|

|

|

||||||||||||

|

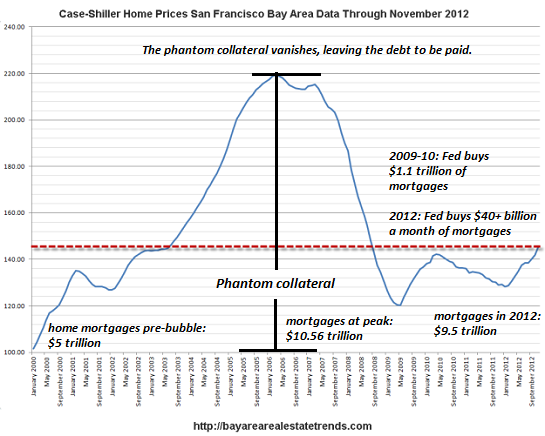

Is the Global Recovery Self-Sustaining? (February 5, 2013) To claim a "recovery" based on unlimited Central State borrowing and spending and central bank manipulation of asset valuations is self-sustaining is beyond absurd. The mainstream media (MSM) is overflowing with stories proclaiming the global economy is on the mend: Europe's crisis is in the rearview mirror, China's growth has rebounded, Japan is aggressively pursuing Keynesian Nirvana and the U.S. economy is in the sweet spot between resurgent housing prices and ever-higher corporate profits. This reality is the reason global stock markets have surged: everything's getting better. The goal of every Central Planning scheme on the planet is a self-sustaining recovery: that is, one that doesn't require another couple trillion dollars, euros, yen or yuan to keep it from collapsing in a heap. Though the conventional punditry is hesitant to declare victory, by reading between the lines we know the basic propaganda thrust: we are over the hump, the recovery (in housing, stocks, bat guano, etc.) is now self-sustaining. Really? Based on what engine of growth? If we cut through the Keynesian jargon of aggregate demand and other Cargo-Cult mumbo-jumbo, what we find is the Status Quo is hoping to boost its precious aggregate demand with the same bag of tricks that imploded so spectacularly in 2008: the wealth effect based on phantom collateral created by Centrally Planned asset bubbles. Central Planners in America have had remarkable success in inflating an asset bubble in stocks--five year highs!--but alas, the wealth effect is limited by the inconvenient reality that only the top of 10% of households own enough stock to feel any wealth effect from a market that has more than doubled in four years of Fed intervention and unprecedented fiscal profligacy. That leaves housing as the only widely held asset that can possibly generate a wealth effect in more than the top 10% of households. This explains the Federal Reserve's frantic campaigns to reflate housing prices: buying 10% of all outstanding mortgages in 2009-10, and then setting out to buy another 10%-20% in an unlimited mortgage buying program announced in 2012. Add $1 trillion+ in Treasury bond purchases designed to keep interest rates negative when adjusted for inflation, and the Fed is literally pulling out all the stops to reflate housing with historically low mortgage rates. I covered this recently in The Rise and Fall of Phantom Housing Collateral (December 13, 2012). With the Fed's unspoken collusion, lenders have reduced housing inventory by keeping foreclosed and defaulted homes off the market. By driving supply below recession-weakened demand, the Fed and lenders have managed to trigger bidding wars that have boosted home prices by 20% or more in beaten-up markets. By keeping interest yields at less than zero, the Fed has effectively driven "hot money" seeking a yield into stocks and housing; as a result, investors and prospective flippers account for 30%+ of home sales. Nothing is too grandiose for Central Planning, of course, when the goal is to save the banks from having to mark their vast portfolios of defaulted and foreclosed mortgages to market, or forcing them to liquidate millions of impaired properties. Saving crony capitalism from itself is the raison d'etre of Our Expansionist Central State (video presentation). But inflating asset bubbles to create phantom collateral to support the much-desired borrowing-and-squandering of debt-based aggregate demand has a funny little self-destruct feature: the phantom collateral vanishes, leaving behind the debt, which still must be paid. And all those heavy monthly payments on old debt leaves less income to spend on stuff. In other words, asset bubbles and debt based on phantom collateral crush real demand based on rising income. In the last Fed-engineered asset bubble, mortgage debt doubled to more than $10 trillion from a previous base of $5 trillion. The phantom collateral soon disappeared, leaving homeowners owing the extra $5 trillion: the pleasure boats, fine dining and exotic vacations of debt-based aggregate demand are long forgotten, but the debt payments are still around and must be paid monthly.

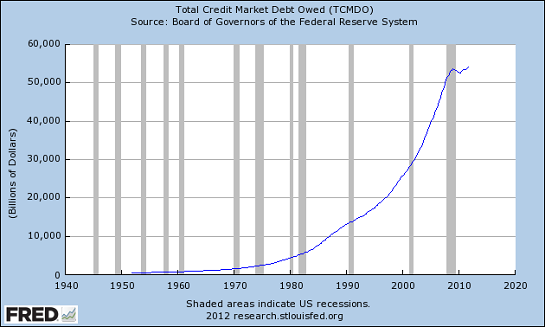

The aggregate demand so beloved by Keynesians was all based on debt rising faster than either GDP or household income: As a percentage of disposable personal income, mortgage debt rose from 53% in 1960 to 113% in 2003. Mortgage debt rose from 50% of GDP in pre-bubble years to 79.3% of GDP--an astounding rise of 30% in a mere decade of home-equity-extraction, borrow-and-blow gluttony. When this unsustainable acquisition of debt finally hit the wall in the 2008-09 global financial meltdown, debt's unyielding rise stutter-stepped and slowed, as the collateral underlying that debt vanished into thin air.

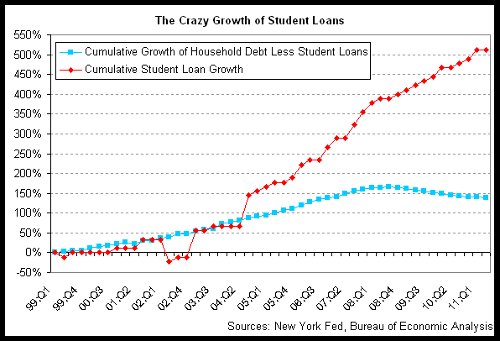

Never fear, the Expansionist Central State to the rescue. When one debt bubble bursts, crimping the consumerist orgy of "aggregate demand," then the State creates a new debt bubble--in this case, a $1 trillion student-loan monster that has turned a significant percentage of an entire generation into debt-serfs.

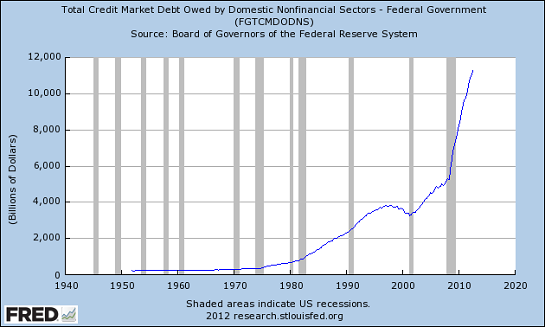

Since the collateral supporting Federal debt is presumed to be infinite, so too is the Central State's line of credit: need $6 trillion to prop up a crony-capitalist, hopelessly corrupt and inefficient Status Quo? No problem.

Though you will not find a Keynesian pundit or economist with the courage required to admit it, the same problem of phantom collateral applies to Federal and state debt: the consumption all that debt funded is soon forgotten, but the debt remains to be paid, essentially forever. The collateral supporting Federal debt is also phantom. Printing money is not the same as creating surplus value; that requires actual work and capital, and it is intrinsically limited by the cost-basis of production and market forces.

To claim a "recovery" based on unlimited Central State borrowing and spending

and central bank manipulation of asset valuations is self-sustaining is beyond

absurd. Aggregate demand (i.e. debt-based spending) supported by phantom collateral is not

sustainable, no matter how many times Keynesian Cargo-Culters and Federal Reserve

governors dance around their flickering little camp fire waving dead chickens.

RIP: Our Expansionist Central State (23 Minutes, 25 Slides) CHS with Gordon T. Long: Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:  1. Debt and financialization

1. Debt and financialization

2. Crony capitalism and the elimination of accountability 3. Diminishing returns 4. Centralization 5. Technological, financial and demographic changes in our economy Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of

the same coin: once we accept responsibility, we become powerful.

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

NOTE: gifts/contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Subscribers ($5/mo) and contributors of $50 or more this year will receive a weekly email of exclusive (though not necessarily coherent) musings and amusings. At readers' request, there is also a $10/month option. What subscribers are saying about the Musings (Musings samples here): The "unsubscribe" link is for when you find the usual drivel here insufferable.

All content, HTML coding, format design, design elements and images copyright © 2013 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I am honored if you link to this essay, or print a copy for your own use.

Terms of Service:

|

Add oftwominds.com

Oftwominds.com #7 in CNBC's

#25 in the top 100 finance blogs

|