|

|

| weblog/wEssays archives | home | |

|

The Big One Just Hit (September 8, 2007) Here in California we refer to the next catastrophic earthquake as The Big One--not a modest little 7.0 temblor like Loma Prieta in 1989, but a massive 8.0+ quake like the 1906 event which devastated San Francisco. The financial Big One hit today. Though the markets are still standing, the apparently modest damage is illusory--deep inside, the supports have broken. Over the next few weeks, we will witness a seemingly sound structure start collapsing under its own weight--the global house of structured debt. Though to the naked eye it seemed to have survived today's modest financial quake, reverberating shock waves will soon bring it down. Let's start with a chart of the U.S. dollar index. The mainstream media is full of stories about the Federal Reserve cutting rates, but the bigger story--the fall of the dollar below the multi-decade support level of 80--was barely mentioned.

Note that this dip below 80 is not likely to be the bottom. MACD and RSI are dropping in a manner which suggest more downside is highly probable. Readers, I cannot overstress the vast importance of this break below 80. This is truly an earthquake which is rumbling through flimsy shacks and brittle highrises from Japan to New York. The effects are multiple and deeply adverse. As the dollar drops, the yen strengthens. Yes, the yen has dropped along with the buck--much to the annoyance of the Europeans, who have seen their currency the Euro strengthen relentlessly as the buck and yen did a two-step downward. Now, however, the yen has finally begun to rise as the dollar drops. Why do we care? Here's why: the yen carry trade has supported U.S. equity and lending markets on a gargantuan scale. What's the carry trade? Borrow $200 billion in Japan at 1% interest rates and then invest the borrowed funds in Treasuries paying 4.5%, or leverage the money into derivatives or equities purchased on margin. Though I am not an expert on the carry trade, I have read that it is no longer profitable if the yen is below 115. The yen is 113 and heading lower. Forcing traders to sell dollar-based assets and repatriate the funds into yen--the so-called unwinding of the trade--requires stupendous selling of equities, derivatives and bonds--whatever was purchased with the borrowed money. A key prop under the U.S. market has been kicked out. As we all know, the U.S. requires vast flows of capital from foreign banks, institutions and investors to prop up our colossal deficits and debt markets. We need foreign buyers for our Treasuries, corporate paper, mortgage-backed securities, and other financial assets. Because we run a truly staggering trade deficit--on the order of $800 billion a year--foreign banks have a lot of dollars to recycle somewhere. So they have bought Treasuries and hundreds of billions in other debt--you know, like all those CDOs and MBS which are blowing up/being revealed as worth far less than advertised. All that is peachy--until the dollar weakens below 80. Why buy an asset in dollars if you fear the dollar will lose 20% of its value in a few months? What exactly is so "safe" about a Treasury in which you can lose 20% of your capital? Nothing. It's a lousy investment. Technical analysts such as Louise Yamada have been warning for years that there is no support under 80 for the dollar-- there is literally no bottom. Why do we care? Because the Treasury and the Fed have to worry what happens if they let the dollar drop to 76, then 70, then 65 and then who knows how low. While the MSM is focused on the Fed bailing out Wall Street speculators and those who gambled on housing and lost, the Really Big Board Game--foreign currency exchange--makes the domestic-economy interest-rate noise look like a couple of kids playing tiddly-winks. Can the Fed really afford to sacrifice the dollar, and hence the entire U.S. position in the global financial structure to placate a few loud-mouthed TV entertainers (Oops I mean "analysts") and pandering politicos? This is why the Fed and other central banks are playing around with all these "liquidity enhancement" games; they all fear a collapse in the dollar and are absolutely loathe to see the Fed cut interest rates, which would sink the dollar faster than the torpedo which sank the Lusitania (the grand ship sank in half an hour). What games? Frequent contributor Harun I. sent in this clipping: Huge Mushrooming in Central Banks' Liquidity PumpingOnly an insanely irresponsible and/or stunningly ignorant speculator would have the Fed undercut the dollar to save some gamblers' soft hides. If Bernanke truly understands the Big Board Game, he will stand pat on the Fed funds rate. Even pandering with an essentially meaningless 25 basis-points drop will send the signal all central banks dread--the U.S. will let the dollar plummet, regardless of the losses which will be suffered by foreign holders of the buck and dollar-denominated assets. At that point, all financial heck will break loose, and idiots who were screaming for 50 bp or more cuts will be standing on the sidelines wondering what hit them and their speculating pals. Next chart: the astounding level of precarious debt which is currently balanced on the crumbling foundation of consumer spending.

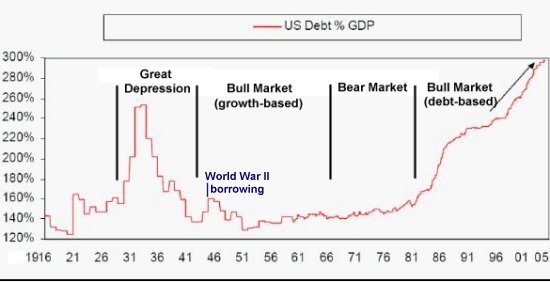

Do you really think throwing more debt into the economy is going to help matters? Note that we now stand on a precipice even higher than the one which brought on the Great Depression. Bernanke is on the record claiming that looser money (more liquidity) would have ended the Great Depression. But if you've lost your shirt gambling, then who will be dumb enough to lend you more money? Even with a pool of limitless funds, no one wants to lend money which will promptly be lost; and responsible people will have no desire to borrow more, regardless of the interest rates. Please note that interest rates in Japan have been 1% for 15 years--and their "recession" continues apace. So much for the notion that limitless liquidity will end any recession that was caused by too much liquidity and borrowing in the first place. Did you notice that the economy lost jobs for the first time in four years? Do you reckon that might eventually cause a decline in consumer spending? As Mish has painstakingly described, the employment number is loaded with completely fraudulent "ghost jobs" which the Bureau of Labor Statistics is pleased to assume were created with zero evidence. So the reality is probably 120,000 jobs were lost, not 4,000. How healthy is the American family's balance sheet? Let's look at a chart:

Despite all the endless reassurances that the U.S. consumer remains "healthy," does this look like a healthy chart to you? This is a snapshot of financial ruin--expenditures outstripping income to a fearsome degree. Knowledgeable correspondent Fabius Maximus noted that such aggregate numbers don't reveal the true precariousness of the middle-class and lower-middle-class American households' finances. Income and wealth are too concentrated in the US for aggregate numbers to tell us much. It's too coarse a view. Instead one must use segment analysis, looking at the situation of average households in the 2nd and 3rd quintiles of income or wealth. The census has the numbers.Thank you, Fabius for this cogent analysis of the crumbling foundations of the U.S. household's balance sheet. Lastly, we all have heard about housing sales dropping 12%, (the actual number of escrows closing may well drop 40%--not that the number will be released), of house prices dropping 3% in just a few months--even cheerleaders are confessing that the housing bust is in full swing. Let's turn to the ramifications of this bust on the U.S. economy. Here is a good recap from CBS Marketwatch: What will send the U.S. into recession? But critics say the Fed's rate cuts can't produce a miracle. The credit crunch on Wall Street reflects an unwillingness to lend because of a lack of trust, not a lack of funds. Until the markets get rid of the chaff, the price of credit isn't going to be that important.As for the global nature of the meltdown, consider this Bloomberg article sent in by longtime correspondent Ken K.: CDO Losses Can't Be Quantified, France Regulator Says Prada called for global regulators, banks and investors to develop an information warehouse where all CDOs, bonds based on pools of debt and other assets, would be recorded so that the risk of losses can be quantified. The CDO market should replicate the Depository Trust & Clearing Corp., which has monitored credit-default swap trades since last year, Prada said.To summarize: 1. Lowering the interest rates will trigger a decline in the dollar with unknown but potentially fatal results which can only be fixed with much higher interest rates in the future. 2. The U.S. household is staggering under an unprecedented burden of debt, which it has created by borrowing and spending more than its income can possibly support. 3. Lowering the Fed funds rate will not rebuild the shattered structure of global risk appetite and trust; that is irrevocably broken. 4. Lowering the Fed funds rate will not rebuild the American consumers' balance sheets which have been irrevocably broken by the decline in housing values. 5. Lowering the Fed funds rate will not enable households to extract more equity to spend--that tool is broken. 6. Lowering the Fed funds rate will not create new jobs or stop the erosion of jobs which has--despite painfully obvious official suppression of reality--finally become visible to all. So exactly what will a Fed funds rate cut do? I am reminded of the schoolyard joke about the short-term benefits of peeing in your pants: it will give the stock market a warm feeling for a very brief moment. Thank you, Daren W., ($15) for your much-appreciated donation to this humble site. I am greatly honored by your support and readership. All contributors are listed below in acknowledgement of my gratitude. For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2007 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |

There's a big disagreement among economists about the role of mortgage-equity withdrawal in

consumer spending over the past five years. Contrary to Feldstein's position, some don't believe

it's had any impact at all. (CHS: you mean $1.5 trillion had no impact at all??)

There's a big disagreement among economists about the role of mortgage-equity withdrawal in

consumer spending over the past five years. Contrary to Feldstein's position, some don't believe

it's had any impact at all. (CHS: you mean $1.5 trillion had no impact at all??)