|

|

| weblog/wEssays archives | home | |

|

Want to Know When Housing Has Bottomed? Here's How (April 23, 2008) The shills and cheerleaders are already calling the "bottom" in housing prices. It's worth recalling that these are the same Nostradamuses who declared the last "bottom" in 1991, 1992, 1993, 1994, 1995 and 1996--and voila, they were finally right seven years into the slide (1997). Want to know when the "bottom" is finally in? The "bottom" will be close when buying real estate make sense as a sound business proposition. This kind of foreclosed/distressed property is not even close to being a decent business proposition:

If you want to spawn "The Creature From the Black Lagoon," then by all means fill up this abandoned McMansion's pool:

What's a sound business proposition? making a profit from day one, without the aid of any tax shenanigans. At the real bottom in real estate cycles, you can buy a house or apartment and rent it out at market rates--and make a profit on day one in cash-accounting terms. If you can't rent the property out for a profit from day one, it isn't the bottom. Untold numbers of inexperienced speculators bought homes with the untested notion that they could "rent it out" ("buy to let" in the U.K.) if flipping it for vast profits didn't work out. Let's go through the actual expenses of an absentee landlord/owner: 1. down payment. The down payment isn't "free": you could be earning 3% or so in a money market/T-bill. As pathetic as that is, it's not zero. If the down payment isn't earning more than 3%, then why bother buying real estate? 2. mortgage/borrowed money. This is self-evident. But wait--there's more! 3. property management. Even if you do it yourself, it's not "free"; nobody's time is free. The standard fee is abour 5-6% to handle the rental and collect the rent. This does not cover gardening, upkeep, repairs, etc.--those are extra. Plus somebody has to respond to tenant complaints. That's not free, either. 4. property taxes. Like weeds, these just grow constantly. Don't forget the special assessments. 5. advertising/marketing. Sure, craigslist is free--but somebody has to meet prospective tenants, process their rental applications, check their credit, etc. Maybe that's included in your property management fee, maybe not. 6. auto/truck expenses. hauling stuff to the dump and driving to Lowes/Home Cheepo isn't free. 7. cleaning and maintenance. When the tenant moves out, the place isn't perfect, no matter what you hope/what the lease says. (And how good is that lease, anyway? Better add a couple hundred bucks for attorney's fees if you're smart.) Ah, maintenance. That covers quite a few costly items: appliances that die, carpets that wear out, hardwood floors stained by cat pee/soggy house plants, furnace filters, paint that gets grimy, etc. Many pros figure 10% of the rent goes (eventually) to repairs/maintenance. If you stipulate the tenant takes care of the yard, be prepared to own a slum. 8. Insurance. It's nice if you could get homeowner's coverage, but you can't--your rental is a commercial property. Now you need liability coverage, too, not just fire insurance. Nothing like a tenant "tripping on the broken concrete" to remind you of that. 9. repairs. A building is a living thing which breaks down over time--expecially if it's a cheaply built, poorly constructed McMansion/condo. Windows break, paint peels, roofing leaks, flashing rusts, stairs rot, crummy veneer flooring delaminates, the list is endless. 10. utilities. Many landlords pay for water, but maybe you won't. 11. fees and licenses. Your city or county probably wants some business license fees from your landlording business. One way or another, there's sure to be some fees or licensing costs somewhere. Maybe the city inspects the property for safety--and bills you. Some agency or municipality is sure to assess you something beyond property tax. 12. Vacancies. Yes, some premium properties are rarely empty, but don't fool yourself--the pros know vacancies are a fact of rental real estate life. Most figure 5% (for premium properties) to 10% (for less than premium). OK, so let's say a rental property rents for $1,500/month in the real world. In my neck of the woods, this would be a small 2-bedroom, 1-bath bungalow. Maybe in your area, it would be a 4-bedroom, 2-bath home. Regardless, the key is to add up the real-world expenses and see if owning the property pencils out as a business proposition. Due to variations in property tax rates, it's difficult to set a generic cost to owning a house. And of course, the property tax drops along with the value of the property. To keep things simple. let's say the rental costs $300,000 and the owner bought it with no down payment. According to zillow.com's mortgage estimation tool, a $300K mortgage at 6% (30-year fixed-rate) costs $2,124/month or $25,500 a year. A rough guesstimate of all the non-mortgage expenses listed above for a $300K property comes to between $8,000 and $9,000, so let's take the lower number. (Insurance and other costs vary widely, too.) $8K + $25K = $33K in expenses against $18K in annual income. A $15,000 per year loss is not a good business proposition. So let's lower the price to $200,000. The mortgage drops to $18,000 a year, and the lower valuation shaves $1,000 off the property tax. So $7K + $18K = $25K versus an annual income of $18K. A $7,000 annual loss is a lousy business proposition. So let's drop the price down to $150,000. The mortgage drops to $1,224/month or $14,600 annually. Let's shave another $1,000 off the property tax (too bad for the city/ county depending onrising property tax revenues) and assume all non-mortgage expenses can be reduced to $6,000 per year. $14.5K + $6K = $20.5K versus $18,000 rental income: we're down to a $2,500 annual loss. So let's ratchet the pruchase price down to $130,000. Now the mortgage is only $13,000 a year and the non-mortgage expenses, well let's say they're down to $5,500 a year. $13K + $5.5K = $18.5K against $18K in rental income. Hey, we're finally getting close to breakeven here. An actual, honest profit is just around the corner. So let's assume a purchase price of $126,000 for the house which rents for $1,500 per month ($18,000 a year). Now at long last we can anticipate a modest profit--unless of course the property sits vacant more than a few weeks out of the year. Real estate investment pros have a rule of thumb for establishing fair value of rental property. Multiply the annual gross rental by between 6 and 10; that gives you a "business" estimate of the value of the rental. In not-so-great neighborhoods, a multiple of 6 is standard; a house that rents for $18,000 a year would thus be worth $108,000. A moderate neighborhood would fetch a multiple of 7--magically, our $126,000 number. Premium neighborhoods (where it is presumed you can raise the rents) may be worth 8 to 10 times gross annual rents. So even in a wonderful neighborhood with terrific schools and other assets, a house renting for $18,000 a year is worth no more than $175,000--as a business proposition. Of course you can pay more, but you're paying for "blue sky," not an asset that can be sold on the open market as a business proposition.

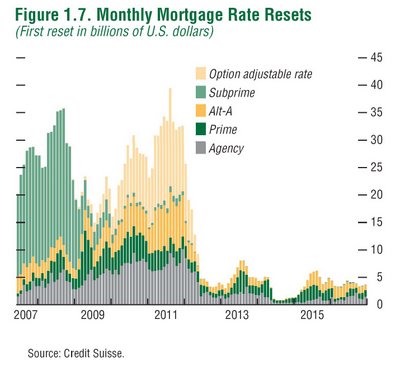

And when will that occur? If we look at the chart of mortgage re-sets, we see the non-subprime re-sets really start rising in 2009 and keep increasing all the way through 2011 before finally falling off in 2012. Since we can also anticipate the recession will be neither shallow nor short, there are ample reasons to expect the inventory of unsold homes to rise in inverse proportion to the number of qualified, willing buyers. What does an oversupply of merchandise (houses) and a dearth of demand/buyers lead to? Falling prices. It's easy to multiply a number by 7. That big house down the street that rents for $3,000 a month/$36,000 a year? At the real "bottom," that house will sell for about $250,000 (or less). That condo which rents for $1,200/month/$14,000 a year? $100,000, tops. And so on. Can real estate decline in value? Yes. At what point does it make sense to buy real estate as an investment which bests other business opportunities? When it makes a profit on day one, after all expenses, not just mortgage/property tax/insurance. And what's a time-tested method of figuring that price? Seven times gross annual rental income. Calling the bottom won't be that difficult; it requires only patience and simple arithmetic. One caveat: if a property can't be rented at any price, its value is essentially zero.

copyright © 2008 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |

There are many other variables, of course; if interest rates climb, then the cost of the

property has to decline further to make investment sense. Nonetheless, we can say with

great historical accuracy that housing of any sort which can be purchased

for a multiple of 6 or 7 is a sound investment. History suggests that only when

properties are selling for these low multiples can we discern the "bottom."

There are many other variables, of course; if interest rates climb, then the cost of the

property has to decline further to make investment sense. Nonetheless, we can say with

great historical accuracy that housing of any sort which can be purchased

for a multiple of 6 or 7 is a sound investment. History suggests that only when

properties are selling for these low multiples can we discern the "bottom."