|

|

| weblog/wEssays archives | home | |

|

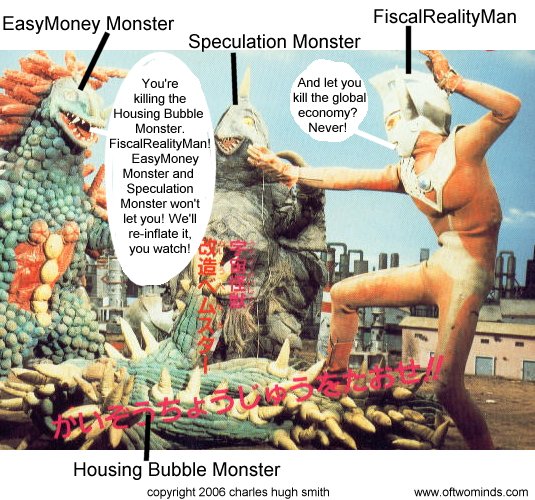

The Housing Bubble: Made in China and Japan? (November 20, 2006) BusinessWeek's lead article, Can Anyone Steer This Economy? observes that "Global forces have taken control of the economy. And government, regardless of party, will have less influence than ever." While it's true that the U.S. government has little control over the U.S. economy, that's not to say government has no influence. I don't refer to the U.S. government, of course, but the central banks of China and Japan, which have enabled the easy money which fed the speculative fever which created the housing bubble. (See illustration below.)

EasyMoney Monster was born from the monstrous marriage of MS (massive liquidity) and LLS (lowered lending standards). Speculation Monster was sired by the union of DSFHYILIW (desperate search for high yield in a low-interest world) and HIASI (housing is a safe investment). By buying U.S. debt in previously unimaginable quantities--over $1.5 trillion in Treasuries alone--the government-run central banks of China and Japan enabled the Fed to lower interest rates to inflation-adjusted zero, fueling a speculative frenzy in U.S. housing. With treasury bonds yielding such low returns (thanks to massive buying of basically zero-return T-bills by the Chinese and Japanese banks), the slightly higher yields on U.S. corporate bonds and mortgage-backed securities looked good to overseas investors and institutions, who then snapped up veritable mountains of private-sector U.S. debt. Since virtually any debt instrument issued in the U.S. is being purchased regardless of yield or risk by foreign banks and institutions (Gulf oil producers' buying has been funneled through London and offshore Carribean banks), there are no brakes on debt creation--or on the speculation such easy money encourages. And why the speculation in housing? In a low-interest world, the yield on bonds is also low, and many investors burned by the dot-com stock market meltdown sought the higher returns and apparently lower risk of real estate/housing. Given easy money, low lending standards and low interest rates, the barriers to entry were lowered to near-zero. No savings? Get a no-down payment loan. Low income? Get a no-document loan. Can't afford the payments? Get an option ARM with low teaser rate and interest-only monthly payments. Is there any wonder these conditions have created a massive speculative bubble in housing? FiscalRealityMan appears to have the upper hand in his battle with the Housing Bubble Monster, but the dynamic duo of the EasyMoney Monster and Speculation Monster will be hard to beat, as long as the Chinese and Japanese governments continue sopping up ever greater quantities of U.S. and lending standards continue to bounce along rock bottom. Why are they absorbing such risky quantities of dollar-denominated debt? To enable the U.S. consumer to keep buying their exports, of course. That strategy has paid off handsomely now for years, but the true cost of the gambit is becoming increasingly obvious: a global speculative frenzy which is blind to risk. For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2006 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |