|

|

|

Could 50% of All Homes End Up in Foreclosure? (June 3, 2008) Just how bad could the housing bust get? How about half of all urban homes being in foreclosure? As stunning or unbelievable as that may sound, it already happened once in the U.S., in the Great Depression, as documented in this report: Lessons from the Great Depression (St. Louis Federal Reserve). Though history doesn't repeat, it certainly echoes, and the parallels between the present and 1934 are particularly sobering. The only "missing ingredient" to a full-blown depression is job loss/income contraction, and many of us foresee a long, painful wave of lay-offs and downsizing on a global scale just beginning. How did half the nation's urban housing end up in foreclosure? All too easily, it seems; eerily, the slippery slope seems remarkably like the present:

Here are excerpts from the report:

A study of 22 cities by the Department of Commerce found that, as of January 1, 1934, 43.8 percent of urban, owner-occupied homes on which there was a first mortgage were in default. The study also found that among delinquent loans, the average time that they had been delinquent was 15 months.The report details how loose lending standards during the 1920 Housing Boom contributed to the severity of the Bust:

Thus, although the proximate cause of the high rate of loan delinquencies and foreclosures during the 1930s was the economic depression, the likelihood of default on any given loan apparently was influenced by the characteristics of the loan itself.Do you reckon that 20% default rate in the subprime mortgage market reflects a similar dynamic? In another parallel, the state and Federal governments jumped in to "solve" the problem with new government-backed refinancing and by "freezing" the foreclosure process. Interestingly, the Pareto Principle's 20% (the 80/20 rule) shows up twice: the Federal agency created to refinance every homeowner in trouble ended up owning 20% of all mortgages in the country, and 20% of those mortgages still entered foreclosure.

33 states enacted legislation providing relief for those with delinquent mortgages, including 28 states that imposed moratoria on home foreclosures (Poteat, 1938). The justification for government intervention remains the same as well:

The right of lenders to foreclose on collateral is the main reason why the interest rates on secured loans, such as home mortgages, are typically much lower than those on unsecured loans, such as credit card debt. Ordinarily, mortgage foreclosures receive little notice from the public because they have little impact on parties other than the delinquent borrower. Are there any differecnes between then and now? The report's author worries that there is one key difference: the appetite for risk is so pervasive and ravenous now that any bail-out may well feed further speculative lending. And moratoriums, as popular as they might be politically, merely hinder the "work-through" required to restore the credit markets:

Some policies, including a government bailout of delinquent loans or expanded loan guarantees, could also encourage increased financial risk-taking and thereby lead to further instability in the future.So what finally restored the housing/credit markets and the U.S. economy? Borrowing and spending trillions of dollars to fight World War II. (The U.S. government borrowed about $500 billion during the war which adjusted for inflation would be trillions in current dollars.)

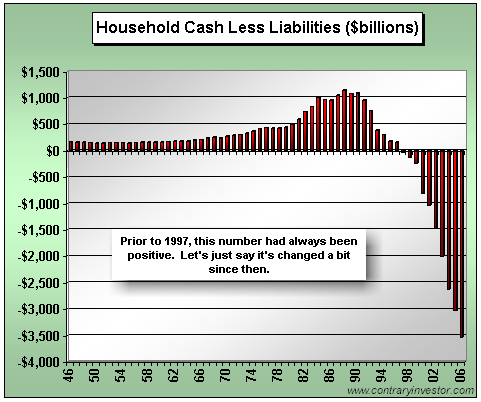

As the global economy contracts, so will global savings which can be channeled into buying U.S. T-bills and other debt. Since we'll be unable to "borrow our way out of this mess," then what is the ultimate solution? Start saving and investing, and write off the trillions in bad debt crippling the credit markets. The government propaganda machine and the TV pundits will have you believe there will be no recession and no job losses. We shall see who's right: the cheerleaders and their ginned-up statistics, or those of us who see severe job losses as the inevitable consequence of a credit contraction. NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, T. Simms ($25), for your unexpected and very generous donation

via mail to this site.

I am greatly honored by your support and readership.

For more on this subject and a wide array of other topics, please visit my weblog. All content, HTML coding, format design, design elements and images copyright © 2008 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||

Unfortunately, that's not an option now; we've already borrowed trillions

to fight distant wars and other government spending, and we've relied not on

domestic savings but on willing

foreign buyers of our debt to do so.

Unfortunately, that's not an option now; we've already borrowed trillions

to fight distant wars and other government spending, and we've relied not on

domestic savings but on willing

foreign buyers of our debt to do so.