|

|

|

|||||||||||||

|

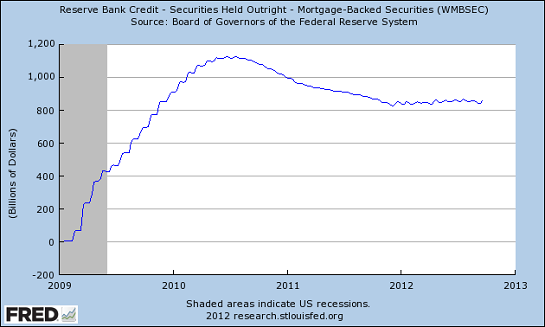

The World's Largest Money-Laundering Machine: The Federal Reserve (October 8, 2012) The Fed policy's first-order effect is to issue hundreds of billions in "free money" to banks; the second-order effect is to destroy the rule of law in the U.S. Let's start with a few questions about the proper role of the Central State and Central Bank: why should they bail out private banks? The answer boils down to something like this: "If the private banks absorbed the losses that are rightly theirs in a capitalist system, they would implode. Since the State and Central Bank have enabled these private banks to infiltrate and dominate the nation's financial system, that system is now hostage to these private 'too big to fail' banks." In other words, "capitalism" in America now means socializing losses and privatizing profits generated by State and Central Bank intervention. Imagine for a moment the "beauty" of this system for owners of private banks: in a truly socialized banking system, the taxpayers would absorb any losses, but the State would also benefit from any future bank-sector profits. In the U.S. system, the losses are socialized but the people draw no benefit; the profits flow to the top 1/10th of 1% private financiers. This is the perfection of State-financier crony capitalism. Let's next ask why the Central State and Central Bank should subsidize and bail out the mortgage industry, a major component of private banking. Once again we find losses are neatly distributed to the citizenry while the profits all flow to private hands. Given that 98% of all mortgages are backed or guaranteed by Federal agencies (Fannie Mae, Freddie Mac, Ginnie Mae, FHA, VA, FmHA, etc.), the mortgage market is already completely socialized: the taxpayers are on the hook for any and all losses, but the profits from originating and servicing the loans are all private. Meanwhile, 1 out of 6 FHA insured loans are are delinquent, and everyone who cares to examine the ledger knows the taxpayers will soon be bailing out FHA just as they did Fannie Mae and Freddie Mac. But the socialization of losses and privatizing of profits is only the first-order effect of the banks' capture of the State. The second-order effect is even more destructive: the rule of law has been subverted by the world's largest money-laundering machine, the Federal Reserve. Once again we can start by asking why a nation's Central Bank should buy mortgages from private financial institutions. Once again the first answer is a variation on the same theme: the Central Bank prints money and buys the mortgages as a way of socializing private losses and passing through billions of dollars in "free money" to private hands. The newly printed money robs purchasing power from every holder of the currency (the socialization of costs) while the immense flood of "free money" flows to private hands. Here's how it works. We know Fannie Mae is absorbing losses of 50% to 65% on its foreclosed properties (Nearly half of Fannie Mae REO unable to reach market, via U. Doran), and we also know that 31% of all homeowners with mortgages are "underwater," owing more than their house is worth (Housing, Diminishing Returns and Opportunity Cost). We also know the Federal Reserve bought $1.1 trillion in MBS (mortgage-backed securities) in 2009-10, and the Fed has announced its intention to buy $40 billion more MBS a month until the housing bubble re-inflates or Doomsday, whichever comes first.

The Fed also bought $1 trillion in Treasury bonds, monetizing Federal debt:

Let's say you own a portfolio of mortgage-backed securities and your pals at the Fed are willing to buy the garbage at full price, no questions asked: are you going to sell your few AAA-rated MBS, the good stuff, or are you going to sell them the absolute dregs, the MBS so stuffed with defaulted mortgages that you've never dared to even do a mark-to-market estimate of their real worth? You dump the worst of your portfolio, naturally, and so in effect the $1.1 trillion in MBS the Fed bought with newly created cash was probably worth (charitably) $600 billion at best. That means the Fed not only wiped out the losses that should have accrued to the owners of the impaired mortgages by removing the MBS from their books, it handed the owners (banks, pension funds, etc.) a cool $500 billion in "free money" by paying full value for massively impaired assets. Since there is about $9.7 trillion outstanding mortgages (down from $10.3 trillion at the top of the bubble--not much deleveraging going on here), the Fed could have paid off 10% of every outstanding mortgage in the country with that $1.1 trillion. The one-time payment of principle would have flowed right to the mortgage owners, just like the Fed's "gift purchase" did, but in this case the money would have reduced the principle owed by homeowners, reducing their debt directly. Setting aside the ethical implications (what about those who have no mortgage, etc.), the difference between the way the $1 trillion flows to the mortgage owners is remarkably different: in the first case, the homeowners get nothing and the banks get $500 billion in free money. In the second case, the banks still get the $1 trillion, but because it flowed through the borrowers, it reduces the mortgage principle. Since the Fed can create unlimited money, why not pay off every mortgage in the land? That's only $9.7 trillion, and if the Fed wanted to unleash an orgy of spending, that would certainly do it. Trillions in losses would be filled with "free money," since the Fed would pay the full value of all mortgages. This thought experiment reveals the real agenda of the Fed's asset purchases: it's not about aiding the nation or borrowers, it's all about funneling "free money" to the banks to restore their balance sheets and profits. There's another reason, one outlined by Catherine Austin Fitts: QE3 Pay Attention If You Are in the Real Estate Market. Correspondent Jim S. has alerted me to the wide-ranging consequences of the Fed's money-laundering, and correspondents Chad D. and Stephen N. also directed me to this article. The second-order purpose of the Fed's mass purchases of mortgages is to recycle dodgy phantom mortgages--in effect laundering the debt and money on a vast scale. Here is an excerpt from Fitts' analysis:

The Fed is now where mortgages go to die. Thousands of mortgages on homes that do not exist or on homes that have more than one first mortgage are now going to the Fed to disappear. Thousands of multifamily and commercial mortgages will be bought up as well. As this happens, trillions of dollars that have been amassed offshore will be free to come back into the US to buy up and reposition land, farmland, residential and commercial real estate and other tangibles. In a nation in which rule of law existed in more than name, here's what should have happened: 1. The scam known as MERS, the mortgage industry's placeholder of fictitious mortgage notes, would be summarily shut down. 2. All mortgages in all instruments and portfolios, and all derivatives based on mortgages, would be instantly marked-to-market. 3. All losses would be declared immediately, and any institution that was deemed insolvent would be shuttered and its assets auctioned off in an orderly fashion. 4. Regardless of the cost to owners of mortgages, every deed, lien and note would be painstakingly delineated or reconstructed on every mortgage in the U.S., and the deed and note properly filed in each county as per U.S. law. That none of this has happened is proof-positive that the rule of law no longer exists in America. The term is phony, a travesty of a mockery of a sham, nothing but pure propaganda. Anyone claiming otherwise: get the above done. If you can't or won't, then the rule of law is merely a useful illusion of a rapacious, corrupt, extractive, predatory neofeudal Status Quo. The essence of money-laundering is that fraudulent or illegally derived assets and income are recycled into legitimate enterprises. That is the entire Federal Reserve project in a nutshell. Dodgy mortgages, phantom claims and phantom assets, are recycled via Fed purchase and "retired" to its opaque balance sheet. In exchange, the Fed gives cash to the owners of the phantom assets, cash which is fundamentally a claim on the future earnings and productivity of American citizens. Some might argue that the global drug mafia are the largest money-launderers in the world, and this might be correct. But $1.1 trillion is seriously monumental laundering, and now the Fed will be laundering another $480 billion a year in perpetuity, until it has laundered the entire portfolio of phantom mortgages and claims. The rule of law is dead in the U.S. It "cost too much" to the financial sector that rules the State, the Central Bank and thus the nation. Once the Fed has laundered all the phantom assets into cash assets and driven wages down another notch, then the process of transforming a nation of owners into a nation of serfs can be completed. Here's the Fed's policy in plain English: Debt-serfdom is good because it enriches the banks. All hail debt-serfdom, our goal and our god! In case you missed this: The Royal Scam (August 9, 2009):

Once all the assets in the country had been discounted, the insiders then repatriated their money and bought their neighbor's fortunes for pennies on the dollar, finding cheap, hungry, competitive labor, ready to compete with even 3rd world wages. The prudent, hard-working, and savers (the wrong people) were wiped out, and the money was transferred to the speculators and insiders (the right people). Massive capital like land and factories can not be expatriated, but are always worth their USE value and did not fall as much, or even rose afterwards as with falling debt ratios and low wages these working assets became competitive again. It's not so much a collapse as a redistribution, from the middle class and the working to the capital class and the connected. ...And the genius is, they could blame it all on foreigners, incompetent leaders, and careless, debt-happy citizens themselves.

But how is this legal plunder to be identified? Quite simply. See if the law takes from

some persons what belongs to them, and gives it to other persons to whom it does not belong.

See if the law benefits one citizen at the expense of another by doing what the citizen

himself cannot do without committing a crime.

Special offer exclusively for oftwominds.com readers: for two days only, Chartist Friend from Pittsburgh is offering a one-month trial subscription to his daily chart service for an extremely modest $5. Many of you have seen the Chartist Friend from Pittsburgh's insightful charts reprinted in my blog entries. In my view, his charts offer a unique value not found in other's charting systems.

As always, I receive no compensation from this offer.

Resistance, Revolution, Liberation: A Model for Positive Change

(print $25)

Resistance, Revolution, Liberation: A Model for Positive Change

(print $25)

(Kindle eBook $9.95) Read the Introduction (2,600 words) and Chapter One (7,600 words) for free.

We are like passengers on the Titanic ten minutes after its fatal encounter with the iceberg: though our financial system seems unsinkable, its reliance on debt and financialization has already doomed it.

If this recession strikes you as different from previous downturns, you might

be interested in my book

An Unconventional Guide to Investing in Troubled Times (print edition)

or

Kindle ebook format. You can read the ebook on any

computer, smart phone, iPad, etc. Click here for links to Kindle apps and Chapter One.

The solution in one word: Localism.

Of Two Minds Kindle edition: Of Two Minds blog-Kindle

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: gifts/contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Subscribers ($5/mo) and contributors of $50 or more this year will receive a weekly email of exclusive (though not necessarily coherent) musings and amusings. At readers' request, there is also a $10/month option. What subscribers are saying about the Musings (Musings samples here): The "unsubscribe" link is for when you find the usual drivel here insufferable.

All content, HTML coding, format design, design elements and images copyright © 2012 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this essay to your site, or printed a copy for your own use.

Terms of Service:

|

Add oftwominds.com to your reader:

My Big Island Girl

Instrumentals by my friend

|

| Survival+ | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||