|

|

| weblog/wEssays archives | home | |

|

Inflation/Deflation I: Is Japan an Accurate Model? (January 8, 2007)  Knowledgeable reader Cheryl A. was kind enough to ask me to weigh in on the "will the

near future be inflationary or deflationary" question:

Knowledgeable reader Cheryl A. was kind enough to ask me to weigh in on the "will the

near future be inflationary or deflationary" question:

I was wondering if you would consider discussing why some experts/ authorities believe the future will be inflationary while others see it as deflationary. John Williams is now projecting it will be hyperinflationary.

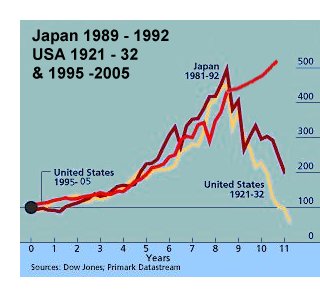

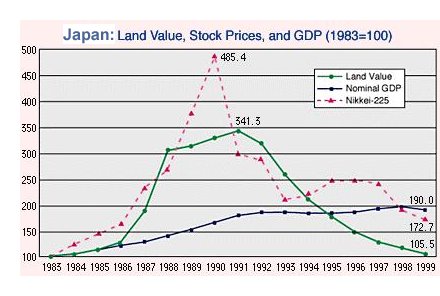

An astute question on a confusing--and for investors--"gotta get this right" topic. My responses will take the entire week, and will hopefully yield conclusions I haven't read elsewhere, though no doubt many others have followed the same trails. Although it may seem odd to start the discussion by considering Japan, it's the logical starting point because so many deflationists (such as the esteemed Mish) point to Japan as the model the U.S. will follow as it slides down a deflationary path. As a non-believer in any economic school--Austrian, Chicago, etc. etc.--I am not looking for evidence to support my belief system. Japan is a highly complex society and economy, the world's second largest despite a decade of relative decline. Care must be shown before jumping to conclusions about anything within Japan, because the surface may not be the reality. Long-time readers know that we maintain a large circle of personal friends in Asia, stretching from Thailand, Indonesia and Singapore to China, Korea and Japan, where our friends number in the dozens. As a result, my understanding has been informed by experienced insiders. If you think you can grasp Japan via a dry paper or two by a stateside "expert," you are sadly mistaken. (Though I did study the language, geography, literature and society in my university days.) This is a warning to anyone seeking a simplistic answer to the deflation/inflation question: it isn't simple. For an example, let's turn to some snapshots of Japan. Our first chart shows the asset-inflation bubble which rose in Japan's "easy money" 1980s and subsequently collapsed, like all such asset bubbles--as shown in the second chart. Here we see that land values rose with the stock market, and then fell, in a long slow slide, to a full-retrace, i.e. a return to the pre-bubble valuations. Meanwhile, the GDP traced a nearly straight line even as asset prices plummeted. This chart shows asset inflation and then deflation on a grand scale. So let's ask: what conditions were present which were unique to Japan which may not be present in the U.S.? 1. Japanese debt, corporations and their interlocking ownerships are not transparent. While much has been made of the past decades' "reforms," only a fool would claim Japan's debt and corporate structures are now as transparent as those in the U.S. As I have documented elsewhere (see Archives, "Unfolding Crises: Asia"), the true size of bad debt in Japan remains unknown, as so much bad debt (i.e. uncollectable loans lacking collateral) remains on the books as loans in good standing. The underlying health of Japan's financial system remains suspect. 2. For cultural reasons, houses depreciate from the moment they're completed, regardless of what land values do. In Japan, houses are routinely pulled down after 30 years and replaced. If you buy a house and the land beneath it, the value is reckoned much as property tax bills are figured in the U.S.: one value for the house, one for the land. The house will lose value every year regardless of inflation or deflation. 3. The Japanese countryside has been losing population for decades. On my first visit to rural Japan in 1992, I was surprised to see abandoned schools, and to meet Japanese farmers married to Sri Lankan women. Gaijin (foreigners) are rare in the countryside, but less so nowadays, as Japanese men are finding it difficult to find Japanese women willing to live and work in farm country. As a result, they're seeking wives from elsewhere in Asia. The U.S. has also experienced a decades-long exodus from rural counties, but the property bubble in Japan reached far deeper into the countryside than the U.S. bubble has. According to blogger Fred Roper in Oklahoma City (see his Satellite Sky blog in the right-hand column), you can still buy a decent house in a decent neighborhood in Oklahoma City for about $100,000. This supports the notion that the housing bubble in the U.S. remains a coastal phenomenon.  Part of the reason behind Japan's rural bubble lies in the political structure of its government.

Rural representatives retain far broader powers than in the U.S., and the subsidies ("bridges to nowhere"

like the one in Alaska which excited such outrage in the U.S.) have been far more egregious

than in the U.S. The point: conditions unique to Japan boosted land prices in rural

Japan to a degree which is not present in the U.S. The decline in rural asset prices

was thus exacerbated by these distortions.

Part of the reason behind Japan's rural bubble lies in the political structure of its government.

Rural representatives retain far broader powers than in the U.S., and the subsidies ("bridges to nowhere"

like the one in Alaska which excited such outrage in the U.S.) have been far more egregious

than in the U.S. The point: conditions unique to Japan boosted land prices in rural

Japan to a degree which is not present in the U.S. The decline in rural asset prices

was thus exacerbated by these distortions.

4. Japan is losing population as a result of a birth dearth. Here is a delightful photo of our friend's two nieces. As I make a mental list of about 20 young women between 24 and 35 whom we know, I realize only four have children. Now perhaps a few more will have children later in life, and perhaps this group of women is not representative; but this suggests a staggering reduction in young women's willingness to bear children (or even get married)--a trend which statistics confirm. The point is obvious: a declining population feeds land and housing deflation, as there is less demand for housing every year.  5. Despite its ballyhooed "recovery," Japan continues to depend on deficit spending to

an astounding degree. Note that bonds, i.e. new government debt, is fully 42% of

the central government's "revenues." Even though the interest rate on thse bonds is a pitiful

1% or so, the interest payments still consume 22% of the federal budget. What would happen

if Japan was forced to live with a balanced budget? Or what if interest rates rose to

5%?

5. Despite its ballyhooed "recovery," Japan continues to depend on deficit spending to

an astounding degree. Note that bonds, i.e. new government debt, is fully 42% of

the central government's "revenues." Even though the interest rate on thse bonds is a pitiful

1% or so, the interest payments still consume 22% of the federal budget. What would happen

if Japan was forced to live with a balanced budget? Or what if interest rates rose to

5%?

The point: Japan has been living far beyond its means, depending on the surplus savings of its citizens, and their willingness to accept pathetic rates of return (1%) on those savings. Despite a decade of "pumping" (low interest rates, deficit spending, etc.), the government itself is totally dependent on deficit spending to fund typical government functions. The point: Japan can pursue the folly of massive government deficit spending indefinitely because its populations saves prodigiously and is willing to accept near-zero returns. The ultimate wisdom of piling mountains of debt onto a shrinking future generation is suspect, and it this regard Japan has failed to reform the key issue: the generational transfer of debt service to the future taxpayers.  6. Despite reforms, Japan has enormous sources of more-or-less enforced savings.

Residents had few options for savings other than postal accounts, and even though some of

these restrictions have been lifted, the government was able to tap this vast pool of

domestic savings--and the Japanese remain prodigious savers--while paying virually nothing in

the way of interest. There are cultural considerations here which cannot be quantified;

Japan is a conservative society and people continue to save in traditional fashion despite

new opportunities. Furthermore, many people still recall losing vast sums in the stock

market bubble and thus continue to save in traditional postal or bank accounts.

6. Despite reforms, Japan has enormous sources of more-or-less enforced savings.

Residents had few options for savings other than postal accounts, and even though some of

these restrictions have been lifted, the government was able to tap this vast pool of

domestic savings--and the Japanese remain prodigious savers--while paying virually nothing in

the way of interest. There are cultural considerations here which cannot be quantified;

Japan is a conservative society and people continue to save in traditional fashion despite

new opportunities. Furthermore, many people still recall losing vast sums in the stock

market bubble and thus continue to save in traditional postal or bank accounts.

As this chart shows, a stunning amount of Japan's tax revenues now goes just to service debt. So what are the conclusions? We should be careful not to assume Japan's property bubble parallels our own; while all bubbles share certain characteristics, they do not necessarily share the same conditions. For instance, political and financial distortions and long-term population trends are quite different in the U.S. than in Japan. Despite the rah-rah about Japan's "recovery," the Japanese government's finances remain dependent on massive new debt--a stunning generational transfer of ever-rising obligations. The fact that Japan can continue a "prime the pump" strategy of low interest rates and massive deficit spending does not mean they have successfully reformed the distortions and bad debt within their financial system. The system relies on an enormous pool of domestic savings which is restricted--in cultural and regulatory ways--from seeking higher returns overseas. The U.S. should be so "lucky." For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2007 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |