|

|

|

||||||||

|

Housing Recovery: Sell Now Or Your Capital Will Be Trapped (July 27, 2009) As news reports of housing's "recovery" fill the mainstream media, the devastating effects of rising interest rates are never mentioned: every house with equity becomes a capital trap. Here's the "housing is recovering" story graphically depicted:

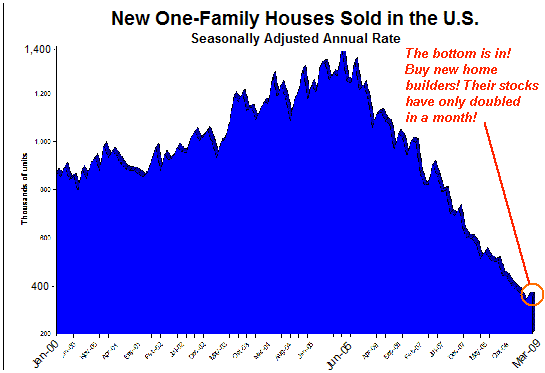

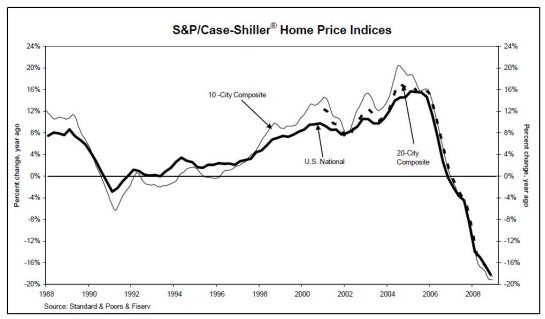

Anecdotally, breathless stories of the return of multiple bids are filtering into a Mainstream Media anxious to report "proof" of a "recovery in housing." Just for context, let's take a quick look at the Case-Shiller Index:

This translates into a 50% decline in bubblicious areas of the nation: Dr. Housing Bubble: Calif. Housing drops 50% from peak. As noted in the above article, fully 58% of all California home sales are foreclosure resales. In other words, "the bottom is in, now is the time to snap up bargains." Not so fast. Let's focus on the key feature of buying a house as opposed to, say, a TV: very, very few people buy a house with cash. The vast majority of real estate purchases are financed with mortgages--debt. And credit is lent at a rate of interest. As a result, the relationship between interest rates and the value of real estate is a see-saw. Buyers can only afford X per month in mortgage payments. If interest rates double, they can only afford to buy a house at a much lower valuation. Here are graphic depictions of the relationship:

In other words, when interest rates double, house prices will drop in half, regardless of any other conditions. The newly risk-averse lenders will only originate mortgages which amount to roughly a third of the borrower/buyer's monthly income, and so this is the metric which controls the price of housing. The price can be set to whatever level the seller desires, but it will eventually settle to the price the buyers can actually afford. So why am I suggesting interest rates could double from 4.5% to 9% in the near future? Please consider this chart of total U.S. debt, 1929-2008:

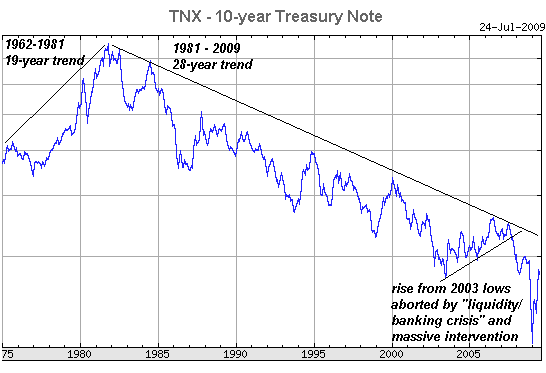

We've all read about the $2 trillion Federal deficit for this fiscal year; but let's not forget that corporations, local governments and agencies and real estate buyers also want to borrow money. Bottom line: the demand for surplus capital far exceeds the supply of surplus capital globally. Every other government on the planet (yes, even the Chinese government) is also anxious to borrow huge sums of money from someone to fund their exploding deficit spending. Courtesy of frequent contributor U. Doran, here is a report from Sprott Asset Management on how dependent the U.S. is on non-U.S. capital: The Solution...Is the Problem. The excellent John Mauldin recently issued a report on how governments want to borrow $5 trillion but there is no more than $3 trillion available to borrow: Buddy, Can You Spare $5 Trillion? This is the classic "unstoppable force hitting the immovable object"--oh, but wait: interest rates are set by the market and are thus quite movable. Consider this chart of the 10-year U.S. Treasury bill yield:

Note that the rise from 2003 lows was aborted by a global "flight to safety" and a massive intervention in the capital markets by the Federal Reserve and U.S. Treasury which caused interest rates to plummet to unprecedented lows. But longer term, this cycle of declining interest rates is already extremely long in tooth at 28 years and counting. the average interest rates cycle has historically measured about 20 years in length, suggesting this cycle is due for a turn and the start of a 20+-year cycle of rising interest rates:

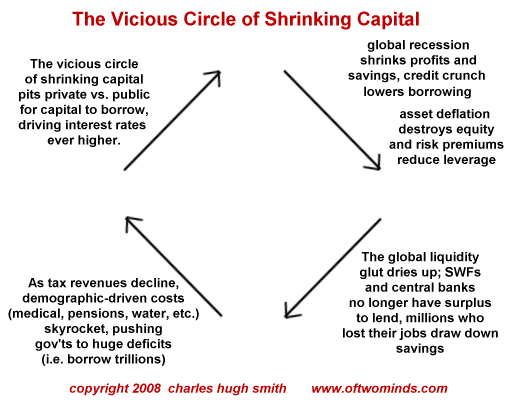

But wait: it gets worse. Surplus money looking for a home is drying up even as the demand for surplus capital skyrockets. This vicious circle can be displayed thusly:

The net result is interest rates will have to rise--and soon. While it is impossible to predict exact dates, simple laws of supply and demand dictate that rates will soon rise and will rise steeply as the shortfall between what governments want to borrow and what's available to borrow becomes visible (not to mention private demand for capital). As interest rates rise, then the Capital Trap shuts on all equity locked in real estate. I covered this subject last year: The Housing Capital Trap Snaps Shut (May 28, 2008) The mechanism can best be illustrated with an example. Let's say a homeowner who bought long ago has a $100,000 mortgage on a home which was once worth $450,00 at the bubble peak. Now the property has sunk to a value of $250,000. The owner still has $150,000 in equity: quite a substantial sum. But if interest rates double, then the house would have to fall roughly in half to be affordable to buyers. Equity would shrink to a mere $25,000. Or alternatively, if the owner insisted the "true value" was still $250,000 based on other metrics, then the capital is trapped as the house cannot be sold in the marketplace. Thus it can be argued that to the degree a house is an investment and the basis of household wealth, the owner would be wise to sell the house now in this brief "housing recovery" while rates are still low, pocket the $150,000 equity (For simplicity's sake, I leave out commissions, property taxes, etc.) and rent an equivalent home. As interest rates rise, that equity will begin earning a decent return in a simple savings account. I know this concept--that savings will accrue more wealth than equity in a house--is so alien as to be absurd. We have been conditioned by the past three decades of explosive rises in real estate valuations and declining interest rates to believe "real estate always rises" and cash is essentially trash. But the 28-year long orgy of ever-lower rates is ending, and may end abruptly, and soon, as the U.S. Treasury seeks not just to borrow trillions more but also roll over expiring bonds. The key concept here is that a house is only worth what someone can afford to pay for it. Thus we must be wary of divining "the bottom" based on metrics which don't take rising interest rates into account. Why can't the Fed just print the $2 trillion the government wants to borrow? Wouldn't that solve the problem? In theory, perhaps, but in practice, when the Fed did exactly that, announcing it was printing $300 billion to buy Treasuries, the bond market reacted violently by pushing rates up dramatically. Printing trillons of dollars is seen as inflationary by the bond market, and if inflation is being ramped up to 4%, why buy a bond that pays 2%? To keep buying bonds which are guaranteed to lose money is simply unwise. The net result is the Fed cannot just print $3 trillion (don't forget all the bonds which have to be rolled over) and buy Treasuries--the bond market would instantly demand much higher rates to compensate for the additional risks of inflation. Real estate industry cheerleaders counter by saying housing "always rises in inflationary eras." By that they refer to the 70s, when real estate shot up alongside rising inflation. But what they forget is that housing was rising from extreme levels of affordability, and that the Baby Boom was entering its prime homebuying decade in the 70s. Now we have 18.7 million vacant homes, a high level of unaffordability and rising interest rates.

There are many psychological reasons to own property: the sense of security, that you can

do what you want with the home and yard, and so on. These are very real and valuable. But

as an investment, rising interest rates will trap whatever capital is sunk in the house.

To the degree a house is not just shelter and psychological security but an investment,

that matters.

"Your book is truly a revolutionary act." Kenneth R.

HUGE GIANT BIG FAT DISCLAIMER: Nothing on this site should be construed as investment advice or guidance. It is not intended as investment advice or guidance, nor is it offered as such. It is solely the opinion of the writer, who is NOT an investment counselor/professional. All the content of this website is solely an expression of his personal interests and is posted as free-of-charge opinion and commentary. If you seek investment advice, consult a registered, qualified investment counselor (As with any other professional service, confirm their track record and referrals).

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Your readership is greatly appreciated with or without a donation.

For more on this subject and a wide array of other topics, please visit

my weblog.

All content, HTML coding, format design, design elements and images copyright © 2009 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

|

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||