| |

How Does a Hedge Work? Here's How

(October 3, 2007)

I recently asked longtime contributor Harun I. to explain (again) how hedging works.

The reason is simple: though hedging is generally presented as something reserved for corporations

and large funds, I have learned from Harun that the concept can be applied by us "regular

investors." For instance: want a hedge against a declining dollar? Buy a gold ETF (exchange-traded

fund) or physical gold or perhaps gold mining stocks (not a perfect hedge due to these being

stocks, but stil....) All offer some hedge against a declining dollar.

Concerned oil might rise? Then a hedge might be futures on oil contracts, or even an oil ETF.

Price of grain rising? Then a futures contract on wheat provides a hedge.

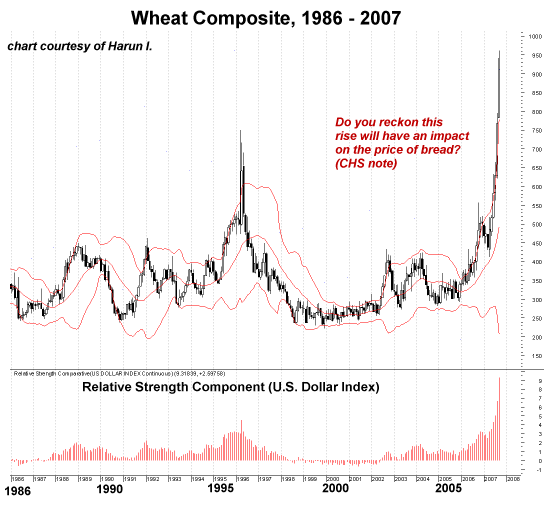

We start with a striking chart of wheat Harun supplied:

I sense that your attention is drawn more to hedging so therefore it is that with which I

will begin.

First, due to definition, we must understand the public will be considered speculators.

Bona Fide Hedgers are those actually engaged in the business of producing or manufacturing

a good or service of which the risks of doing so is what they attempt to offset. Life as a

business doesn’t qualify.

So a bona fide hedger either has a cash position (long cash or actuals) that will be sold at

a later date and therefore has the risk of declining prices or he has to purchase raw

materials to manufacture a product or deliver a service (short cash or actuals) and therefore

has the risk of prices increasing. Processors can carry both risks of increasing and

decreasing prices.

For example, an oil refinery must buy crude oil and is worried about rising crude oil prices.

It must also be concerned about falling prices of the products it delivers, i.e., unleaded

gas or heating oil. A soybean processor must worry about rising soybean prices and falling

prices of soybean meal and soybean oil.

Bona fide hedgers are not trying to make money; they are trying to control costs (protect

their bottom line). As pointed out in The book Way of The Turtle, Southwest Airlines

was able to remain profitable while other airlines struggled because it was able to effectively

hedge its fuel costs. In other words through hedging operations SWA was able to purchase

fuel at a lower effective cost than many of its competitors and pass along the savings to

its customers through lower airfares and profit to its shareholders through higher stock

prices.

Another way of looking at this is to say that SWA effectively transferred the risk

of higher fuel prices (operating costs) to speculators who were willing to assume that risk

in expectation of a reasonable return on investment.

The ability to transfer risk (uncertainty) to those willing to accept it is what enables

stable prices. In the short term price volatility may be substantial but over the long

term prices will be less volatile. Crude oil prices have raised several folds but the major

refineries have remained profitable for the most part and prices at the gas pump have not

risen on a one to one basis with crude oil.

The ability hedge the purchase of Light Sweet Crude in the futures markets have cushioned

the blow of parabolic increases of the raw materials necessary for the production of energy

products.

Whether people like it or not the fact remains that if not for futures markets retail prices

would gyrate wildly as would corporate earnings and therefore stock prices would gyrate

wildly as well as every new development causes stampedes to pass on costs in order to remain

profitable while attempting to keep products affordable.

How does this work at the corporate level? Let say that a major oil refiner, General Guzzler,

has a research report that indicate higher crude oil prices, it is November 2006 when the

hedge was placed and November 2007 when the hedge was lifted. What was the effective or true

cost of the crude oil to General Guzzler?

Cash Market price - Futures Market Price = Basis

$55.00/bbl $57.00/bbl -2 (cash under futures)

$80.00/bbl $83.00/bbl -3 (cash under futures)

(+/- ) in cash market Futures Position Gain (+/-) -1 change

($25.00/bbl)

$26.00/bbl in basis

From the information above we can see that when the hedge was placed the cash market price

Gen Guzzler was trying to protect was $55.00/bbl., futures were at $57.00 when purchased.

When crude oil was purchased in the cash market a year later it was $25.00/bbl more expensive.

However the futures market position when offset was profitable having made $26.00/bbl.

If we subtract the futures market gain of 26 from the cash market purchase price of 80 we

see that not only was the 55 target price protected, Gen Guzzler actually made $1.00/bbl as

the effective price was $54.00/bbl., reducing costs even further.

Another way to figure

the effective cost is to simply add or subtract the gain/loss of the change in basis from

the original cash market price of $55.00/bbl.. Even though prices are now substantially

higher production costs have been kept in line and Gen Guzzler can deliver a product that

is affordable and earn a profit.

Had Gen Guzzler not hedged, it would have had to purchase oil at $80.00/bbl instead of

$54.00/bbl which means in order to stay profitable the increase has to be past on to the

consumer. This increase would likely crush the end user and therefore the economy within

a year.

Do all hedges work out this way? No. But being exposed to basis risk (the ability

to transfer risk) instead of full price risk helps to stabilize profit margins to corporations

and prices to end-users. Yes, prices are high but without hedging it could be much worse.

As consumers we conduct the business of life. The business of life is fraught with risks.

There is currency risk, which is the risk that our dollars will buy less tomorrow than

today. There is supply/demand risk, which is the risk that demand will increase for a product

or service forcing prices higher or that supplies will be inadequate forcing prices higher.

This is inclusive of the cost of money. These risk affect everyone from small business

owners to the bagger at your supermarket.

Therefore it could be inferred that one must have a plan to offset these risks to at least

maintain ones standard of living. We can do that by educating ourselves to understand our

risks and then find suitable ways to hedge those risks. How many remember the high price of

sugar in the 1970s?

Wheat has experienced a rather parabolic bull run of late (see chart). Should high prices

persist or increase even more how will that affect ones ability to purchase the foodstuffs

derived from wheat? And now that you are spending more for food out of a given amount of

money, on what areas of spending will you cut back? By using the real principles of hedging

as used by the fictitious Gen. Guzzler Corporation can I keep my effective costs reasonable

and therefore protect my standard of living? The answer is yes.

Is this without risk? No. There is always risk. As in the example above basis risk reduces

risk it does not eliminate it. The leverage in futures markets due to small margins is a

double-edged sword and to the uneducated or irresponsible can create losses beyond ones means.

There are ways to control or reduce risk whether through option strategies or just arranging

with the broker not to use full margin (putting up the full value of the contract). One can

use the stock market, e.g., purchasing gold miners instead of gold. There are ETFs and

commodity index funds.

Is this advice? No. It is an invitation to think differently. The Internet and libraries

are full of information on how to assess your financial condition so that you may make

prudent decisions about what investment risks are suitable. Of course this assumes that

one is honest with oneself. By taking charge and controlling your financial state you

become less dependent on the government (in reality other tax payers) for your existence.

This reduces the need for large, intrusive government.

Thank you, Harun, for an excellent explanation of an often-mystifying subject. This idea

of hedging is a powerful concept in times when our purchasing power is declining, either

via obvious inflation or slight-of-hand via our currency being destroyed.

Thank you, Anthony S., ($20) for your much-appreciated third donation to this humble

site. I am greatly honored by your contribution and readership.

All contributors are listed below in acknowledgement of my gratitude.

For more on this subject and a wide array of other topics, please visit

my weblog.

copyright © 2007 Charles Hugh Smith. All rights reserved in all media.

I would be honored if you linked this wEssay to your site, or printed a copy for your own use.

|

|