Why the Massive Expansion of "Money" Hasn't Trickled Down to "The Rest of Us"

December 22, 2016

If you create and distribute money only in the apex of the wealth/power pyramid, it can only benefit the few rather than the many.

There are numerous debates about money: what it is, how we measure it, and so on. In recognition of these debates, I'm referring to "money" in quotes to designate that I'm using the Federal Reserve's measure of money stock (MZM).

Nowadays, "money" is often credit. We buy stuff not with currency/ cash, but with credit extended by lenders. The government pays for its programs with borrowed money as well, by selling sovereign bonds and spending the proceeds.

So to get a rough measure of the expansion of "money," we look at money stock and total credit.

There's a third measure: GDP, or gross domestic product. As money and credit expanded, did GDP go up, too? By how much?

GDP is also a flawed measure of value and activity, but once again we'll use it as the conventional measure of economic "growth."

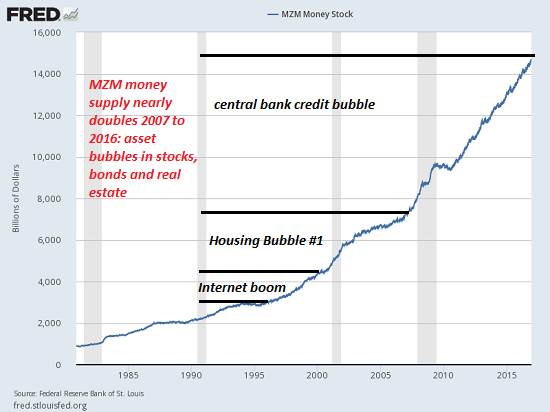

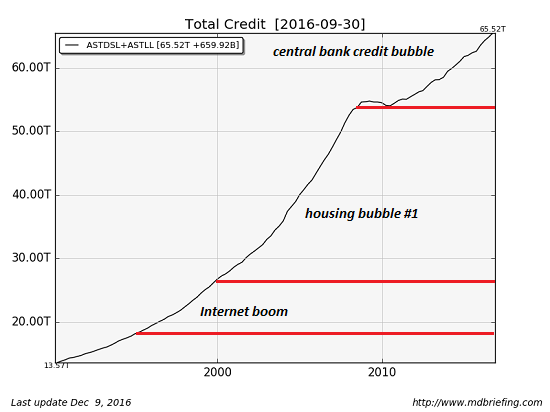

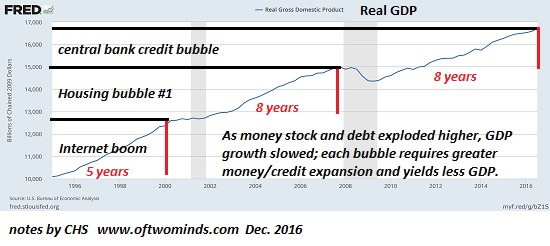

When we glance at money, credit and GDP, we are immediately struck by the disconnect between expansion of money/credit and GDP growth. A relatively modest expansion of money stock and credit was sufficient to fuel a powerful expansion of GDP during the 1995-2000 Internet boom.

The next expansion of GDP--Housing Bubble #1--required an enormous expansion of credit and about double the growth in money stock as the Internet boom.

The current "recovery"--what I term the central bank credit bubble--has required a monumental increase in money stock and a non-trivial expansion of credit.

This is the very definition of diminishing returns: Every expansion of GDP is weaker but requires vastly greater expansions of money stock and total credit.

Longtime correspondent J. Numis identified a key dynamic that few others seem to have noticed: the money has been created in the top of the wealth pyramid of banks, financiers and corporations, and very little has "trickled down" to the bottom 95% in the form of higher wages or increased wealth. Here is J. Numis' comment:

"What we're going through is 'Cyberinflation' which bears no resemblance to hyperinflation, in that way too much ethereal money is out there--but only in the hands of a relative few--thus not debasing its overall value among the populace, in terms of making them believe. Kind of brilliant if you ask me, and a paradigm that nobody is looking for--as it didn't exist heretofore."

This expansion of "money" has inflated asset bubbles, because the wealthy few with access to the new money/ credit have the means to outbid everyone else for productive assets. Some of "the rest of us" have benefited indirectly, as those who own appreciable chunks of stocks, bonds and real estate in the hot areas have seen their net worth rise as the asset bubbles have inflated.

But the benefits of asset bubbles are concentrated in the top 5%, as most of these assets are owned by the top 5%. The next 15% benefits modestly, but the bottom 80% don't own enough assets to get any boost at all.

If anyone wonders why this monumental expansion of "money" hasn't sparked generalized wage inflation maybe one factor is that very little of this new money has trickled down to the bottom 95%.

This is why I contend that If We Don't Change the Way Money Is Created and Distributed, We Change Nothing (December 24, 2015). Every other reform is mere window-dressing.

In my book A Radically Beneficial World, I propose a way of creating and distributing money at the bottom of the pyramid to those who are creating value in their own communities, as opposed to only creating new money in the top of the pyramid and only distributing it to the obscenely wealthy.

No wonder so little "trickles down" to "the rest of us": if you create and distribute money

only in the apex of the wealth/power pyramid, it can only benefit the few

rather than the many.

Join me in seeking solutions by

becoming

a $1/month patron of my work via patreon.com.

Check out both of my new books, Inequality and the Collapse of Privilege ($3.95 Kindle, $8.95 print) and Why Our Status Quo Failed and Is Beyond Reform ($3.95 Kindle, $8.95 print). For more, please visit the OTM essentials website.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Amy W. ($5/month), for your superbly generous pledge to this site -- I am greatly honored by your support and readership. |

Thank you, Vincent W. ($5/month), for your splendidly generous pledge to this site -- I am greatly honored by your support and readership. |

Discover why Im looking to retire in a SE Asia luxury resort for $1,200/month. |