|

|

| weblog/wEssays archives | home | |

|

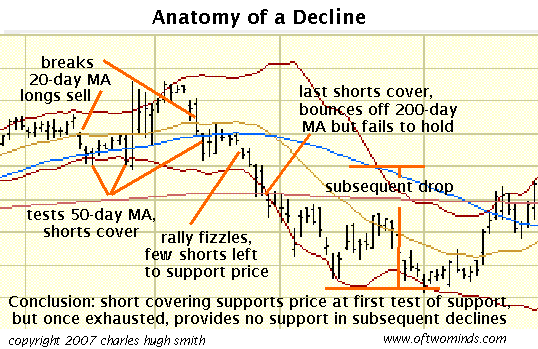

Does Short Interest Really Support the Market? (June 27, 2007) To those of you who tire of financial and stock analysis--my apologies. The reason why I am concentrating on this topic this week is the market may be poised to move dramatically-- which provides an opportunity for us small-fry to profit, should we guess the direction of the move, or hedge our bets properly. Disclosure: I took a short position via puts yesterday in CFC and FNM, two stocks I discussed in the Monday entry. I anticipate them skyrocketing, now that I am short. One reason to suspect the market is posed to move dramatically is all the major indices are hugging their 50-day moving averages; this suggests indecision. The high volume on major down days like last Friday suggests weakness/distribution, i.e. "smart money" selling to those willing to "buy on the dips." Let's consider one cliche you read again and again: record short interest places a strong bid under the market, providing key support in the event of a sharp decline. As this chart shows, this works at the first test of support; but once the shorts have covered, there's no longer any floor under the stock.

Here's the basic idea: let's say a hedge fund manager owns a million shares of Google; he or she is thus "long" Google. To protect the long position against a sudden drop, the manager sells a million shares short, or buys put option contracts on a million shares. This "short position" fully hedges the million "long" shares against losses. So if GOOG drops $10 per share, the portfolio drops $10 in value on the long side, but gains $10 on the short side--i.e. the shares held short have a $10 gain, as do the puts. Recall that selling short means you received the current price for shares you don't yet own; when you buy the shares later (hopefully for a price lower than you received), then you've "covered your short." The difference between what you sold them for and what you paid to buy them is your profit. Headlines blare that "short interest is at new highs." So guess what percentage of NYSE (New York Stock Exchange) shares are short. Drumroll, please: 3.3%. Yes, the "record high" short interest is not even 4% of all outstanding shares--about 12 billion shares, or four days' trading volume. This is an awfully small percentage of shares to support the idea the market can't decline very much. Let's stand in the shoes of the hedge manager for a moment. Let's say you sense GOOG is weakening--say it's dropped below the key technical level of the 20-day moving average. Why would you hold your long shares if you detected a downtrend in the making? You'd sell (distribute) your long shares, and hold your short shares or puts until the dust settles. Guess what: every other manager with a long position is thinking the same way. So as everyone dumps their long shares, the selling accelerates the price decline. At some point--again, perhaps the 50-day or 200-day moving average, some managers will "cover their shorts" by buying shares of GOOG. This does provide a temporary "floor" under a stock's decline--but what happens when the shorts have all covered and the price is still dropping? There is no longer any shorts to provide a bid/buying. As this chart (the stock is CFC) shows, once key technical levels which trigger short covering are violated, then the stock continues dropping. You may recall reading contributor Harun I.'s comments on the Pareto Principle in Hedge Funds and The Pareto Principle (February 19, 2007). The principle is often called the 80/20 rule, and it has an adjunct: the 64/4 rule. Hmm, isn't it interesting that short positions are about 4% of the market. The principle suggests that small number of shares can have an effect far larger than their percentage would suggest, causing major shifts in 64% of all shares. Proponents of the "short covering will support the market" idea are convinced the 4% covering will support the 64% of stocks declining; they may be right for awhile, but when the 4% have covered, the effect might be to remove the last leg of support from a market which then goes into a free-fall. Why is short interest rising? There may be two reasons. One is the growth of hedge funds, which hedge long positions by going short. (Many mutual funds are restricted from having large short positions.) The other might be that those who tend to go short--i.e. professional managers and traders--are making sure they will profit should a sharp downtrend occur. To summarize: take all assurances that "record shorts will support the market" with a hefty grain of salt/skepticism. Hedge funds may unwind both long and short positions in a hurry, further draining the pool of shorts which need to be covered. For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2007 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |