|

|

|

||||||||||||

|

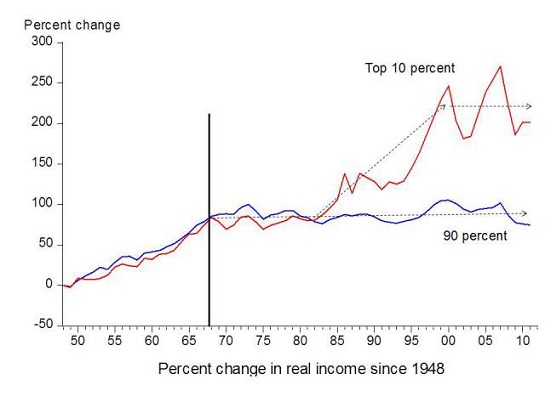

Why We're Stuck with a Bubble Economy (December 9, 2013) Inflating serial asset bubbles is no substitute for rising real incomes. Why are we stuck with an economy that only generates serial credit/asset bubbles that crash with catastrophic consequences? Ths answer is actually fairly straightforward. Let's start with the ideal conditions for an economy that depends on consumer spending. 1. Rising real income, i.e. after adjusting for inflation/currency depreciation, wages/salaries have more purchasing power every year. 2. An expanding pool of new households, i.e. young people who move away from home or graduate from college, get a job and start their own household. New households buy homes, vehicles, furniture, appliances, kitchenware, tools, etc., driving consumption far more than established households. Neither of these conditions apply to today's economy. Income for the bottom 90% has been stagnant for forty years, and has declined 7% in real terms since 2000.

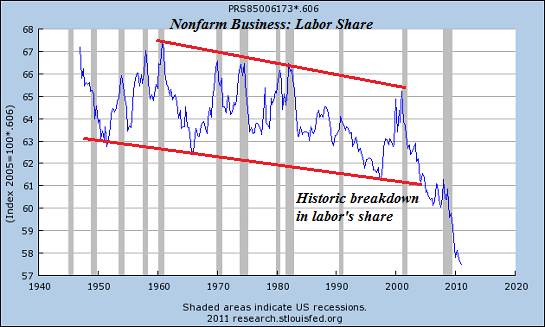

This stagnation is not the "new normal": the new normal is much worse, as labor's share of the national income has fallen off a cliff:

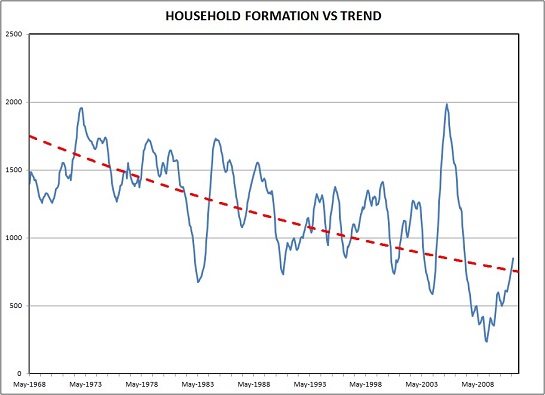

Household formation has also stagnated. That spike circa 2004-07 was caused by the housing bubble, which created new jobs and collateral that could be leveraged into new home purchases.

Since 2008, the Federal Reserve has bought $3.2 trillion in mortgages and Treasury bonds, and the Federal government has borrowed and blown $7 trillion in deficit spending. That $10 trillion in stimulus (not counting $16 trillion in Fed loans to banks and trillions more in other loans/subsidies), household formation has only recovered to the sub-1 million a year level. In an economy of 316 million people, that isn't enough to generate "growth" in a $16 trillion economy. With these organic sources of growth moribund or declining, the Fed and Federal government have resorted to other ways of stimulating more borrowing and spending, the sources of leveraged, high-risk "growth": 1. Lower interest rates so stagnant income can leverage more debt (and thus more spending) 2. Generate asset bubbles in stocks and housing that boost "the wealth effect," i.e. the emotional sense of being wealthier as a result of one's assets rising sharply in value, and the collateral available to support more debt. If a house rises by $100,000 in value in a few short years, the owner has $100,000 more collateral to support new debt. The gargantuan expansion of home equity lines of credit (HELOCs) as the housing bubble expanded was the goal of the status quo, as asset bubbles create collateral that supports new borrowing and spending. Now that interest rates are near-zero and mortgage rates are rising from historic lows, there is no more juice to be squeezed from low rates. As for asset bubbles, they always burst, destroying collateral and rendering borrowers and lenders alike insolvent. Without organic demand from rising real income and new households with good-paying jobs and low levels of debt, the consumer-debt based economy stagnates. This has left the economy dependent on serial asset bubbles that create phantom collateral that can support new debt, albeit temporarily.

Inflating serial asset bubbles is no substitute for rising real incomes and new households that aren't burdened with high levels of debt from student loans.

The Nearly Free University and The Emerging Economy: The Revolution in Higher Education Reconnecting higher education, livelihoods and the economy

With the soaring cost of higher education, has the value a college degree been turned upside down?

College tuition and fees are up 1000% since 1980. Half of all recent college graduates are jobless or underemployed, revealing a deep disconnect between higher education and the job market.

It is no surprise everyone is asking: Where is the return on investment? Is the assumption that higher education returns greater prosperity no longer true? And if this is the case, how does this impact you, your children and grandchildren?

The Nearly Free University and the Emerging Economy clearly describes the

underlying dynamics at work - and, more importantly, lays out a new low-cost model for

higher education: how digital technology is enabling a revolution in higher education

that dramatically lowers costs while expanding the opportunities for students of all ages.

The Nearly Free University and the Emerging Economy provides clarity and

optimism in a period of the greatest change our educational systems and society have seen,

and offers everyone the tools needed to prosper in the Emerging Economy.

Read the Foreword, first section and the Table of Contents.

Kindle edition: list $9.95

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify. We will cover the five core reasons why things are falling apart:  1. Debt and financialization

1. Debt and financialization

2. Crony capitalism 3. Diminishing returns 4. Centralization 5. Technological, financial and demographic changes in our economy Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Once we accept responsibility, we become powerful.

NOTE: gifts/contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Subscribers ($5/mo) and contributors of $50 or more this year will receive a weekly email of exclusive (though not necessarily coherent) musings and amusings. At readers' request, there is also a $10/month option. What subscribers are saying about the Musings (Musings samples here): The "unsubscribe" link is for when you find the usual drivel here insufferable.

All content, HTML coding, format design, design elements and images copyright © 2013 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I am honored if you link to this essay, or print a copy for your own use.

Terms of Service:

|

Add oftwominds.com

|