices and that in turn leads to what

economists and engineers call "positive feedback" dynamics. As firms and investors move

to hedge against future losses and to raise money to meet margin calls, the brake becomes

the accelerator: markets come under additional pressure, pushing asset prices lower.

Volatility increases. Liquidity in markets for more risky assets falls.”

This remains the most incredible period in financial history. A strong case can be made

that the traditional Credit Cycle has turned – an especially momentous development

considering the scope of previous Mortgage Credit Bubble Excesses and attendant economic

imbalances. Can we, then, infer that the Liquidity Cycle has similarly turned? Are they

not one and the same? Well, in the age of contemporary Wall Street securities finance,

they are not. And the case that the Liquidity cycle has turned is not yet as convincing.

To this point, there are few indications of waning derivatives growth; or a slowdown in

financial sector expansion; or a meaningful moderation in global Credit growth. Worse

yet, there is ample evidence of Wall Street’s keen desire to push the envelope of

leveraged speculation in preparation for the Credit slowdown-induced Fed

easing cycle. Perhaps U.S. and global markets this week demonstrated to the Fed why

Liquidity and speculative excesses should be the focus. Central bankers should be in no

rush to appease. Cutting interest rates would likely temporarily accomplish a few things,

but promoting a Smooth Flow of Credit would definitely not be one of them.

And for a cogent summary of the coming housing debacle/decline, frequent contributor U. Doran sent in

this story from the Pimco website, and one from Safe Haven:

U.S. Credit Perspectives--"Still Renting":

We know from the NASDAQ bubble that once risk appetite changes, prices can shift violently

in the other direction. Housing is different from equities because it is much less liquid;

therefore price adjustments take more time. In a down housing market, the gap between

buyers and sellers widens, and volumes fall. Buyers pull back and sellers take time to

realize their listing prices are too high.

Eventually, housing prices in entire

neighborhoods will get reset downward by the weakest hand. Just as prices went up and

everyone in the neighborhood applauded the newest neighbor who bought at the top, prices

will likely start to fall as financially-stretched home owners and speculators sell, and

are forced out of the market. As this process unfolds, risk appetite for housing should

take a sharp turn for the worse. This year’s weak start to the traditionally strong spring

selling season suggests we have indeed entered the “buyer’s strike” phase of the cycle.

Recession Imminent (from Safe Haven, by Paul Kasriel)

As homebuilders' stocks rise--"the worst is over" yet again--and as inventory

of unsold houses piles up, we are witnesses to a grand disconnect of hope/perception from

reality. It is merely an observation, not a value judgment, that reality eventually

overwhelms perception.

For more on this subject and a wide array of other topics, please visit

my weblog.

copyright © 2007 Charles Hugh Smith. All rights reserved in all media.

I would be honored if you linked this wEssay to your site, or printed a copy for your own use.

|

|