|

|

|

||||||||||||

|

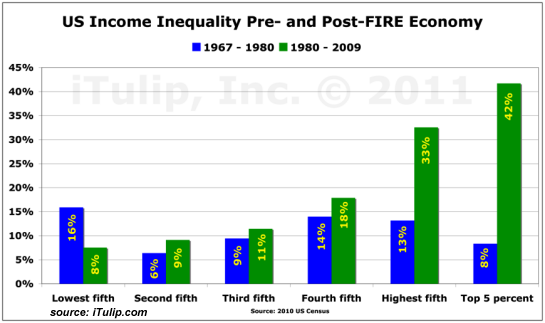

How Cheap Credit Fuels Income/Wealth Inequality (May 30, 2013) Cheap credit is a great boon to the wealthy and a path to debt-serfdom for everyone else. The ever-widening chasm between the wealthy and the "rest of us" has generated any number of explanations for this deeply troubling phenomenon. We can start with capitalism, which is based on competition for innovations, processes, markets, labor and capital. The more successful participants will naturally garner more profit and premium, leaving less for those who don't control assets and skills that carry high premiums in the marketplace.

But this fundamental source of inequality doesn't explain why wealth and income inequality was considerably lower in previous eras of economic expansion. Many observers rightly point to the capture of federal regulatory bodies by corporations and the transition from an industrial economy with plentiful low-skill, high-wage jobs to a post-industrial knowledge-based service economy as causes.

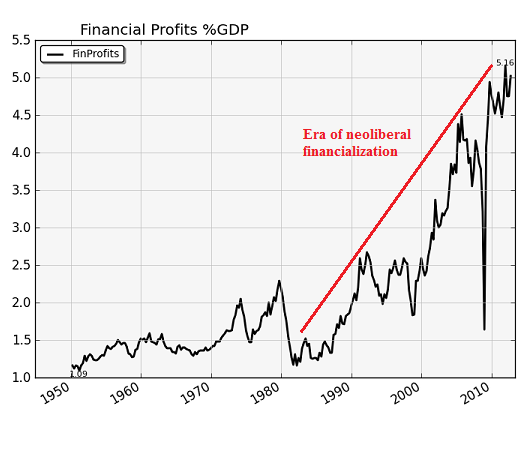

These are undoubtedly causal factors, but what most analysts either miss or dare not mention because it threatens their own privileged spot at the feeding trough is financialization, the process of financially commoditizing every asset to the benefit of the financial sector and the state (government), which also benefits from skyrocketing financial profits, bubbles and rising asset values (love those higher property taxes, baby!).

Financialization is most readily manifested in the FIRE sectors: finance, insurance, real estate. You can see the results of financialization in financial profits, which soared in the era of securitization, shadow banking, asset bubbles and loosened or ignored regulation:

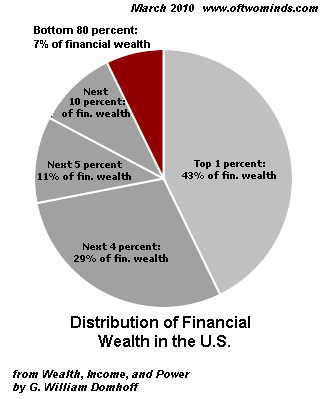

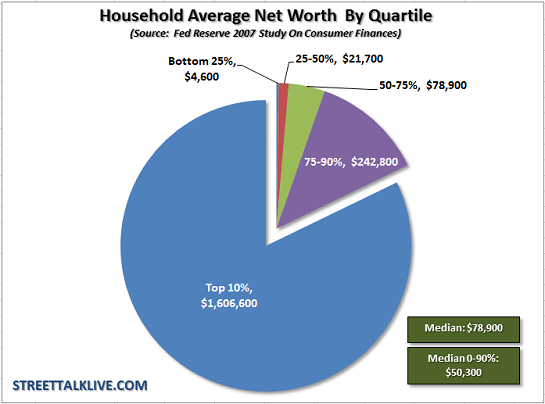

Here's how cheap, abundant credit--supposedly the key engine of growth, according to the Federal Reserve--massively increases wealth inequality: the wealthy have much greater access to credit than the non-wealthy, and they use this vastly greater credit to buy productive assets that generate income streams that increase their income and wealth. As their income and wealth increase, their debt loads decline.

Compare the superficially well-off upper-middle class family with two incomes and a truly wealthy family. The upper-middle class family may have an income well in excess of $100,000, but it used its access to credit to buy non-productive assets such as a sprawling house with granite countertops, two luxury vehicles, etc. Even the horrendously costly college education for the family's kids is ultimately non-productive, since the students didn't learn how to successfully navigate the digital-software-fabrication-robotics-automation (DFSRA) emerging economy. The wealthy family bought a 24-unit apartment building with its credit. That property spins off positive cash flow every month, and that income stream supports a high asset valuation which serves to increase the creditworthiness of the family. Productive assets that churn out steady rentier income streams can be pyramided into ever greater access to credit that is also cheaper than the credit offered to middle-class households. Student loans have rates of 6% to 9%, for example, while the wealthy family can buy productive assets at 3% or 4%. The high earned-income household has access to cheap auto loans, but since the vehicles lose value the moment they're driven off the lot, this low rate is an illusory benefit. The family home is supposed to be a store of wealth, but the financialization of housing and changing demographics have mooted that traditional assumption; the home may rise in yet another bubble or crash in another bubble bust. It is no longer a safe store of value, it is a debt-based gamble that is very easy to lose. Credit has rendered even the upper-income middle class family debt-serfs, while credit has greatly increased the opportunities for the wealthy to buy rentier income streams. Credit used to purchase unproductive consumption creates debt-serfdom; credit used to buy rentier assets adds to wealth and income. Unfortunately the average household does not have access to the credit required to buy productive assets; only the wealthy possess that perquisite.

And so the rich get richer and everyone else gets poorer.

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:  1. Debt and financialization

1. Debt and financialization

2. Crony capitalism and the elimination of accountability 3. Diminishing returns 4. Centralization 5. Technological, financial and demographic changes in our economy Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of

the same coin: once we accept responsibility, we become powerful.

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

NOTE: gifts/contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Subscribers ($5/mo) and contributors of $50 or more this year will receive a weekly email of exclusive (though not necessarily coherent) musings and amusings. At readers' request, there is also a $10/month option. What subscribers are saying about the Musings (Musings samples here): The "unsubscribe" link is for when you find the usual drivel here insufferable.

All content, HTML coding, format design, design elements and images copyright © 2013 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I am honored if you link to this essay, or print a copy for your own use.

Terms of Service:

|

Add oftwominds.com

Oftwominds.com #7 in CNBC's

#25 in the top 100 finance blogs

|