|

|

| weblog/wEssays archives | home | |

|

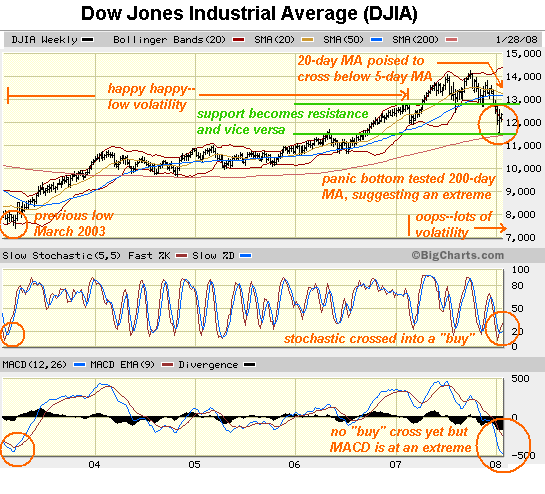

Is the Market About to Crash? (February 18, 2008) In true contrarian fashion, I wondered here on January 30 if the market was poised to rebound: We Told Ya So--But So What?. We all know the credit/debt financial bubble is popping, and that its demise is long in coming and richly deserved--but as observers, we also have to look at the stock market stripped of "fundamental" beliefs about what it "should" do. Here is the chart I posted on January 30. Since then, the market has more or less continued to noodle around:

Courtesy of frequent contributor Harun I., here is an updated chart of the Dow in a shorter time frame. Please note Harun is not responsible for my interpretive comments on the chart:

The most striking points about this chart are (in my amateur opinion): 1. the close correlation of recent price action to fibonacci projections 2. the divergence of MACD, ADX and DMI. That is, these indicators of trend have reversed from downtrends into uptrends. If price confirms that divergence, then that reversal bears close scrutiny. 3. a wedge (or flag) has formed around a key support/resistance level (about 12,700). Price tends to break up or down in a new trend from such a formation. In correspondence with Harun, I noted that market participants seem indecisive--the decline of the green DMI (strength of trend) line certainly suggests this. Harun made these cogent observations:

The decline of the green ADX line and the historical peaks of DMI in many of the markets we are watching is indicative of a non-trending state and a cyclical peak and therefore counter-trend strategies have a higher probability of success. This also means that support are resistance areas are now significant in terms of timing and time frame.If the market drops below that February 2007 low (about 12,000), then that would suggest the next leg down had begun. Alternatively, if the DJIA rises above the 12,700 resistance, that would suggest a near-term uptrend is in place. How on Earth could the market rally when the U.S. is in recession and the financial house of cards is toppling? Good question, and I don't claim to have an answer. But in the spirit of inquiry and contrarian exploration, let's consider what it's like for managers of serious money--not just hedge funds, but insurance portfolio and mutual fund managers. The Fed is lowering interest rates by half-point shots every meeting, it seems, driving short-term yields ever lower. To leave your money in short-term cash is a good way to get near-zero or even below-zero returns. That may be a winning strategy in the long run, but you're not here "for the long run"--you're here to beat alpha, or you'll get fired for "underperformance." That's the way the game is played. The bond market's had its big run from last summer, and the emerging markets--hot as a pistol the last few years--seem to have caught the flu when the U.S. markets sneezed. Europe? Looks topped out and vulnerable. Japan? Some exposure might be good, but as a manager you need some place to plant serious dough, not 5% of your portfolio. So what's the largest, most liquid stock market on the planet? The U.S. market. And were there any reason to suspect it might have bottomed, and a positive return could be gained... you'd be all over it. Given the dearth of alternative opportunities in the $5 billion to $100 billion range, you'd have to be all over it if you wanted to keep your job. But who's got cash to invest? Well, somebody has over $3 trillion under the mattress, so to speak--this is from Credit Bubble Bulletin, by Doug Noland, courtrsy of frequent contributor U. Doran:

Total Money Market Fund assets (from Invest Co Inst) jumped $26bn last week (6-wk gain $275bn) to a record $3.388 Trillion. Money Fund assets have posted a 29-week rise of $804bn (56% annualized) and a one-year increase of $995bn (41.6%).So we have the players, and the cash. Now why invest in selected U.S. companies? From the money managers' point of view, consider how few major U.S. multinationals have exposure to this credit/debt meltdown. IBM? Zero. Apple? Nada. Proctor and Gamble? Not worth mentioning given its global reach and size. Most of these corporations earn more overseas than they do in the U.S., and they have no credit risk worth mentioning. Sure, we know the world economy will follow the U.S. into recession, but on a relative performance basis, you could certainly make the argument that major U.S. multinationals and tech companies will weather the downturn much better than other global firms, and perhaps better than commodities, which are exquisitely sensitive to drops in demand--which is precisely what happens in recessions. Would you like to bet that the winter wheat crop will disappoint, and wheat will double to $20/bushel? What if the crop exceeds expectations? The it's $5/bushel wheat, here we come. In any event, most managers of serious money are precluded from even speculating in commodities and currency futures. So what's my point? Only that in times of uncertainty and high volatility, then active portfolio management is necessary to catch the trends. Take a look at this chart of the DJIA in the 70s. Note its extreme fluctuations in price:

Now in nominal terms, the 1966 "buy and hold" investor was made more or less whole again in 1973 and 1977--that is, the DJIA returned to about 1,000. But adjusted for dropping purchasing power, the "buy and hold" investor lost 2/3 of their money by the time the Bear Market finally ended in 1982. Was ignoring trends a wise investment/preservation of capital strategy? It's something to ponder as we look ahead and try to conserve what investments/purchasing power we still have.

Add this site to your reader with these feeds: RSS feed Atom feed

NOTE: contributions are humbly acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency. Thank you, Matthew G. ($50), for your very generous support of this humble site. I am greatly honored by your contribution and readership. All contributors are listed below in acknowledgement of my gratitude. For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2008 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |