|

|

| weblog/wEssays archives | home | |

|

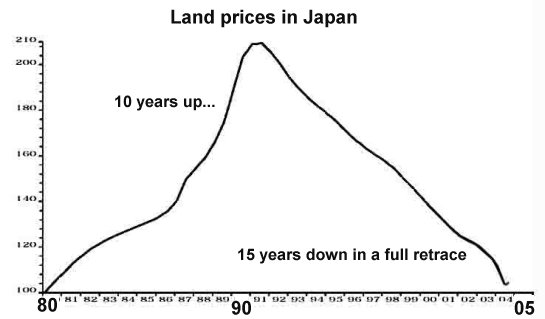

What We Can Learn from Japan's 15-Year Decline in Real Estate (October 31, 2006) A Halloween Scary Story...with Zombies... Frequent contributor Michael Goodfellow suggested I provide some data about Japan's real estate bubble and bust--and just in time for Holloween, here we have some truly frightening charts:

Here we see that Japan experienced a full retrace to the pre-bubble value of real estate. This is typical of valuation bubbles. If the U.S. housing bubble follows this pattern (and why should it deviate from a pattern which has held for hundreds of years, going back to the Tulip Craze in Holland?), then the house that sold for $150,000 in the S.F. Bay Area in 1995 and went for $600,000 in 2005 will eventually retrace to being worth $150,000.

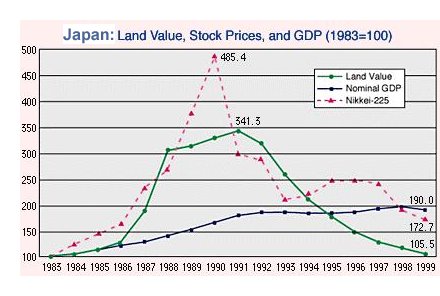

Just for context, here is a chart which shows that the export-dependent Japanese economy actually rose even as the stock and real estate markets were plummeting. To hope that the import-dependent U.S. economy will fare as well would at first glance appear unlikely. Note that that the stock market bubble topped before the real estate bubble, but both tanked, slowly and painfully, for a decade or more. (Note that while the two charts show somewhat different timeframes for the re-trace, the end result is the same.) Here we have a summary from Wikipedia on the Japanese real estate bubble and its aftermath: Prices were highest in Tokyo's Ginza district in 1989, with some fetching over US$1.5 million per square meter ($139,000 per square foot), and only slightly less in other areas of Tokyo. By 2004, prime "A" property in Tokyo's financial districts were less than 1/100th of their peak, and Tokyo's residential homes were 1/10th of their peak, but still managed to be listed as the most expensive real estate in the world. Some US$20 trillion (1999 dollars) was wiped out with the combined collapse of the real estate market and the Tokyo stock market.The key take-away from the charts and summary is this: the Japanese bubble was not in housing, it was in lending. The same is true of the U.S. bubble which is just beginning its deflation. If all mortgages had continued to require 20% down in cash and well-documented sources of income, the bubble would have run out of buyers long ago. How long will it take for the U.S. property bubble to fully deflate? Good question. Japan's property values outside Tokyo and a few other major cities continue to decline fully 15 years after the bubble top. Will the U.S. also suffer a 15-year decline? The answer is less financial than political; Japan's Diet (Federal Legislature) is heavily slanted toward sparsely populated rural districts, and the intertwined nature of business and government is quite different from the U.S. These and other factors (such as the great power of the government financial bureaucracies and the cultural disinclination to mar a facade of normalcy) hindered Japan's ability to grapple honestly with the vast deflation of property and equity assets which left their financial system crippled with non-performing, never-to-be-repaid loans.

Hopefully, the U.S. citizenry will refuse to let the powers that be stand aside and watch numbly as the bubble deflates. If some action akin to the cleanup of the Savings and Loan fiasco of the early 90s (another mess needlessly brought on by no oversight and loose lending standards) were instigated, perhaps the U.S. decline could be shortened to a mere six years or so from Japan's 15-year "Lost Decade." If, however, the government agencies responsible for overseeing financial institutions and lenders allow the lenders to try to re-inflate the bubble via "zombie" loans to "zombie" borrowers, then the pain will only be lengthened and exacerbated--as Japan has so ably shown. As the chart above reveals, government bail-outs have created such a massive public debt that fully 70% of Japan's tax revenues are devoted to paying interest on the public debt. If that doesn't frighten you, then you may already be a zombie. But all that remains to be seen, for the hard years are still ahead. For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2006 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |