|

|

|

|||||||||||||

|

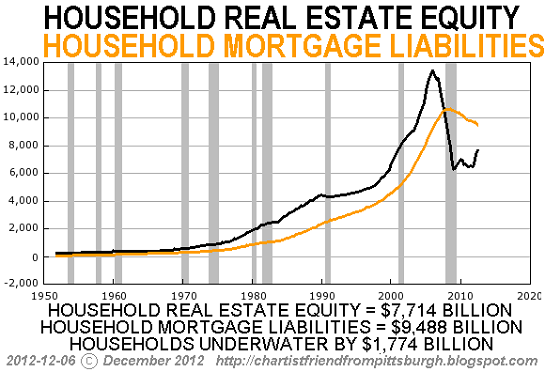

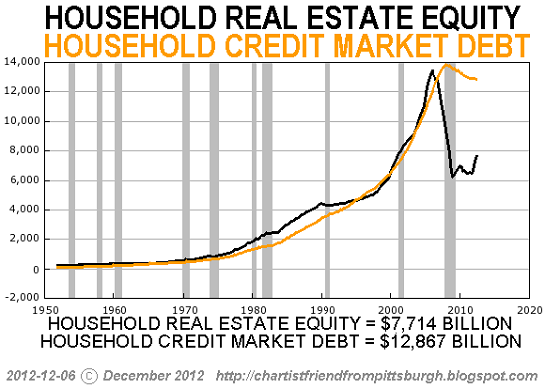

Essays in Fragility: The Rise and Fall of Phantom Housing Collateral (December 13, 2012) How much phantom housing collateral is still on the books? Nobody knows, and that in itself renders the housing/mortgage sector fragile. Mortgage debt doubled in a mere decade. If we go back to pre-bubble 1997, residential mortgages totaled $5.1 trillion. (Source: mortgage debt outstanding, 1959-2003). This was roughly 50% of real GDP of $10 trillion (source: Real U.S. GDP). At the top of the bubble, residential mortgage debt was $10.57 trillion, more than double the total of 1997. (Source: Balance Sheet of Households, Federal Reserve). This was 79.3% of real GDP--a rise of 30%. As a percentage of disposable personal income, mortgage debt rose from 53% in 1960 to 113% in 2003. Income rose over those 43 years, of course, but mortgage debt rose much faster. Mortgage debt has declined as lenders have written off losses. Mortgage debt has declined from $10.56 trillion in 2007 to $9.48 Trillion in 2012. Is it coincidence that this $1.1 trillion decline equals the Fed's purchases of mortgages since 2009? The World's Largest Money-Laundering Machine: The Federal Reserve (October 8, 2012) "The Fed is now where mortgages go to die" -- Catherine Austin Fitts This reduction in debt and the recent modest increases in housing prices has pushed homeowner's equity up from $6.7 trillion in 2009 to $7.7 trillion in 2012. That extra $1 trillion has raised owner's equity as a percentage of household real estate up from an abysmal 39.8% to 44.8%--but this is a far cry from the $10.2 trillion in equity logged in 2007. (Recall that 1/3 of homes are owned free and clear, with no mortgage at all. In these cases, homeowner equity is 100% of the market value of the home.) Courtesy of Chartist Friend from Pittsburgh, here are two charts contrasting housing equity with debt: the first is mortgage debt, the second is total household debt.

Note the "wealth effect" as housing values soared, providing collateral for more debt, and the "reverse wealth effect" as phantom collateral vanished.

Was the equity in the bubble years real or phantom? It was real for those who sold and turned the bubble equity into cash. But how many of the 75 million mortgage holders sold and did not acquire another mortgage? Given that the number of mortgages has barely budged (around 50 million), not many. For everyone else, borrower and lender alike, the equity and the collateral were phantom. This rise and fall of phantom collateral leads us to ask: how much of the $17.2 trillion in household real estate is still phantom? How many homes on lenders' books are valued higher than their real market value? How durable is this "housing has bottomed" surge in prices if the global economy slides into recession? Why ask these questions? Consider this chart of income, courtesy of Doug Short:

If mortgage debt has fallen 10%, and household income has also declined by about 10%, then what's changed? Recall that roughly 50% of household income flows to the top 10%. If the income of the top 10% rises while the income of the lower 90% falls, the median income will be skewed. In other words, the declines experienced by the lower 90% may well exceed the 9% shown on the chart. As a percentage of disposable income and GDP, mortgage debt is still at historic highs. The fact that mortgage debt is down from its bubble highs does not mean all phantom collateral has vanished. It only means that all interested parties, borrowers, homeowners and lenders alike, have a stake in promoting the claim that housing has bottomed. Where would households' ability to borrow be if housing and income both decline? In a way, the Status Quo is desperately trying to boost housing to compensate for the reduction in income. What's left to leverage if both income and equity are declining? So here's the basis for the "bottom is in": 1. The global economy is sliding down a slippery slope into recession. 2. Real household incomes have declined by 10% or more. 3. Mortgage rates are already at historic lows and cannot fall much more, if any. And last but not least, systemic mortgage fraud is a thing of the past: if you forget about rule of law and justice, that is:

How much phantom collateral is still

on the books? Nobody knows, and that in itself renders the housing/mortgage sector

fragile.

Things are falling apart--that is obvious. But why are they falling

apart? The reasons are complex and global. Our economy and society have structural

problems that cannot be solved by adding debt to debt. We are becoming poorer, not

just from financial over-reach, but from fundamental forces that are not easy to identify

or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization

2. Crony capitalism and the elimination of accountability 3. Diminishing returns 4. Centralization 5. Technological, financial and demographic changes in our economy Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of

the same coin: once we accept responsibility, we become powerful.

To receive a 20% discount

on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter

discount code SJRGPLAB. (This is the only way I can offer a discount.)

Please click on a book cover to read sample chapters

NOTE: gifts/contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Subscribers ($5/mo) and contributors of $50 or more this year will receive a weekly email of exclusive (though not necessarily coherent) musings and amusings. At readers' request, there is also a $10/month option. What subscribers are saying about the Musings (Musings samples here): The "unsubscribe" link is for when you find the usual drivel here insufferable.

All content, HTML coding, format design, design elements and images copyright © 2012 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I am honored if you link to this essay, or print a copy for your own use.

Terms of Service:

|

Add oftwominds.com

|