|

|

| weblog/wEssays archives | home | |

|

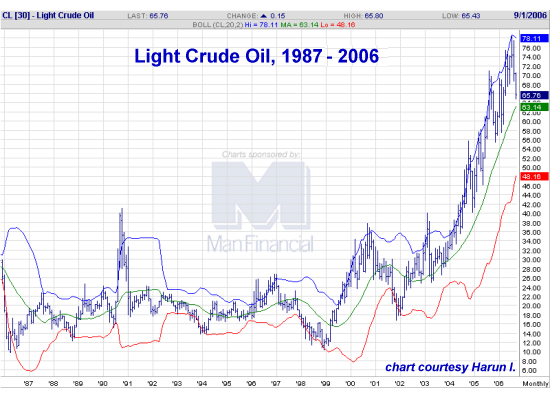

Living in Extraordinary Times (August 30, 2007) We are living in extraordinary times. No, not because of the iPod or other electronic frippery. We are the last humans who will experience cheap petroleum. Yes, Peak Oil, depletion, whatever you want to call it, looms just ahead, and here is the evidence. Frequent contributor/resource analyst U. Doran recommended these articles, which make an ironclad case for declining production which will soon be unable to meet global demand: World Oil Forecasts Including Saudi Arabia - Update Aug 2007 World total liquids production (Fig 1) remains on a peak plateau since 2006 and is forecast to fall off this peak plateau in 2009. According to the IEA, the current peak production of 86.13 mbd occurred on July 2006 and only one year later, June 2007 total liquids production fell to an unexpectedly low 84.28 mbd. As long as demand continues increasing then prices will also continue increasing."All the Canaries Have Stopped Singing" transcript of Interview with Author of "Twilight in the Desert" Matthew Simmons, with Jim Puplava (Financial Sense) Longtime readers will find nothing new here; I have posted numerous charts and links over the past two years popping every fantasy that shale oil from Canada is the solution, there is plenty of oil in the ground, etc. etc. Yes, there may well be--but it's no longer cheap to bring to the surface. So what's this mean to you? That is up to you. Can this knowledge be leveraged into financial gain by us small-fry? Well, glance at this chart of oil 1987-2006 and tell me if investing in the petroleum industry in 1999 or 2002 was an investment which paid handsome returns:

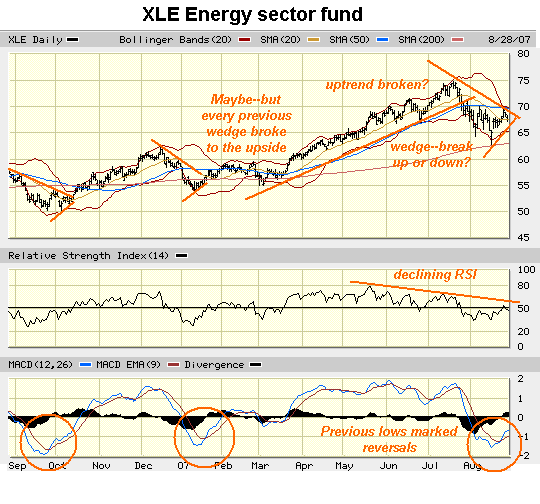

Is this advice? No. It is simply information. There are no easy answers in the financial world, or indeed, in any world. As I often observe: If it is were easy, we'd all be millionaires. You cannot become wealthy by following the simplistic "BUY!!" recommendations of Fools or Pundits or Screaming Entertainers. You have to acquire financial/investment self-knowledge and knowledge of the world, and then base decisions on that knowledge. So what does the end of cheap oil mean to you? Perhaps it means you sell your V-8 truck and get a 4-cylinder version. Maybe it means you sell your house in the exurbs and move closer to your job/school, etc. (renting, of course, until housing falls 50+% from today's prices). Maybe you start looking at candidates' stands on energy policies. Or maybe you decide to switch some 401K funds into an energy-centric mutual fund which invests in both petroleum and alternative energy companies. Maybe you decide to do nothing. That's all up to you. The goal here at OfTwoMinds is to try to make sense of the larger forces at work in our world. How you deploy that knowledge--assuming you don't reject it as wrong, which is also a possibility--is up to you. Advice is cheap, knowledge is dear. That said, here is a chart of the XLE energy sector ETF:

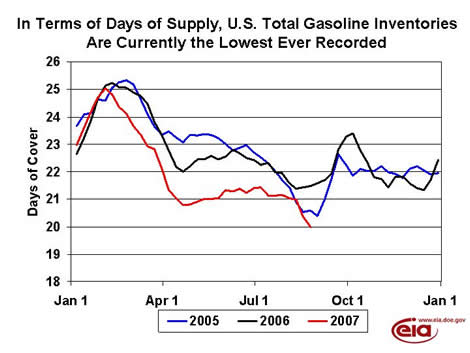

While the fundamental evidence presented in the above articles would suggest higher energy prices are our future, this chart has cross-currents. The declining RSI suggests weakness, while the MACD suggests a bottom may be forming. The 5-month uptrend appears to have been broken, and a wedge formation can be discerned. Wedges tend to break up or down, often in a big move. You could argue for a move down by noting that a softening economy will lower demand, or argue for a move up by noting the rapidly rising demand in Asia and India for petroleum. No one knows what will happen in the future. However, if you put together the information in the Oil Drum article and the interview with Matt Simmons with the data displayed in these charts, you can probably reach some conclusions on the preponderance of evidence. Is oil likely to stay cheap for a long time? There seems to be a lot of "maybe's" and not much hard evidence to support this notion. Is corporate America planning for higher oil costs? The Wall Street Journal issued a special report on August 27, 2007-- Business Goes on an Energy Diet: With oil, gas and electricity prices soaring, companies worldwide are beginning to realize that saving energy can translate into dramatically lower costs. And that means higher profits and happier shareholders -- not to mention a cleaner planet. Still, most companies are moving slowly in implementing these types of energy-saving changes -- if at all.The link requires an online subscription, but you can always read it for free at a library. Late breaking addition: Knowledgeable reader D.F. sent in an unsettling chart of gasoline inventories, with this note and links to source data: As the chart below indicates, not only is the absolute level of inventories low (see Figure 4 in the Weekly Petroleum Status Report), but in terms of days of supply, it is the lowest ever recorded ( the days of supply data goes back to March 1991), reaching just 20 days. This is even fewer days than seen following the hurricanes in 2005.Here is the chart:

To repeat: there is no investment advice offered on this site. All that is presented is data, information and charts which are open to interpretation. Will some canny types look at this and promptly buy gasoline futures, so as to capture the rise in prices which this chart suggests may well transpire? Well, why would anyone sell gasoline futures, when the supply is at multi-year lows? This is not advice, just an observation. If gasoline prices rise sometime in the next few months, you may recall this chart. Here's what the Energy Information Administration had to say in its report This Week In Petroleum (released August 29, 2007): What this means is that while retail prices are not expected to jump sharply on a national average, they are also unlikely to fall dramatically over the next few weeks. Of course, this expectation is based on the assumption that there are no major hurricanes or other non-market events impacting petroleum infrastructure over the next few weeks. (emphasis added) With no storms forming in the Atlantic as of this writing, that should be considered as another bit of good news for drivers.  Lest those reassurances leave an unrealistically warm and fuzzy afterglow, consider this

chart of hurricanes per year.

Lest those reassurances leave an unrealistically warm and fuzzy afterglow, consider this

chart of hurricanes per year.

The rising trendline suggests that last year's complete absence of hurricanes in the oil-patch regions of the Gulf of Mexico was an anomaly which may not be repeated. Poor Dumb Writer Disclosure: I own shares and calls (options) in integrated energy company APC. This is not a recommendation or advice, merely a disclosure that I have long had a financial stake in an oil/gas stock. Thank you, Tom S., ($50) for your extremely generous donation to this humble site. I am greatly honored by your support and readership. All contributors are listed below in acknowledgement of my gratitude. For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2007 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |