|

|

|

||||||||||||

|

The Endgame of State/Local Government Pensions (June 14, 2013) There is no way the pensions and benefits promised in an era of financialized abundance can be paid once the wheels of financialization fall off. Yesterday I described the destructive effect of abundance on decision-making: An Abundance of Bad Decisions. One aspect of this dynamic is the tendency to extrapolate prosperity into the future as a permanent state of affairs. One example of this is state/local government pensions: during the past 30 years of financialized abundance, the benefits and pensions promised to public employees were increased substantially. Public unions are a powerful political force in many states, and in eras of rising tax revenues, it's an easy political decision to increase public employee benefits and pension payouts. The rising stock and bond markets generated huge profits for the public-employee pension funds, enabling them to grow without taxpayer contributions. The effortlessness and persistence of this growth encouraged the mindset that pensions would be paid for via the magic of ever-rising markets; if tax revenues weren't even needed to fund the pension plans, then no hard political choices would ever have to be made. Alas, the 8+% annual growth rate of the boom era is now structurally unrealistic. The New Normal is bond yields of 2% or 3% at best, and equities markets that are increasingly at risk of significant sell-offs. The illusion that the pension funds can pay the promised benefits is maintained by plugging wildly unrealistic 7% or 8% returns into projections of future pension fund earnings. Now those unrealistic projections are being questioned: California, Illinois on Brink of Pension Crisis (Mish). This means tax revenues will have to be diverted from other government expenses to fund the pension plans. A key dynamic in the pension crisis is called the the ratchet effect: it was effortless to increase the benefits and pensions of public employees, but it is effectively politically impossible to trim those promises. The Ratchet Effect is one reason why the nation's political machinery has become sclerotic and ineffective: Dislocations Ahead: The Ratchet Effect, Stick-Slip and QE3 (February 14, 2011). As correspondent Mark G. explains, the public pension crisis has been 20 years in the making, and cannot be resolved without massive, sustained political and fiscal pain:

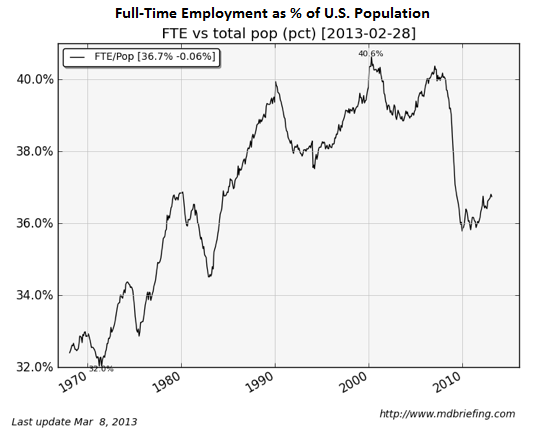

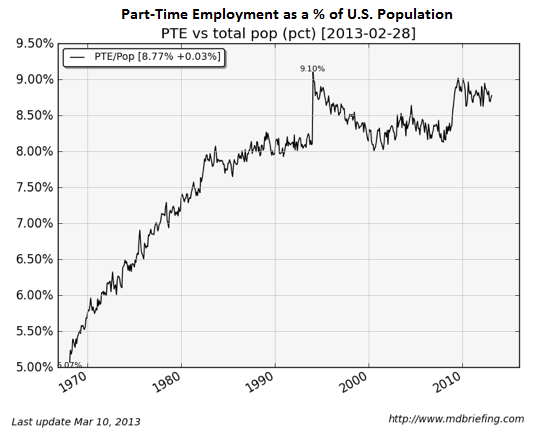

1. Long term interest rates began a secular decline in 1981. This continued until at least early this year. Thank you, Mark, for this primer on the unsustainability of public pension promises. Raising taxes is the default solution to state/local government shortfalls, but there's a structural problem with raising taxes: 1. Fulltime jobs--the kind that pay the bulk of state/local taxes--are stagnant. 2. Real income is down for the vast majority of workers.

If state and local governments think low-income part-time workers can pay more taxes and survive, they are engaged in magical thinking:

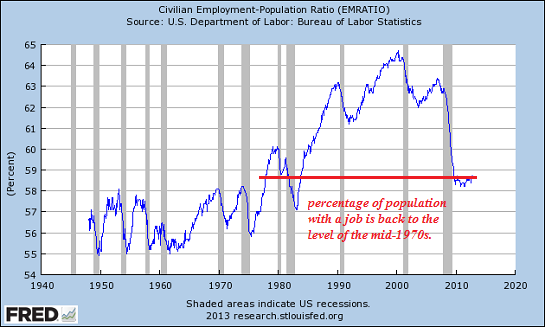

The percentage of the population with a job is back to the levels of the 1970s:

Real (adjusted for inflation) household income has declined by almost 8%; exactly how are households supposed to pay higher state and local taxes as their income steadily declines?

State and local governments planning on a Federal bailout should ponder this chart, which clearly shows a structural gap of monumental proportions between Federal tax revenues and Federal spending.

The endgame of promises made in an era of illusory, financialized abundance will be hurried along by a collapse in the equities and bond markets. I addressed the likelihood that all three primary investment markets would decline together in What If Stocks, Bonds and Housing All Go Down Together? (May 24, 2013): in a nutshell, if yields rise, mortgage rates rise and that sinks the housing market. Rising yields also sink stocks, as higher yields pull money out of risky equities. And rising yields also collapse the value of existing bonds, wiping out much of the wealth that is currently considered safe.

In sum: there is no way the pensions and benefits promised in an era of financialized

abundance can be paid once the wheels of financialization fall off.

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:  1. Debt and financialization

1. Debt and financialization

2. Crony capitalism and the elimination of accountability 3. Diminishing returns 4. Centralization 5. Technological, financial and demographic changes in our economy Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of

the same coin: once we accept responsibility, we become powerful.

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

NOTE: gifts/contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Subscribers ($5/mo) and contributors of $50 or more this year will receive a weekly email of exclusive (though not necessarily coherent) musings and amusings. At readers' request, there is also a $10/month option. What subscribers are saying about the Musings (Musings samples here): The "unsubscribe" link is for when you find the usual drivel here insufferable.

All content, HTML coding, format design, design elements and images copyright © 2013 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I am honored if you link to this essay, or print a copy for your own use.

Terms of Service:

|

Add oftwominds.com

|