|

|

| weblog/wEssays archives | home | |

|

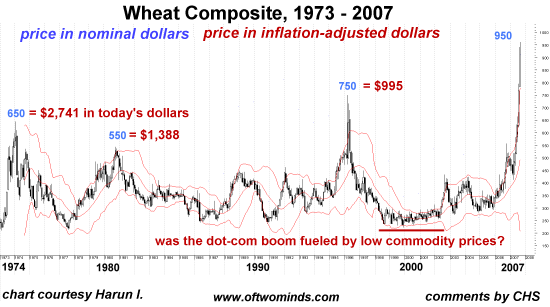

How We Can Have Both Inflation and Deflation (October 17, 2007) Readers ask: what does the future hold? Inflation or deflation? My answer: both. Take a look at this chart of wheat prices (courtesy of Harun I.) over the past 24 years. Note the prices in blue are nominal (historical) and the prices in red have been adjusted for inflation as per the Bureau of Labor Statistics.

While many commentators insist inflation is a monentary phenomenon (too much money chasing too few goods), I humbly submit that the forces of scarcity (supply and demand) act on commodity prices regardless of whether money supply is increasing or decreasing. This chart of wheat is a good example of supply and demand setting prices, not monentary policy. Each spike represents a shortage, i.e. an imbalance between supply and demand--or perceived supply and demand. Even as wheat soars in current dollars to $1,000/100 bushels (i.e. $10/bushel), we note that in current dollars, the price spike in 1974 reached $27.41/bushel, and the spike in 1980 hit $13.88. So today's price is by no means a "new high" or even an extreme. As I noted on the chart, the period of the dot-com stock bubble coincided with low commodity prices, not just in wheat but also in corn, gold and oil, which sank to $10/barrel in 1999. The force behind the increase in demand for agricultural and petroleum products is the worst-kept secret in the world: the increasing prosperity of the 2.3 billion citizens of China and India. Most observers believe this increase in wealth (and the resultant demand for more and better food and transportation) is unstoppable. If this is true, then we can anticipate looking back on $10/bushel wheat with fond affection for its relative "cheapness." But monentary policy (heedless expansion of money supply and credit) does of course have consequences in asset pricing, as shown by this graphic history of the Dow Jones Industrial Average:

And here's another manifestation of massive credit expansion, commercial paper (short-term loans):

And last but certainly not least, let's not forget the credit-fueled Mother of All Housing Bubbles:

The list of extremes being fed by monetary expansion (money supplies growing by 18-20% annually in economies growing 3% annually) is endless. Here is a chart of derivatives.

A key observation is that all asset classes have skyrocketed in unison in this debt-based "prosperity." Global real estate markets have climbed to the stratosphere in lockstep with emerging stock markets, collectibles, gold and other commodities. That correlation makes all asset classes vulnerable to a global downturn. As credit tightens and fear returns to "reprice" loans and risk, then money availability drops and a rapid, across-all-asset-classes deflation will occur. For example, here is my projection of the whimpering endgame of the housing bubble:

The trillion-dollar question is this: will the coming global deflation in assets reduce demand for food and oil? If so, then even commodities like wheat and oil will plummet in price. If not, then we may experience inflationary prices in commodities (i.e. getting the same item but paying a lot more for the privilege) even as our assets (real estate, stocks, bonds and collectibles) drop in value.  We also have to remember that supply is not necessarily as elastic as demand.

We also have to remember that supply is not necessarily as elastic as demand.

If there is a demand for more houses (a fading memory, to be sure), then we can collectively go out and build more houses. This is not so easy when it comes to finding new super-massive fields of petroleum or growing more wheat; little things like massive crop failures and drought can radically change the supply of corn, wheat and soy beans regardless of demand. If we recall that the majority of wheat available for export is grown in Canada, Australia and the U.S., we begin to understand the true fragility of global supply. How would a crop failure (a regular occurance in the historical record) in any one breadbasket effect the global price? It's a question worth asking as food inflation in China reach 20% per annum. Food-price fears in China (The Economist) If we look at the chart of wheat prices above, how can anyone be surprised by the rampant food inflation in China, and indeed, just about everywhere? Thank you, James Kunstler, ($100.00) for your heart-warming and extremely generous donation to this humble site. I am greatly honored by your support and readership. All contributors are listed below in acknowledgement of my gratitude. For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2007 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |