|

|

|

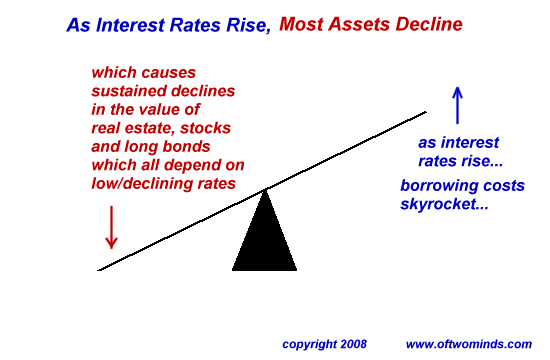

Oversupply and Compression: How the Median House Price Will Fall from $215K to $70K (July 30, 2008) I am constantly amazed (yes, I know I shouldn't be) by how many otherwise intelligent people expect housing to "recover" next year. I shouldn't be surprised, of course, because fantasy and hope are the key traits of all post-bubble busts. Thus we had analyst after analyst in 2001 and 2002 calling "the bottom" in the Nasdaq, even as it fell from 5,000 to 3,000 to 2,000 and then finally to 1,000. In a similar fashion, we now have a nearly universal belief that oil and commodities have "topped out" and the recent decline is a new trend. Happy days are here again, oil is heading back to $75/barrel, hoo-ha! (NOTE: Before you jump on the "oil will just get cheaper and cheaper now" bandwagon, I heartily recommend the new Readers Journal essay by Portugal-based correspondent José de Freitas: Why the Trend in Oil Is Up.) In a similar fashion, we should not be fooled that a brief market reaction is the start of a new trend, i.e. "housing will soon bottom." On the contrary, I predict the median price of a house in the U.S. will fall from $215,000 all the way down to $70,000. According to the National Association of Realtors, the median home price was $215,100 in June 2008. These data sources suggest the median is around $230,00 and the average around $300,000: US: Median Price of Houses Sold including Land Price and US: Average Price of Houses Actually Sold. Whatever number you pick, I predict a 2/3 decline from here, based on these long-term trends and historical patterns: 1. A further 30% decline is required to bring rents and the cost of ownership back into the long-term historical range/ratio. The only reason to buy a house/dwelling which costs far more than renting the equivalent residence is the investment belief that appreciation of the property will exceed (after all the tax benefits are calculated in, etc.) the appreciation of other asset classes. (Note: the ratio varies depending on locale, but in general it is still out of whack from the mean.) In other words, it's an investment decision, not a decision about owning a place to live. If real estate proves to be a poor investment which only depreciates year after year, this belief (currently a near-religious belief of stupendous power in the U.S., based on the past 25 years of debt-fueled speculative frenzy), then housing will decline back to the historical ratio. Now if rents are set to rise 30% above inflation, then the argument could be made that housing will not decline; but with wages in a long-term decline and the economy souring, what rise in income is foreseeable which would fuel a rise in rents? It is more likely that rents will decline in most markets as well, further pressuring the decline in housing values. There are other reasons to believe buying will become ever more unattractive compared to renting: 2. The cost of money will rise for a generation. The two keys to appreciation in real estate are: cheap, easily available money/mortgages, and a highly liquid market in which any property can be quickly bought/sold. Guess what's disappeared and won't be coming back: cheap, easy money and a liquid market. If you are fearful that you can't sell the house you're about to buy, then it's a Capital Trap you will want to avoid. And if money becomes tight again, then a 20% down will be standard once again--and in a recession which has strangled credit, asset values and the economy, how many people will have saved up that much cash? How many will be willing to sink all that cash into a Capital Trap? Relatively few compared to the hordes who "qualified" in the era of liar-loans, no-down, interest-only loans, etc.) 3. Oversupply and vast overbuilding render the market illiquid. With almost 20 million empty dwellings (of which perhaps 4-5 million are true "vacation/second homes") and huge numbers of empty rooms in existing housing, the number of homes for sale will exceed the number of qualified buyers for a long time to come. PIMCO's Bill Gross went on record recently suggesting 1 million homes should be dynamited; good idea, Bill, but that still leaves 15 million empty dwellings. Please don't tell me about population growth: Immigration is already slowing because jobs are drying up, and household size in the U.S. can easily rise, enabling more people to live in the same number of dwellings. The overbuilding was not the result of meeting demand for housing, it was all about meeting the demand for speculative vehicles. Once the speculators are slowly roasted year after year by declining prices, then eventually nobody will be thinking that housing is a "great investment." Once that belief system has been eradicated via everyone who acted on it being destroyed financially, then housing will once again be viewed as shelter rather than a speculative vehicle for investment or "get rich quick" deals. I am continually astonished by the number of people who believe a house which tripled in price and has now fallen a mere 20% is "cheap." As I have written before, there are only two valid reasons for buying a dwelling, and appreciation is not one of them: A. It's cheaper to buy than rent B. You can make money on Day One by buying the dwelling and renting it out at local market rate rents. Both carry this important caveat: you can afford to let your Capital be Trapped in an illiquid market for years. If you might have other uses for the cash, then it would unwise in the extreme to trap it in illiquid real estate. 4. Price-Earnings Compression occurs when risk re-enters a market. This is a well-known element in the stock market: in good times, a company earning a dollar per share will be valued at $25/share--a PE (price-earnings ratio) of 25. That is called PE expansion, and it results from euphoric belief that the economy will forever enable ever higher profits. In recessions, losses reinject risk back into speculative and investment calculations, and PEs contract/compress. Thus the company may still be earning $1/share, but in a real recessionary trough it will be valued at a mere $8/share--a third of its euphoria-"real estate/tech/China/etc. only goes up" valuation. Real estate is not immune to price-earnings compression. If a property keeps declining in value, then the ratio of its net income (from rents) to its value will shrink. Thus in a rising market a property might well be valued at $500,000 based on its rental income, but in a declining market its value may be compressed to $300,000 even if rents haven't dropped a dime. All the risks get priced in--risk that rents might drop, that vacancies may rise, etc.--and buyers turn wary and cautious. 5. Other investments will outshine real estate and money will continue to flow away from housing. If you could earn 10% on your cash, why sink it into a risky illiquid market in housing? Recall that real estate is based on leverage; if you put 20% down to buy a property and it drops 10% in value, if you have to sell you will lose 75% of your initial cash: 50% due to the decline in value and another 25% in transaction costs (realtors fees, closing costs, transaction taxes, etc.) A mere 10% decline in a $500,000 house wipes out half the value of a $100,000 (20%) down payment. Leverage really destroys wealth quickly on the way down. As interest rates rise globally, just parking your money in cash earning a nice return will look better than risking it in depreciating illiquid real estate. Risk cannot be eradicated, it can only be obscured. 6. The inexorable rise in interest rates (i.e. the cost of money) will compress property values by as much as 50%. The reason is simple: if the average buyer can only afford (say) $1,500 a month for a mortgage and property taxes, then the value of the house will rise or fall in direct correlation with mortgage rates, i.e. what the buyer can afford. If rates plummet, as they did in the past decade, then the buyer can afford (say) a $300,000 home for that $1,500/month at 5%. Magically, valuations rise to these levels. Conversely, when rates rise to 10%, the $1,500/month only enables the purchase of a $150,000 home--and so prices decline to what buyers can afford to pay. This is simple supply and demand correlated to the cost of money, which is correlated to its own supply and demand and the level of risk.

Put another way: if you're lending money, and real estate has been declining for years, how much risk premium do you need to bury your bank's capital in a capital trap? As the recognition of risk rises, so do mortgage rates. And as risk rises, long-term fixed-rate mortgages vanish, effectively saddling the buyer with the risks that money will continue rising in cost. That adds another reason for buyers to hold off on sinking their capital and income into an illiquid property. 7. Residences near core jobs, transit and walkable neighborhoods will decline less than housing far from jobs and transit. Those houses will fall to zero value. Thus for median (and average) prices to fall to $70,000, we don't need a market overwhelmingly priced below $100,000--we only need millions of houses valued at near zero. As readers of Jim Kunstler know, the suburban/exurban environment was based entirely on the presumption of endless cheap oil for transportation and commuting. Now that Peak Oil is cutting away at supply even as global growth catapults demand, then that presumption is no longer valid. There may well be oil available for decades, but it will no longer be cheap. Demographically, there are many reasons for people to migrate from exurbs and suburbs to city cores. Cost of commuting is only one; another is health care. As hospitals and urgent care facilities close, aging Baby Boomers who want access to care must move back into cities and large towns. Cities will remain comparatively job rich environments, and so staying close enough to get to work is another reason for migration to urban cores. Towns with a good hospital, clean water and some core of jobs (a college, a hydro-electric plant, farming, etc.) will attract residents who don't want to be stranded in an exurb graced with an abandoned strip mall and little else. The poorer you are, the less money you have for cars, gasoline, etc., and so lower-income people have excellent motivations not to be warehoused in outlying worthless communities which are not served by rail or any public transit and which offer little or no social services (free clinics, libraries, parks, etc.). These are all reasons to expect increasing numbers of residents per household and a reversal of the trend toward one-person households. As I have tirelessly proven in the case of the 2001 dot-bomb exodus from San Francisco and the Bay Area, cities can expand or contract in population by huge margins while their housing stock remains more or less constant. People move back home, people rent out an empty room, and so on. A 100,000 people can move in or out of a city without adding or subtracting a single dwelling. Thus we can foresee housing and rents actually stabilizing in urban zones and towns with ready access to water, nearby cropland/food, jobs, transit, walkable neighborhoods, energy (think Oklahoma, Texas, locales with coal, large hydro-electric dams or huge solar or wind arrays, etc.) and some medical care (even the rationed sort will be welcome if the alternative is none at all). Areas with few to none of these assets will see their housing stock sink to near-zero in value. Supply and demand will eventually rule, regardless of government bailouts, backstops, interventions, etc. There are at least 15 million surplus dwellings in the U.S., an overhang which will not disappear in a few quarters or years. Millions will lose value as they were built in an undesirable locale, while the rest will re-set according to the demand/supply/risk calculations based on the cost of money, demographics, Peak Oil and a number of other trends (scarcity of jobs and healthcare, reduction in government services, etc.) Real estate, bonds and stocks rose during the generation-long trend of ever-lower interest rates from 1982-2005. Now that trend has reversed and cash will outperform all three assets which depend on ever-lower rates and ever-easier money to appreciate in value.

It's a shocking conclusion, I know: a house will return to being shelter, not an

investment vehicle for staggering wealth generation.

Read all five of this month's superb essays if you missed them

Why the Trend in Oil Is Up

Although I'd be lying if I said I am certain of which direction the oil price is going, my gut feeling is telling me that it's going up as a general trend, despite brief respites. A few points have not been sufficiently made, and I think Rainer H.'s piece exhibits some of the problems those points would address. NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Alberto R. ($20), for your second generous donation and your

ongoing contributions of ideas and essays to this site.

I am greatly honored by your support and readership.

For more on this subject and a wide array of other topics, please visit my weblog. All content, HTML coding, format design, design elements and images copyright © 2008 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||