|

|

| weblog/wEssays archives | home | |

|

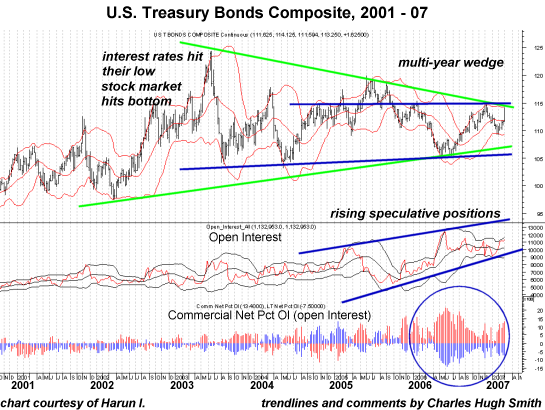

Bonds, Interest Rates and Gold (March 6, 2007) Since calling for a downturn in equities and gold on Feb. 26 (woo-hoo), I've been busy throwing doubt on the cheerleaders' next favorite consensus: that the Fed will have to lower interest rates, thereby sparking a new frenzy of cheap borrowing which will re-start the sinking real estate and equity markets. To those of you who find charts tiresome: please bear with me. If, as I have long suggested here, the housing, equity (stocks) and bond markets all enter long-term declines, then that will have an enormous impact on every citizen in the nation: tax receipts will plummet, pension funds will sink, 401K retirements will be savaged, "the wealth effect" (rising home and stock values make people feel richer) will reverse, gutting the consumer spending which has propped up the "debt prosperity" of the past seven years--just to name a few possible effects. Frequent contributor Harun I. was kind enough to share some charts of the U.S. Treasury Bonds. I have been careful to note which interpretive comments are mine, as I wouldn't want Harun to be mistakenly held accountable for my interpretations of his charts. Keep in mind that the value of a bond is inverse to interest rates; when interest rates peak, bonds drop in value. When interest rates fall to their nadir, bonds rise in value. It works like this: if a $100 bond pays 5% interest today, and interest rates jump to 10% tomorrow, then who wants to buy a bond paying a lousy 5%? Nobody, so the bond drops 50% in value. In reverse order: if you own a bond which is paying 10%, and interest rates drop to 5%, then your bond will command a premium (rise is value) because everyone wants yesterday's higher interest. Let's start with a long-term look at U.S. Bonds, with comments and trendlines by Harun:

Note that bonds and gold displayed a rough correspondence through about 2001, rising and falling in near-unison. But since 2002, the bond-gold ratio has displayed a widening divergence from this historical correlation. What does this suggest? Only that such divergences tend to eventually revert to historic means: either gold has to rise or bonds have to drop--or some of both. Next up: a chart of the U.S. Treasury Bonds Composite which I marked to show a wedge formation--which tends to break sharply up or down--and the rise in speculative interest in the bond market. Such a rise in open interest might well provide the fuel for the kind of big move which the wedge predicts.

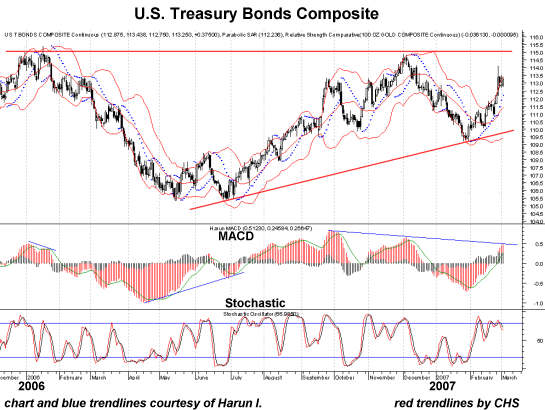

In this short-term chart of the Bonds Composite, Harun noted the decline in MACD, which diverges from the rise in bonds. (A similar divergence in MACD presaged the current decline in stocks.) I added red trendlines marking a resistance level, which suggests that bonds may well "top out" at that ceiling. This further suggests that pundits hyping "sure thing" reductions in lending rates may be mistaken. The second red line shows the uptrend running smack into this resistance--forming the sort of wedge which often breaks sharply to the downside, especially when MACD has been declining.

The interesting thing about charts is that they don't tell you the proximate cause for a change in trend--they simply suggest the odds favor such a reversal. Thus my entry of Feb. 26 (yes, the day before the meltdown--not to congratulate myself too much for a pleasant coincidence) was based not on a reading of the Shanghai market (that came the actual day of the reversal) but simply on the type of divergences noted on the charts above. In other words: those foreseeing lower interest rates always turn to some "fundamental" reason, like the faltering economy will force the Fed to lower rates. But fundamentals don't always offer much in the way of accurate prognostication. So while I can't tell you the reason why interest rates appear set to rise--will it be a collapse in the dollar, a massive reduction in liquidity, a politically-inspired sell-off of U.S. Treasuries?--the charts don't offer much support to the view that interest rates are set to plummet and bonds to correspondingly skyrocket. The upshot: be careful about acting on "sure things." For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2007 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |