|

|

| weblog/wEssays archives | home | |

|

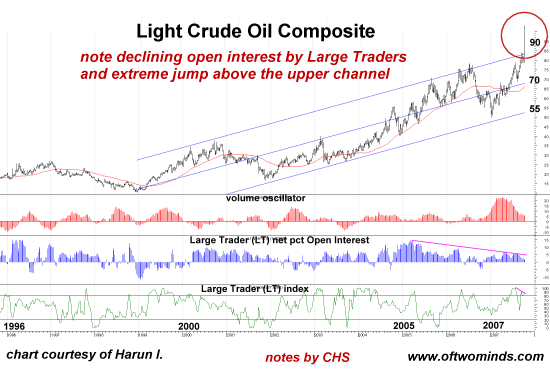

Behind the Curtain II: The Destruction of the Dollar (November 8, 2007) The dollar drop seems to be gathering speed. Many have been predicting the decline of the U.S. dollar would continue, but the speed of its recent decline is frightening to everyone but Ben Bernanke and Hank Paulson--the two people who should not just be worried but who should be acting to arrest the decline. Anyone with a moderate serving of common sense knows what needs to be done: Mr. Bernanke needs to stand up and announce that there will be no Fed Fund rate cuts in December and beyond, as the U.S. is finally going to defend its currency. Why should we care? It's called a vast reduction in the purchasing power of everyone paid in dollars. Oil exporters are paid in dollars, and in reaction to the reduction of value of those dollars the price of oil has jumped. Thanks to frequent contributor Harun I., we have a chart which displays this:

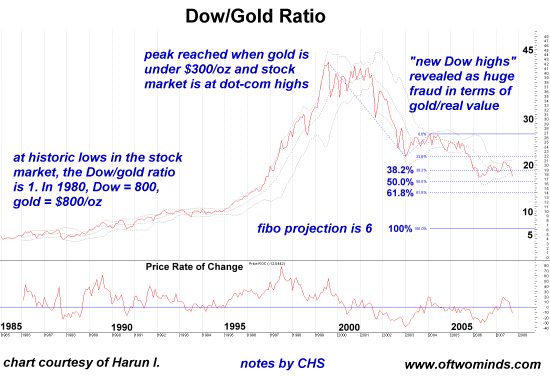

But the U.S. Dow Jones Industrial Average (DJIA) just hit all-time highs; doesn't that mean that we're all making money and the nation is doing just peachy-keen fine? Not if you look at the Dow/gold ratio. Harun was kind enough to provide this chart of the Dow and gold plotted in a ratio. Here's how this works. At real Bear Market lows, such as 1980-81, the ratio is 1, as the Dow was at 800 and gold was $800 per ounce. At the peak of the dot-com bubble, the ratio had soared to 45. Put another way: one share of the DJIA bought 45 ounces of gold. Back in 1980, it bought one ounce of gold. Currently it buys about 16, a loss of 2/3 since 1999. So much for "new Dow highs." Harun plotted some Fibonacci projections on the chart, and this suggests the Dow/gold ratio might descend to 6--meaning the Dow might stabilize at 12,000 and gold will rise to $2,000, or gold might stabilize at $1,000/ounce and the Dow will drop to 6,000.

Whatever the numbers, the reality is owners of U.S. stocks have seen the real value/purchasing power of their holdings decimated. Thank you, Hank and Ben, for destroying our currency to save your banker buddies. The Ministry of Propaganda has been working overtime to reassure us all that $100/barrel oil is "no problem." Like rank weeds popping out after a rain of doubt, suddenly the mainstream media is chockful of stories claiming $100/barrel oil will have virtually no effect on the "diversified, resilient U.S. economy." Various charts are trotted out to prove that the rising cost of energy will have no adverse effects. So next time you pull into the gas station, just fold up a chart from the Wall Street Journal and insert that in your tank. Maybe your vehicle's engine will muster up sufficient belief in the "diversified, resilient U.S. economy" to keep running despite the absence of fuel. The Ministry of Propaganda's most important Big Lie is that there is no inflation. How the MP will manage when oil is $120 and gasoline is $4+ a gallon is a real mystery. Meanwhile, back in the U.S. stock market, money managers desperate to maintain some percentage of their clients' purchasing power are chasing technology stocks higher and higher. There are supposedly so many oil tankers clogging Rotterdam harbor that they can't even offload their cargoes. Hmm. Perhaps the rise in oil is not demand-driven but just another desperate speculative rush to anything but the dollar. If you doubt that the oil market is highly leveraged and highly speculative, please read The Financialization of Oil (March 20, 2007) Ironically, the smart money fleeing the U.S. stock market may be exacerbating the dollar's decline. Those in the know have watched the heavy buying of U.S. Treasuries recently and wondered who the heck is buying Treasuries even as the Chinese and other non-U.S. holders have started to dump their dollars. The answer appears to be managers selling their U.S. stocks and putting the money into "safe" Treasuries. As long as there are fools willing to buy Treasuries, the U.S. Treasury is under no pressure to raise interest rates. The buyers must be domestic, because foreign buyers of Treasuries are losing money hand over fist as the dollar loses more value every day. Thus a stock market meltdown in the U.S. might have the peculiar consequence of encouraging the dollar's continued slide as frantic U.S.-based portfolio managers seek a lousy 4% return rather than suffer gigantic losses in U.S. stock markets. From the point of view of foreign owners, however, the Treasuries are handing them catastrophic losses on a daily basis. Thus we have the Chinese central bankers issuing unveiled warnings that the U.S. had better start defending the dollar lest its bagholders decide to exit the dollar en masse. Unfortunately for the Chinese, Ben and Hank only have ears for their pals on Wall Street. The rest of the world gets a deaf ear. You just lost 10% of your dollar portfolio's value? Too bad; we have to protect our poor little crying friends over at Morgan Stanley, Citicorp, Merrill Lynch, Bear Stearns and Goldman Sachs. All of this makes me wonder if all markets--even those in gold and oil--might not suffer simultaneous collapses. Just from a common-sense perspective, you have to notice that all markets are at extremes: global stock markets, global real estate markets, global petroleum markets and precious metals. So-called "safe havens" are skyrocketing in parabolic rises which usually end in sharp collapses. Could speculative unravelings eventually even reach oil and gold? Given that the paper trading in those markets far exceeds the physical supply's value-- why shouldn't they suffer the same speculative collapse as any other market perched at extremes? If derivatives, futures contracts and options far exceed the actual physical commodities' value, then what happens when speculators have to liquidate positions to cover margin calls or derivative unwindings elsewhere? Even if there are no direct links between these markets, the major players own financial instruments in all markets. As players unwind positions in one market, they might have to sell in another market to cover client withdrawals or other liabilities. Perhaps that's how a meltdown in one apparently isolated market could quickly infect every market at speculative extremes--which is all markets, everywhere. Readers Journal updated 11/09/07 New Haiku, new poems, new essays and more! Please see top-right sidebar. Thank you, David R., ($5) for your thoughtful and much-appreciated donation to this humble site. I am greatly honored by your support and readership. All contributors are listed below in acknowledgement of my gratitude. For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2007 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |