|

|

| Readers Journal blog | home | |

|

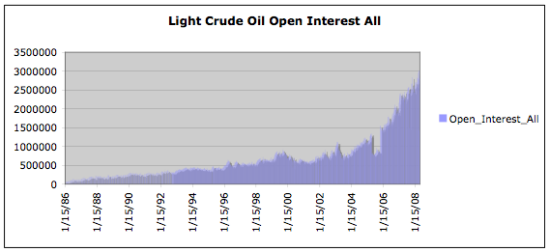

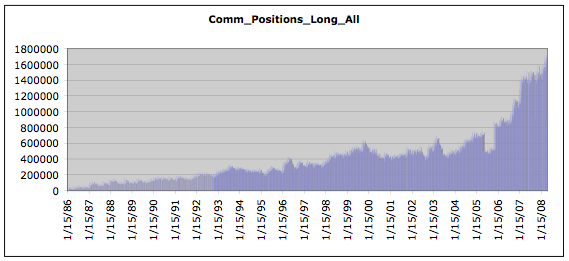

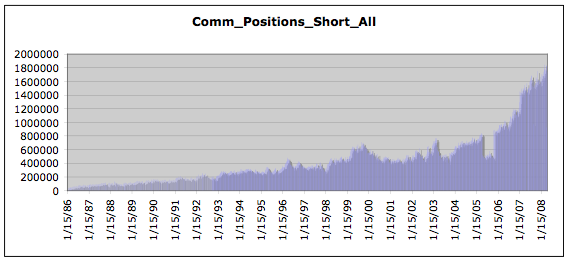

The Rise in Oil: Speculation or Uncertainty? (Harun I., May 17, 2008) RE: PERHAPS 60% OF TODAY'S OIL PRICE IS PURE SPECULATION (Financial Sense): The author wages a largely rhetorical argument. I won't argue that there may be a bubble building in energy futures but the causes he presents is suspect. The CFTC is not doing its job? Nonsense. The margin for Light crude is over $12,000 for speculators up from $3,000 which exchanges raised (without prompting from the CFTC) to protect their interests. How many small traders have that kind of money to put up? Judging from the CFTC COT Report (NonRept traders chart) not that many from a historical view point. Commercials making a killing? Not according to their Long and Short Open Interest Charts which are nearly even. But Commercials are not trying to make money, they are trying to control costs.

Are large speculators making money, yes they are. Their longs outweigh their shorts significantly. They should make money, they are accepting the risk commercial don't want and deserve a return on their capital for doing so. He also posits that the run up is due to deregulation as of the CFMA but OI for hedger and speculators dipped after 2000 and stayed reasonable until 2006. Blaming OTC derivatives lack of reporting might make sense but the problem with that is the OTC Forex market is unregulated as well and I think few would argue that it dwarfs the entire US equity markets let alone energy futures. The implication is that certain interests are trying to run a corner. The problem with cornering the market has always been to whom do you sell once you are the market. The public has been priced out (because of high margins). Further, if one examines Forex and now energy OTC exchanges one will likely find they are very similar to the bucket shops that written about in Jesse Livermore's tale. And most professional traders I know won't go near unregulated exchanges. I personally know men who have turned a few thousand dollars into millions within months and these gunslingers warned me off these exchanges early in my trading career saying that these exchanges were "disasters waiting to happen." Remember when I noted large commercial net long positions in Soybeans when prices were low and ethanol was not a concern? Well obviously they (commercials) knew something everyone else didn't. The price spike prior to the first Gulf war did not result in a large increase in OI and therefore did not confirm price. Today no such divergence exists. Commercials are either hedging uncertainty or hedging something of which they are certain. The fact that there are surpluses is not supported by a market that is inverted (i.e. front month trading at a premium to deferred months). Carrying costs (storage, interest, insurance) should make deferred contracts trade at a premium to the front month simply because of time. Does this imply hoarding? If so why? Remember a military without access to adequate energy supplies will be defeated in time in a large protracted conflict. I'm am not saying that he is wrong, I merely posit that the evidence provided in his article is insufficient (for me) to agree to his conclusion. When markets go up and cause pain it is said out of control speculators are bidding up the market. When a market comes under heavy selling pressure we hear about unscrupulous short sellers (e.g, George Soros shorting British Pound). By now one would hope the inanity of such arguments was apparent. By the way ICE now trades all the softs and US Dollar index. NYBOT is no more. Will this lead to rampant speculation in these areas as well? Everyday, buying agents and selling agents get together and negotiate forward contracts. These contracts are negotiated at either agreed upon price or market price at delivery. Then the firms of both parties assess their risks and send their orders to the floor of the respective futures market to transfer price risk to those willing to accept it for a reasonable return (speculators), buyers are going long to protect against rising prices and sellers are going short to protect against lower prices. With this in mind why would purchasers come into the market with bids that hurt them or take offers likewise when there is a surplus? Anyway, it is because of this process that prices stay pretty much tied to supply/demand in the futures markets. If prices get too far out of line arbitragers see the riskless profit opportunity and their activities bring prices back in line. In actuality only 3% of futures contracts are ever "delivered".

Once again, I don't know if he is right but I'm skeptical.

All content, HTML coding, format design, design elements and images copyright © 2008 Charles Hugh Smith, copyright to text and all other content in the above work is held by the author of the essay as of the publication date listed above. All rights reserved in all media. The views of the contributor authors are their own, and do not reflect the views of Charles Hugh Smith. All errors and errors of omission in the above essay are the sole responsibility of the essay's author. The writer(s) would be honored if you linked this Readers Journal essay to your site, or printed a copy for your own use. |

||

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||