|

|

|

|||||||||||||

|

Financialization and Crony Capitalism Have Gutted the Middle Class (July 13, 2012) The neofeudal colonization of the "home market" has transformed the middle class into debt serfs.

According to the conventional account, the Great American Middle Class has been eroded by rising energy costs, globalization, and the declining purchasing power of the U.S. dollar in the four decades since 1973. While these trends have certainly undermined middle-class wealth and income, there are five other less politically acceptable dynamics at work:

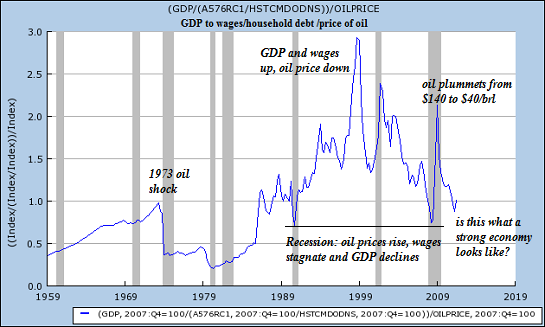

Higher Energy Costs = Lower GDP, Lower IncomesLet’s start with the conventional forces of higher energy costs. The abundance or scarcity of energy is only one factor in its price. As the cost of extraction, transport, refining, and taxes rise, so does the final price. EROEI (energy returned on energy invested) helps illuminate this point. In the good old days, one barrel of oil invested might yield 100 barrels of oil extracted and refined for delivery. Now it takes one barrel of oil to extract and refine 5 barrels of oil, or perhaps as little as 3 barrels of unconventional oil. It doesn’t matter how abundant oil might be; it’s the cost that impacts GDP and income. Here we see that GDP in relation to the price of gasoline hit bottom in the wake of the 1979 oil shock. GDP soared in the late 1990s when oil plummeted to $15/barrel. It spiked lower when oil hit $140/barrel in 2008, and popped back up when oil dropped (briefly) to $40/barrel. (FRED charts courtesy of B.C.)

Here we see the cost of oil’s impact on wages:

As oil costs rise, wages and GDP decline. If we read between the lines, this chart reflects an economy that has become less dependent on oil for its GDP growth than it was in the 1970s, but oil’s influence on growth and income is clearly still fundamental. This fifty-year history of oil, GDP, wages, and household debt reveals that GDP and wages only rose smartly in brief eras of depressed oil prices. Households compensated for the stagnation of their wages by borrowing. The Middle-Class Work-Around: Substituting Debt for IncomeThe key idea here is that real income can only rise if the productivity of labor and capital investment increases. If productivity of labor and capital is flat, any increase in income is a mirage; i.e., a rise in nominal income that is not an actual increase in purchasing power. Here we see that labor productivity has risen steadily, more than doubling since 1970.

Wages also rose—but household debt rose at a much higher rate than wages.

I have been asked by readers to only use “adjusted” or “real” measures of GDP, wages, etc., but sources rarely compare apples to apples, and the high probability that “official” inflation has been understated leaves even “adjusted” data suspect. In nominal terms, the ratio of these two lines is what’s important. From the point in time when they began diverging (1983), wages tripled but household debt rose sevenfold. (According to the Bureau of Labor Statistics’ (BLS) inflation calculator, $1 in 1983 is equal to $2.31 in 2012 dollars.) If we dead-reckon that “real” inflation is probably more like $1 in 1983 = $3 in 2012, this still suggests that wages doubled in the past 30 years. The increase (however you calculate it) flowed entirely to the top 10% of households.

That the bottom 90% of wage earners lost ground has been well established. This summary from the New York Times encapsulates the stagnation:

The decline in earnings isn’t just income inequality at work. Labor’s share of the national income has plummeted to historic lows.

Clearly, the middle class (however you choose to define it, it can’t be the top 10%) compensated for stagnating income with a “work-around” that was heavily incentivized by tax deductions of interest and declining interest rates: borrowing money. Meanwhile, corporate profits have risen sevenfold since the early 1980s (as did household debt—an interesting coincidence).

Perhaps a more accurate measure of corporate profits is to view them as a share of GDP:

Corporate profits as a share of GDP zoomed to historically unprecedented levels in the credit-bubble era following the brief 2001 post-dot-com recession. What accounts for this unprecedented rise in corporate profits and equally unprecedented decline in labor’s share of the national income? The forces at work can be summarized in one word: financialization. The Perverse Incentives and Feedback of FinancializationFinancialization is the incentivization of debt, leverage, speculation, and regulatory capture; i.e., “deregulation,” that enables graft, fraud, and collusion as the “business model” for low-risk profits. From the long view, modern-day corporate/State capitalism (Neoliberal Capitalism) ran aground in the 1970s on two shoals: the rise in energy costs and the exhaustion of consumerist demand driven by rising wages. After stumbling badly through the 1970s (adjusted for inflation, the S&P 500 stock index lost 67% of its value in that high-inflation decade), Neoliberal Capitalism developed a financialization model for growing profits. As the cost of borrowing fell, a stagnant income could leverage (i.e., serve as collateral) for larger amounts of debt. This new debt-driven demand boosted the value of assets such as houses and stocks, which then provided new collateral for even more debt. Restrictions on leverage and speculation were loosened or gutted via State-mandated financial deregulation. This created a self-reinforcing “virtuous cycle” of ever-rising debt, leverage, speculation, asset valuations, and financially derived profits. In the final stages of this debt-based “prosperity,” auto manufacturers were booking most of their profits on auto loans; the actual manufacture of vehicles was merely a step in the origination of new debt. This increasing reliance on debt for “growth” and “prosperity” aligned perfectly with the interests of the stagnating middle class, which had turned to debt as a substitute for income to support their lifestyle. Thus in the early stages of financialization, the interests of the financial sector and the middle class borrowers aligned, as were those of the Central State, which saw tax revenues climb as income and profits rose. Ever-expanding debt rose faster than income, however, so leverage had to constantly increase if debt were to continue rising. This is why by the end of the financialization cycle in 2006, the housing bubble was being driven by “zero down payment” mortgages ($0 down leverages a $500,000 loan) and “no-document” mortgages (“liar loans”), where phantom income served as collateral for phantom assets. The “virtuous cycle” ends once leverage cannot be extended any further. As overall debt expansion ceases, the asset bubbles created by debt-dependent demand implode, and the cycle reverses into deleveraging: as assets decline in value, assets must be sold off and debt either paid down or repudiated/written off. The assets were phantom, but the debts left behind were real, and the losses were real, too. Real income must be devoted to paying down debt that was based on phantom assets. The middle class gorged on debt for 30 years as a “work-around” for stagnant income, and its wealth rose as its investments in housing and stocks reached bubble heights. Now that the credit-based expansion of asset valuations has reversed, middle class wealth has been gutted even as its income is largely devoted to servicing underwater mortgages, high-interest student loans, and other household debt.

The interests of the middle class have now diverged from the vested interests of the Central State and the financial sector, which used its expanding profits to capture regulators and buy political protection of its financialization rackets. Even now, four years after the implosion of the financialization model, we are treated to headlines such as “Rigged Rates, Rigged Markets.” The Neofeudal Colonization of Home MarketsThe use of credit to garner outsized profits and political power is well-established in Neoliberal Capitalism. In what we might call the Neoliberal Colonial Model (NCM) of financialization, credit-poor developing world economies are suddenly offered unlimited credit at very low or even negative interest rates. It is “an offer that’s too good to refuse” and the resultant explosion of private credit feeds what appears to be a “virtuous cycle” of rampant consumption and rapidly rising assets such as equities, land and housing. Essential to the appeal of this colonialist model is the broad-based access to credit: everyone and his sister can suddenly afford to speculate in housing, stocks, commodities, etc., and to live a consumption-based lifestyle that was once the exclusive preserve of the upper class and State Elites (in developing nations, this is often the same group of people). In the 19th century colonialist model, the immensely profitable consumables being marketed by global cartels were sugar (rum), tea, coffee, and tobacco—all highly addictive, and all complementary: tea goes with sugar, and so on. (For more, please refer to Sidney Mintz’s landmark study, Sweetness and Power.) In the Neoliberal Colonial Model , the addictive substance is credit and the speculative consumerist fever it fosters. In the financialization model, the opportunities to exploit “home markets" were even better than those found abroad, for the simple reason that the U.S. government itself stood ready to guarantee there would be no messy expropriations of capital or repudiation of debt by local authorities who decided to throw off the yokes of credit colonization. In the U.S. “home market,” the government guaranteed lenders would not lose money, even when they loaned to marginal borrowers who could never qualify for a mortgage under any prudent risk management system. This was the ultimate purpose of Freddie Mac, Fannie Mae, and now the FHA, which is currently guaranteeing the next wave of mortgages that are entering default. In my analysis, the Status Quo of “private profits, public losses” and the incentivization of gargantuan household debt amounts to a modern financialized version of feudalism, in which the middle class now toils as debt-serfs. Their debt cannot be repudiated (see student loans), their stagnating disposable income is largely devoted to debt service, and their assets have evaporated as the phantom wealth created by serial credit bubbles has largely vanished. Subsidizing a Parasitic Central State and Crony Capitalist CartelsIn broad brush, financialization enabled the explosive rise of politically dominant cartels (crony capitalism) that reap profits from graft, legalized fraud, embezzlement, collusion, price-fixing, misrepresentation of risk, shadow systems of governance and the use of phantom assets as collateral. This systemic allocation of resources and the national income to serve their interests also serves the interests of the protected fiefdoms of the State that enable and protect the parasitic sectors of the economy. The productive, efficient private sectors of the economy are in effect subsidizing the most inefficient, unproductive parts of the economy. Productivity has been siphoned off to financialized corporate profits, politically powerful cartels, and bloated State fiefdoms. The current attempts to “restart growth” via the same old financialization tricks of more debt, more leverage and more speculative excess backstopped by a captured Central State are failing. Neofeudal financialization and unproductive State/private vested interests have bled the middle class dry. In Part II: The Middle Class Survival Guide, we look at what we can do to avoid serfdom and collaborating in an unjust, exploitative, and ultimately doomed system. We are not powerless simply because we are not individually wealthy and politically powerful. The Status Quo depends on our passivity, complicity, and collaboration. Just as each vote we cast in an election supports or resists the Status Quo, every dollar we spend is a “vote,” too. Every dollar we don’t send to a cartel or quasi-monopoly is a dollar we can spend locally or invest in our own life. Click here to access Part II of this report (free executive summary, enrollment required for full access)

This essay was originally published on peakprosperity.com, where I am a contributing writer.

Resistance, Revolution, Liberation: A Model for Positive Change

(print $25)

Resistance, Revolution, Liberation: A Model for Positive Change

(print $25)

(Kindle eBook $9.95) Read the Introduction (2,600 words) and Chapter One (7,600 words) for free.

We are like passengers on the Titanic ten minutes after its fatal encounter with the iceberg: though our financial system seems unsinkable, its reliance on debt and financialization has already doomed it.

If this recession strikes you as different from previous downturns, you might

be interested in my book

An Unconventional Guide to Investing in Troubled Times (print edition)

or

Kindle ebook format. You can read the ebook on any

computer, smart phone, iPad, etc. Click here for links to Kindle apps and Chapter One.

The solution in one word: Localism.

Of Two Minds Kindle edition: Of Two Minds blog-Kindle

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: gifts/contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Subscribers ($5/mo) and contributors of $50 or more this year will receive a weekly email of exclusive (though not necessarily coherent) musings and amusings. At readers' request, there is also a $10/month option. The "unsubscribe" link is for when you find the usual drivel here insufferable.

All content, HTML coding, format design, design elements and images copyright © 2012 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this essay to your site, or printed a copy for your own use.

Terms of Service:

|

Add oftwominds.com to your reader:

My Big Island Girl

Instrumentals by my friend

|

| Survival+ | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||