|

|

| weblog/wEssays archives | home | |

|

The Growing Financial Risks of the Housing Bubble (May 30, 2006)  This is not your father's housing market or indeed, his mortgage market. The imbalances,

and thus the risks, of the housing bubble have spread into our entire financial system.

This is not your father's housing market or indeed, his mortgage market. The imbalances,

and thus the risks, of the housing bubble have spread into our entire financial system.

How so? Let's start--and end--with mortgages, leverage, derivatives and debt. First up is the chart showing that mortgages have grown to about 2/3 of banks' total credit portfolios. Note how this is up from less than 30% twenty years ago. This isn't just a measure of their mortgage exposure; it's also a measure of their exposure to risk in the credit market should a decline in the housing market trigger a rise in non-performing loans--i.e., people squeezed by ARM re-sets or rising debt loads to the point they are unable to keep current on their mortgage payments.  A very knowledgeable reader who prefers to remain anonymous recently encapsulated some of

the other risks inherent in the current housing and lending markets. His first point: the extreme

downside risk inherent in highly leveraged real estate:

A very knowledgeable reader who prefers to remain anonymous recently encapsulated some of

the other risks inherent in the current housing and lending markets. His first point: the extreme

downside risk inherent in highly leveraged real estate:

Your recent posting about the significance of a 10% decline is certainly right on the mark. What's interesting is that people don't think about the fact that in the stock market 10% volatility is nothing, but that's because margin accounts limit leverage of retail investors to 50%. In the housing bubble, 10% volatility is HUGE because there are so many investors leveraged to 100% (or more). Even those without interest only or negative amortization loans who HELOC'd (home equity line of credit) are at huge risk, especially since home equity is such a large part of people's retirement plans.This contributor noted the psychological impact of the tax policy which rewards people for flipping their primary residence every few years--and the rise of mortgage-backed securities and derivatives: Another topic of interest I don't see get much press as a driver of the housing bubble relates to the tax free treatment of the first $250K or $500K in gains on a primary residence. Although there's much press on how our government spurred the housing bubble with a liquidity bail out based on money supply and cuts in interest rates, I think the effect of these tax credits are hugely underestimated in terms of a wholesale change in American "investment psychology". An additional driver I would suggest which also gets little press is the massive proliferation of derivatives by financial institutions to off load and disperse mortgage loan risk and the lax regulatory environment promoted by the prior and current Fed.  A bit of history is necessary here. In the good old days, local banks would actually

retain the mortgages they underwrote, collecting the interest and principal as an integral

part of their portfolio of assets and their income stream. This is now as quaint as buggy

whips. Lenders quickly sell any mortages they underwrite to large banks which just as quickly

aggregate hundreds of millions of dollars of mortgages into "mortgage backed securities"--in

effect, turning mortgages into securities which can be traded like bonds. As the

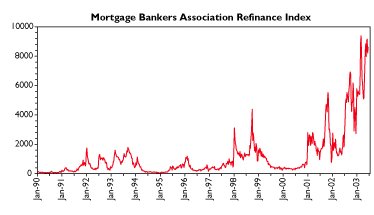

chart reveals, this practise exploded in 2000.

A bit of history is necessary here. In the good old days, local banks would actually

retain the mortgages they underwrote, collecting the interest and principal as an integral

part of their portfolio of assets and their income stream. This is now as quaint as buggy

whips. Lenders quickly sell any mortages they underwrite to large banks which just as quickly

aggregate hundreds of millions of dollars of mortgages into "mortgage backed securities"--in

effect, turning mortgages into securities which can be traded like bonds. As the

chart reveals, this practise exploded in 2000.

And like bonds, the securities can be tranched into various chunks of risk and hedged by various types of derivatives. The idea, of course, is to minimize risk by hedging with derivatives--but the explosion of derivatives has put risk management in uncharted waters. As my correspondent explains:

Regarding mortgage backed securities, just to be clear, there seem to be two related issues:Well said, well said. For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2006 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |