|

|

|

||||||||||||

|

The Happy Story of Boomers Retiring on Their Generational Wealth Is Wrong

(June 25, 2014)

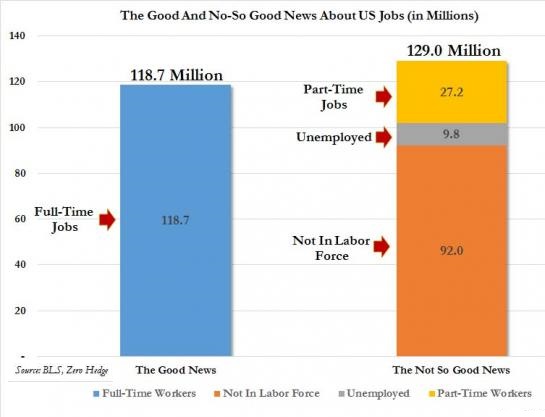

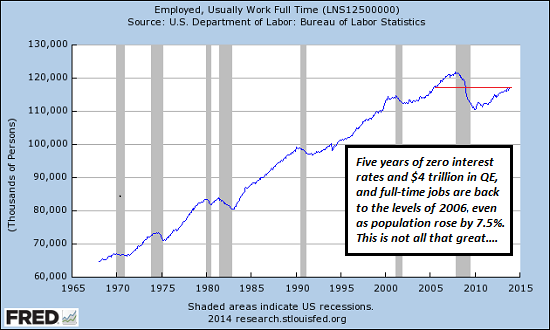

This happy story is wrong on multiple counts. The conventional view of the Baby Boomers' retirement is a happy story: since we're living longer and remaining productive longer, Boomers will not be as much of a burden on Gen-X and Gen-Y as doom-and-gloomers assume. Not only are Boomers staying productive longer, they will draw upon their vast generational wealth as they age, limiting the financial burden on younger generations. This happy story is nicely summarized in this lengthy piece The Fear Factor: Long-held predictions of economic chaos as baby boomers grow old are based on formulas that are just plain wrong. In this view, the only thing needed to prop up Social Security for the rest of the 21st century is a higher tax on high-income earners, in effect moving the limit on earned income exposed to Social Security taxes from about $114,000 to $217,000. This happy story is wrong on multiple counts. Let's start with the most egregious errors: 1. It ignores the End of Work and the decline of full-time jobs 2. It ignores the Elephants in the Room, Medicare and Medicaid 3. It ignores the inconvenient reality that there is nobody to buy the Boomers' overpriced stocks, bonds and homes when they start to unload them Put another way: the happy story ignores the changing nature of work and jobs, the unsustainable cost trajectory of Sickcare (a.k.a. healthcare) and the inability of Gen-X and Gen-Y to buy Boomer assets at bubble valuations. Take these factors into minimal consideration and the claim that 76 million people (out of 316 million) can retire with no negative repercussions falls completely apart. 1. The end of work and changing nature of jobs: I have covered this for many years, most recently in a program with Gordon Long: The New Nature of Work: Jobs, Occupations & Careers (25 minutes, YouTube). Insert end of work in the custom search box on this site and you'll get 10 pages of articles published here on that topic. For example: Global Reality: Surplus of Labor, Scarcity of Paid Work (May 7, 2012) The reality is sobering: 57 million people draw Social Security benefits, tens of millions more draw Medicaid, Section 8 housing credits, etc., and full-time jobs number 118 million:

The Good And The Not- So-Good News About US Jobs In One Chart (Zero Hedge)

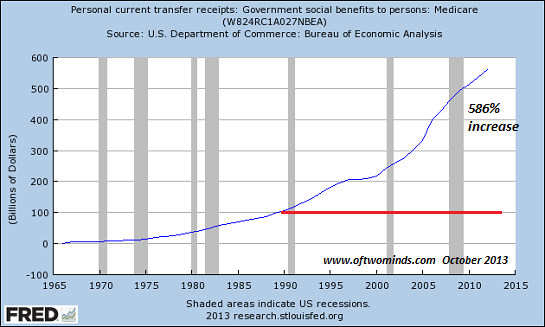

That's a ratio of roughly two workers for every retiree and considerably less than that for workers to the total number of government dependents. As the Baby Boom retires en masse, if full-time jobs don't rise as dramatically as the number of retirees, the system fails. The happy story repeats the usual falsehood that Social Security has a Trust Fund it can draw down. This is a falsehood because the Trust Fund is fiction: when Social Security runs a deficit, the Treasury funds it by selling Treasury bonds, the same way it funds any other deficit spending. If the Treasury can't sell bonds, the phantom nature of the Trust Fund will be revealed. 2. Everyone who looks at numbers rather than fictional claims knows the intractable problem is Medicare and Medicaid. In Sickcare, there are no real limits on cost, and so every attempt to impose cost discipline fails or triggers blowback.

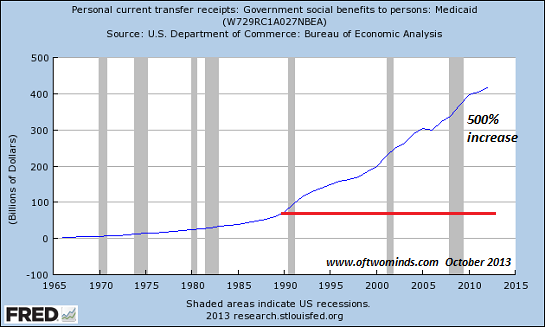

Here is Medicare's twin for under-age-65 care for low-income households, Medicaid:

As I have observed for years, Obamacare and Medicare/Medicaid do not tackle the underlying problems of Sickcare costs in America. If you haven't read these analyses, please have a look: Why "Healthcare Reform" Is Not Reform, Part I (December 28, 2009) Why "Healthcare Reform" Is Not Reform, Part II (December 29, 2009) That Which is Unsustainable Will Go Away: Medicare (May 16, 2012) Obamacare is a Catastrophe That Cannot Be Fixed (December 6, 2013) 3. As I explained in The Generational Short Part 2: Who Will Boomers Sell Their Stocks To?, the Boomers' vast generational wealth will shrivel once they start selling assets en masse. The reality is neither Gen-X nor Gen-Y have the savings, income or desire to buy bubble-level assets from their elders. This reality has been papered over for the past 5 years of super-low interest rates, which have enabled unqualified buyers to buy overpriced assets with modest income. Once the defaults start pouring in (and/or interest rates rise), the reality will become visible: you can't cash in your wealth if there are no buyers. There are numerous other fatal flaws with the happy story that 76 million Boomers can retire on full pensions and live off their home equity and stock portfolios. Here are a few of many: 4. Pension funds based on annual returns of 7.5% will be unable to fund the promised pensions when annual returns decline to negative 5%. As John Hussman has explained, every asset bubble in effect siphons off all the future return: when the bubble finally pops, average annual returns are subpar or negative for years. 5. The ultimate buyer of all Boomer assets is presumed to be the Federal Reserve. I explain why this isn't going to happen in The Fed's Hobson's Choice: End QE and Zero-Interest Rates or Destabilize the Dollar and the Treasury Market (June 24, 2014). 6. It's presumed the Federal government can borrow as many trillions of dollars as it needs to fund retirement and social benefits as far as the eye can see. Please see the article linked above to understand why limits on the Fed's money printing and buying of governemnt bonds imposes limits on Federal borrowing. To quote Jackson Browne: Don't think it won't happen just because it hasn't happened yet. 7. Boomers are staying productive longer and keeping their jobs longer. The reasons for this are many, but one consequence is a dearth of opportunities for Gen-Y job seekers. As full-time employment stagnates or even declines, it's a zero-sum game for the generations: every job a Boomer holds onto is one a Gen-Y applicant can't get. A 12-hour a week low-pay part-time job will not support a wage earner or fund a retiree. 8. A Boomer who bought his home for $50,000 decades ago can live very well on $75,000 a year; it's a different story for Gen-Y. The Boomer has a low mortgage payment (presuming he didn't extract all the equity in the go-go years) and low property taxes in states with Prop-13-type limits. The Boomer who hits 65 has relatively modest medical expenses as Medicare does all the heavy lifting. Low housing and medical expenses leave Boomers with relatively ample discretionary income. The Gen-Y wage earner who takes the same $75,000 a year job is not so fortunate. The Gen-Y wage earner is offered the Boomer's $50,000 home for $550,000, and crushing property taxes to go with the gargantuan mortgage. The Gen-Y wage earner typically still has often-monumental student loan debt to pay off, and much higher healthcare expenses as companies offload rising Sickcare costs onto employees. Higher Social Security and Medicare taxes hit Gen-Y square in the financial solar plexus, while retiring Baby Boomers escape these taxes altogether unless they're still working. The point is an income that offers a Boomer a middle class lifestyle does not offer a corresponding discretionary income to Gen-Yers. The entire pyramid of well-funded retirement is based on a generational continuation of massive borrowing and discretionary spending.

If that doesn't happen for structural reasons, the pyramid of well-funded

retirement collapses under its own weight.

Get a Job, Build a Real Career and Defy a Bewildering Economy (Kindle, $9.95)(print, $20)

Are you like me? Ever since my first summer job decades ago, I've been chasing financial security. Not win-the-lottery, Bill Gates riches (although it would be nice!), but simply a feeling of financial control. I want my financial worries to if not disappear at least be manageable and comprehensible. And like most of you, the way I've moved toward my goal has always hinged not just on having a job but a career. You don't have to be a financial blogger to know that "having a job" and "having a career" do not mean the same thing today as they did when I first started swinging a hammer for a paycheck. Even the basic concept "getting a job" has changed so radically that jobs--getting and keeping them, and the perceived lack of them--is the number one financial topic among friends, family and for that matter, complete strangers. So I sat down and wrote this book: Get a Job, Build a Real Career and Defy a Bewildering Economy. It details everything I've verified about employment and the economy, and lays out an action plan to get you employed. I am proud of this book. It is the culmination of both my practical work experiences and my financial analysis, and it is a useful, practical, and clarifying read. Test drive the first section and see for yourself. Kindle, $9.95 print, $20

"I want to thank you for creating your book Get a Job, Build a Real Career and Defy a

Bewildering Economy. It is rare to find a person with a mind like yours, who can take

a holistic systems view of things without being captured by specific perspectives or

agendas. Your contribution to humanity is much appreciated."

Gordon Long and I discuss The

New Nature of Work: Jobs, Occupations & Careers (25 minutes, YouTube)

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

"You shine a bright and piercing light out into an ever-darkening world."

Or send coins, stamps or quatloos via mail--please request P.O. Box address. Subscribers ($5/mo) and those who have contributed $50 or more annually (or made multiple contributions totalling $50 or more) receive weekly exclusive Musings Reports via email ($50/year is about 96 cents a week).

Each weekly Musings Report offers five features:

At readers' request, there is also a $10/month option. What subscribers are saying about the Musings (Musings samples here): The "unsubscribe" link is for when you find the usual drivel here insufferable.

Dwolla members can subscribe to the Musings Reports with a one-time

$50 payment; please email me if you use

Dwolla, as Dwolla does not provide me with your email.

The Heroes & Heroines of New Media: oftwominds.com contributors and subscribers All content, HTML coding, format design, design elements and images copyright © 2014 Charles Hugh Smith, All global rights reserved in all media, unless otherwise credited or noted. I am honored if you link to this essay, or print a copy for your own use.

Terms of Service:

|

Add oftwominds.com |