|

|

|

||||||||||||

|

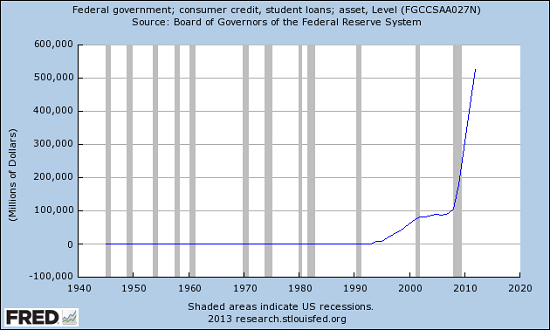

Our Huge, Stinking Mountain of Debt: Student Loans (September 11, 2013) Imagine a huge, stinking mountain of debt, which represents all of the debt in the world... now look at this chart of student loan debt. Notice anything about this chart of student loan debt owed to the Federal government? Direct Federal loans to students have exploded higher, from $93 billion in 2007 to $560 billion in early 2013. This gargantuan sum exceeds the gross domestic product (GDP) of entire nationsfor example, Sweden ($538 billion) and Iran ($521 billion). Non-Federal student loans total another $500 billion, bringing the total to over $1 trillion. Does this look remotely sustainable? Does it look remotely healthy for students, society, taxpayers now on the hook for a half-trillion dollars in potential defaults or the U.S. economy?

Frequent contributor Jeff W. explains the underlying dynamics of this wholesale shift of student-loan debt to Uncle Sam: Why did Uncle Sam take over the student loan business? I dont know for sure, of course. But I surmise that it has to do with the nature of debt money. As debt money is being created, it stimulates aggregate demand and circulates in the economy creating (false) prosperity. As long as the government and central banks can keep pumping new debt money into the economy, the economy runs well enough to keep the sheeple satisfied, e.g., housing bubble debt creation years, especially 1992-2006. The banks also profit enormously from the creation of trillions of dollars of new debt money. Thank you, Jeff, for an insightful overview of the state's role in pumping debt money into the economy and transferring risk to the taxpayers. When one pile of stinking debt becomes too risky for the bankers, this pile is transferred to the Federal government and the taxpayers. Haven't we seen this before? Hmm....are there any possible consequences of this huge, stinking pile of Federal debt expanding?

The Nearly Free University and The Emerging Economy: The Revolution in Higher Education Reconnecting higher education, livelihoods and the economy With the soaring cost of higher education, has the value a college degree been turned upside down? College tuition and fees are up 1000% since 1980. Half of all recent college graduates are jobless or underemployed, revealing a deep disconnect between higher education and the job market.

It is no surprise everyone is asking: Where is the return on investment? Is the assumption that higher education returns greater prosperity no longer true? And if this is the case, how does this impact you, your children and grandchildren?

The Nearly Free University and the Emerging Economy clearly describes the underlying dynamics at work - and, more importantly, lays out a new low-cost model for higher education: how digital technology is enabling a revolution in higher education that dramatically lowers costs while expanding the opportunities for students of all ages. The Nearly Free University and the Emerging Economy provides clarity and optimism in a period of the greatest change our educational systems and society have seen, and offers everyone the tools needed to prosper in the Emerging Economy.

Read the Foreword, first section and the Table of Contents.

Kindle edition: list $9.95, for one week only, $7.95

(20% discount)

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify. We will cover the five core reasons why things are falling apart:  1. Debt and financialization

1. Debt and financialization

2. Crony capitalism 3. Diminishing returns 4. Centralization 5. Technological, financial and demographic changes in our economy Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Once we accept responsibility, we become powerful.

NOTE: gifts/contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Subscribers ($5/mo) and contributors of $50 or more this year will receive a weekly email of exclusive (though not necessarily coherent) musings and amusings. At readers' request, there is also a $10/month option. What subscribers are saying about the Musings (Musings samples here): The "unsubscribe" link is for when you find the usual drivel here insufferable.

All content, HTML coding, format design, design elements and images copyright © 2013 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I am honored if you link to this essay, or print a copy for your own use.

Terms of Service:

|

Add oftwominds.com

|