|

|

| weblog/wEssays archives | home | |

|

Housing Affordability: Crushed by Debt (May 11, 2007) Yesterday we considered the possibility that interest rates might rise for the next 15-20 years, effectively lowering the value of housing with each tick upward. Today let's consider affordability in terms of the percentage of household income which "should" go toward housing.

Back in the good old days, the calculation was simple: your mortgage payment shouldn't be more than a quarter of your gross income. This was also a simple calculation because few people had revolving credit or any debt other than a car payment. No credit cards? You're kidding, right? I recall rather vividly the year my Mom started to complain about her Mastercharge bill (as Mastercard was called back then)--1968. Prior to that, a business type might have a Diners Card, which was not revolving credit but a charge card like American Express which had to be paid off monthly. Sure, you might have had a Sears card, but the credit limit was $200--enough for a new washing machine or table saw and not much else. Credit was issued sparingly, and used sparingly. The typical limit on revolving credit was perhaps $1,000 or at most $2,000 in today's (depreciated) dollars--$500 was a big limit. Now just about all of us receive $20,000 credit-limit card offers every week.

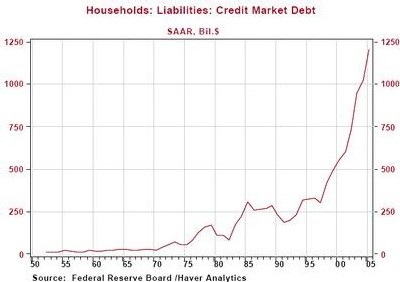

Student loans? Nonexistent. Now people are still paying off student loans in their 40s, with their kids' college just a few years away. Talk about becoming debt serfs. Take a look at this chart and notice that deficit spending (living off borrowed money) has been the order of the day, violating decades-long trends of fiscal prudence. Frequent contributor Harun I. provided this insightful commentary on the topic: (emphasis added by me) I like to run and bike ride. As I ride and run through neighborhoods and look at the local real estate rag the whole affordability question has been nagging me. Anything listed at your modest $250,000 is a shack I wouldn't want Ned-the-wino to live in and yet people are buying homes $300,000 and up like everything is okay.

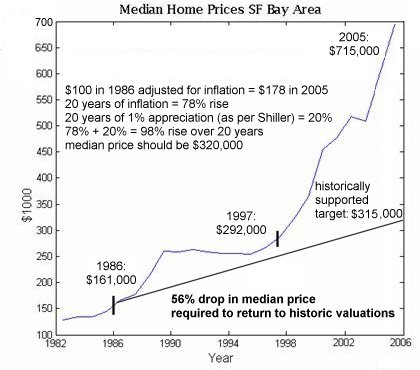

As I write this Thursday, the stock market is down due to the "surprising decline" in retail sales. Meanwhile, the market was up just days ago on the "surprising rise" in consumer debt. No need to connect the dots--they're so close they're touching. As these charts show, consumers have been living off borrowed money for years; household debt has leaped. As an exercise, let's take the median household income of about $45,000 and see how much house that supports in a traditional (i.e. prudent) setting. If we account for principal as well as simple interest, then a mortgage of about $180,000 looks do-able.

With a traditional 20% cash down payment of $45,000 (try not to laugh too hard--as if that ever happens any more) then the median household income would support buying a $225,000 house ($45K down, mortgage of $180K). The median price of a house in the U.S. is about $215,000, so on the surface things look reasonably aligned. But we all know home values on the heavily-populated coasts are much higher than $215,000, The income is higher, too, but not by as much as you might think. California's median income is about $50,000--certainly not enough to justify median house prices in the $600,000 range. If we factor in non-mortgage debt--auto loans, student loans, and credit cards--then the actual earnings left for mortgage debt service is lower than such traditional ratios as "28% of gross income" assume. Simply put: people are carrying much higher consumer debt loads than ever before, and devoting a larger share of their income to servicing that debt than ever before. The actual net income left to service mortgage debt means the actual debt-to-income ratios are far higher and far less fiscally prudent than in decades past. To repeat Harun's question: With MEW (mortgage equity withdrawal) effectively shutdown people are turning to credit cards to stay afloat but how long can that last? If you consider these charts, the answer is: not very long. For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2007 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |