|

|

| weblog/wEssays archives | home | |

|

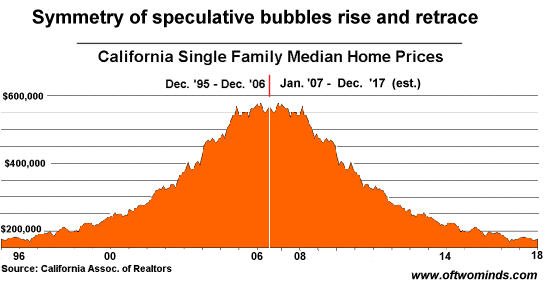

Exhaustion, Jobs and Housing (December 6, 2007) Longtime contributor Cheryl A. proposed an important topic: I hope you'll post on Paulson's five year plan and the effect on the economy. Do you think this will delay the recession projected for 2008-2010?As you know, the "five year plan" (which smacks most weirdly of old Soviet and current Communist Chinese Central Planning at its best/worst) "solves" the "subprime crisis" by having lenders freeze the interest rates and payments for "some" subprime lenders for the next five years--until 2012. All of the obvious objections are contained in the quotation marks above: 1. It is not a "solution to keep homeowners from losing their homes," it's a blatant attempt to keep the lenders/investors solvent by chaining underwater/negative equity owners to the debt-serf machine, i.e. mortgage payments on houses which keep declining in value. 2. The crisis is not limited to subprime borrowers, but to virtually everyone who accepted an exotic, ALT-A, HELOC, adjustable or even fixed-rate mortgage on a property which has declined into negative-equity territory. 3. How the triage works--i.e., Who gets offered the "5-year freeze" and who gets dumped in the "hopeless" ward--is unclear. In all likelihood the triage will work like this: if you're six months behind, you're toast; if you're current, you're golden. But missing from such superficial analyses are two larger factors which will eventually come into play: exhaustion and job losses. Let's start with a chart of how bubbles tend to deflate--symmetrically:

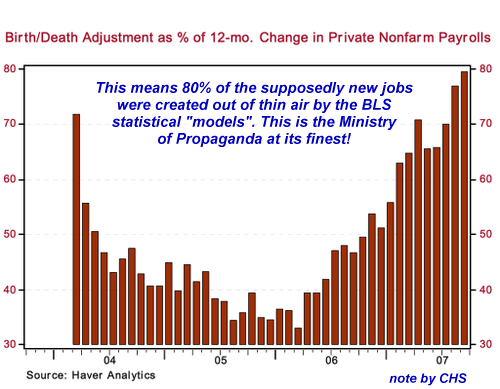

The question posed by this chart (or any chart of a bubble retracing to the mean) is: how long will the "saved" homeowners keep shouldering their mortgages when every year their house is worth less? Humans are selected for basic optimism, and the real estate industry's PR machine will be wedged in high gear for the next five years, proclaiming every Spring that "the market has turned the corner." If you think this cynical, then I invite you to go to any major newspaper's archives and read the real estate industry's eternally positive "market is turning" hype for the years 1991-1997--a stretch of years in which housing declined in real terms every year. So how long will you pay $2,000 a month to "keep your piece of the American Dream" when you can rent the same house for $1,200/month? How many years will that $10,000/year difference be "worth it" if the property value erodes like a half-toppled sand castle buffeted by a rising tide? How about when the gutters need replacing in Year Three of the freeze, and when the water heater blows out in Year Four, and the roof starts leaking in Year Five? How motivated will the beseiged homeowner be to scrape up the money for repairs? The human spirit has limits of endurance, and five years will be plenty long enough to find out just how few people will still believe the "market is turning up" after five years of declines and false hopes dashed/betrayed. There is nothing new about the current real estate bubble deflation except its size; which brings us to the second type of exhaustion: the physical kind. Back in the early 90s (yes, during the last housing deflation period 1990-1997), there were stories of distant exurbs outside Los Angeles slowly being abandoned by newly-minted homeowners who could no longer maintain the grinding 3-4 hour commutes and the destruction of their family life. Parents no longer saw their kids except late at night or yawning at 5 a.m. in the morning; the Potemkin Village of hastily constructed McMansions had no town center and nothing to do, so the kids did drugs and defaced the abandoned houses around them. As property values declined, people gave up and left, preferring to rent somewhere closer to their jobs and to "get their life back." Lastly, consider what happens in the (inevitable) recession just ahead: people lose their jobs. Where will the jobs be lost? Where will they not be lost? Retail: yes. Restaurants: yes. Finance: yes. Manufacturing: yes. Government (as tax receipts plummet): yes. And so on. Even healthcare will not be immune to job losses. As large employers like government and finance/lenders shed workers, those organizations will not be paying health insurance premiums for ex-employees; not only will those unemployed workers no longer be covered, but all the healthcare businesses which were feeding off those well-insured workers will suddenly find themselves on a starvation diet. And if the energy scenario plays out according to supply and demand, as I expect, then global recession will cut demand for petroleum and oil prices will drop from $80-$90/barrel to $40/barrel or even less. If that occurs, even the energy sector may find layoff notices are necessary to protect profits. As those of us who lived through the last "real recession" in 1980-82 (12% unemployment, etc.) recall, job losses quickly spin into a voracious positive feedback loop as layoffs in primary industries trigger layoffs in hospitality, restaurants, entertainment and retail which then trigger declines in tax receipts which then cause horrendous government deficits and "hiring freezes" (a.k.a. layoffs). Unfortunately, as this chart shows, job statistics are so phony it will be hard to tell when job losses are actually gaining momentum until the statisticians are no longer able to mask the carnage.

So what happens to the mortgage in two-income households when one wage-earner loses his/her job? The family hangs on for awhile, doing everything in their power to maintain the huge mortgage payments, but recessions don't end in a month or two; they deepen over time as the positive feedback loop of job losses works its way through the entire economy. Recessions last longer than most people's savings, and so we can anticipate, with much anguish, much more extensive foreclosures, regardless of "Five Year Plans" to freeze payments. Once you're lost your job, a $2,000/month mortgage payments suddenly looms like the summit of Mount Everest right as your oxygen runs out. Thank you, knowledgeable reader Jeff for correcting my error regarding positive and negative feedback loops. Jeff passed on this link as background: Positive Feedback (Wikipedia) Thank you, Ilar Z., ($20), for your generous contribution to this humble site. I am greatly honored by your readership and support. All contributors are listed below in acknowledgement of my gratitude. For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2007 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |