(October 1, 2008)

The coming Depression is baked in and cannot be repealed by a vote of the Senate or

the bailout of distressed/insolvent banks. Along with the Depression will come

drastically lower prices for all assets, which will reflect drastically lower

sales and profits.

The main reason why the Depression is baked in is the global

credit bubble is finally bursting. When credit dries up and becomes more expensive,

there is less money being borrowed and spent. That is straightforward.

But as frequent contributor

Harun I. explains, the credit bubble also fueled an accelerated flow of money

through the system, i.e. velocity of money. This has been readily visible

in the number of dollars which must be borrowed to create $1 of additional GDP.

As the credit bubble expanded, it required more and more dollars to be loaned/borrowed

to eke out a mere $1 of "growth" (GDP). In other words, more and more debt had to be

created and taken on to maintain even anemic growth.

Now the credit bubble has burst, this growth of debt has reversed as lenders "deleverage"

i.e. sell assets and pay down debt.

Here is Harun's commentary:

This plan will be an abject failure simply because it will not create velocity of

money. Jobs will not be created, consumers will not have more income to spend and

will not qualify to borrow.

Trillions in MBS and CDS are symptoms of a greater problem. These instruments

weren't created just because of greed, they were created because they were needed

to fuel an economic ideology (or perhaps reality) that needs exponentially greater

inputs to grow.

Mish analogized this with the "Red Queen's Race". Once the curve

is close to or at vertical it represents infinity, i.e., inputs of infinite

amounts of money or debt expansion (credit money) is needed infinitely just

to remain in place. Because it is an exponential progression is why every graph

we see today dealing with debt growth has "hockey sticked". There is simply no

way to save this type of system.

Everyone, including Paulson and Bernanke got caught thinking linearly and therefore

are now shocked at the rapidity of the onrushing collapse. I have been arm waving

and shouting about this for some time and will continue to do so until people

"get it".

The link below is a primer on exponential growth. The chart is a basic example of

exponential progression. If we think in terms of debt growth, the Y axis represent

quantity and the X axis is time. As the curve progresses exponential increases

in debt are needed over an exponentially condensing time period until the time frame

is always now and inputs required are infinite. Obviously this leads to collapse

from exhaustion.

The link below is a primer on exponential growth. The chart is a basic example of

exponential progression. If we think in terms of debt growth, the Y axis represent

quantity and the X axis is time. As the curve progresses exponential increases

in debt are needed over an exponentially condensing time period until the time frame

is always now and inputs required are infinite. Obviously this leads to collapse

from exhaustion.

Understanding Exponential Growth

Economically, it should now be clearly understood that when an economy's physical

output is in serious decline or non-existent and the economy becomes almost

totally dependent on the expansion of monetary aggregate for "growth", a systemic

meltdown is inevitable.

Here is an appropriate analogy from the Daily Reckoning:

We dont know what Professor Chris Martenson is a professor of. But

he has done the world a favor with his description of what happens

when things grow exponentially, rather than arithmetically.

Imagine you could make a football stadium watertight, he writes.

Then, imagine that you put a magic drop of water in the center...a

drop of water that doubles every minute...so that after six minutes

or so, youd have about enough water to fill a thimble. Now how long

would it take before the stadium filled, he asks?

Were not going to leave you in suspense. For the first 45 minutes,

you can walk around the stadium and barely get your feet wet. But in

the next 4 minutes the stadium fills and you drown.

Thank you, Harun. Next, corrspondent Peter F. offers an example of how

the bailout (TARP) would work in Crony Capitalism , i.e. the system

the bailout was designed to benefit:

Peter F.

I've given a great deal of thought as to how the Troubled Asset Relief Program (TARP), a/k/a the "bank bailout" will achieve the goals of saving the banking system and "getting the economy moving again." I think I've figured it out.

I've read the House Bill and could find nothing that would prohibit the occurence of my scenario. Maybe you can find where I'm wrong.

1. We start with TARP, which issues $100 in new, full faith and credit, U.S. Treasury bonds. The agency now has $100 cash.

2. ABC Bank has on its books a portfolio of troubled debt with a face amount of $100. The problem for ABC Bank is that it will only be able to collect $70 from the borrowers. The loss to ABC Bank will be the difference, $30.

3. The bank sells the troubled debt to TARP for $100 and the loss disappears.

Instead of holding $100 in problem loans, the bank now has $100 cash.

4. TARP doesn't want to hold the problem loans so it sells the loans to a new vulture/scavenger fund which pays $50 for the troubled debt. TARP now has $50 in cash and $100 in bonds outstanding.

5. Where did the scavenger fund get the $50 to buy the loans from the government? Well who now has $100 in cash? ABC Bank. The scavenger fund borrowed the $50 from ABC Bank.

6. ABC Bank now has $50 left over from the sale to TARP. What does ABC Bank

do with that money? It buys $50 in Treasury bonds.

Look at Step 4. TARP now has $50 in cash. We then restart the cycle at Step 2 only

with half the amount of money involved in the transactions. After we repeat the

cycle enough times until we reach the limit (no assets held by TARP) here is what

we get:

Banks

Treasury Bonds: $100

Scavenger Loans: $100

Loss Avoided on $200 in Loans: $60

Scavenger Funds

Junk Loans: $200

Bank Loans: $100

Loss Reserve: - 60

Net Loans: $140

Equity: $40

Profit to Scavenger Funds: $40

Isn't high finance great? On $200 in bad loans the private sector profited $100

($60 in bank loss avoidance, $40 in scavenger fund profits).

But only the Federal Reserve can create money out of thin air. Who took the $100

loss that allowed the banks and scavenger funds to profit by $100? Hint: here's

the balance sheet for TARP:

Assets: $0

Bonds Outstanding $100

Now look into the mirror.

Thank you, Peter. I have to confess this stretches beyond my comprehension

of accounting but certainly seems to make sense. The working /retired accountants

among you may be able to provide additional insights/critiques.

Nonetheless, this example illustrates how the bailout will do virtually nothing

but enrich the cronies who will be buying the distressed assets at fire-sale prices

from the Treasury, and how the taxpayer will be stuck with either worthless assets

(i.e. mortgages so worthless even the cronies don't want them) or worthless debt.

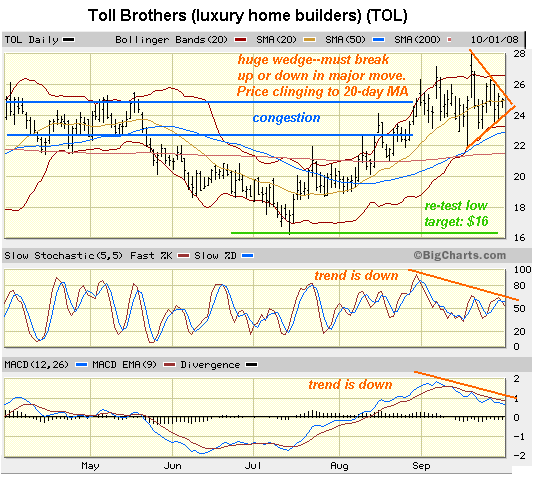

Next up: a sample chart of just one credit-dependent industry among many:

home builders. I have featured Toll Brothers here last month, and disclosed that

I own puts on TOL (i.e. a bet the stock will decline in the near future).

Please read the HUGE GIANT BIG FAT DISCLAIMER below: this is not investment advice

but the opinions of one amateur chart-gazer.

Auto sales--another credit-dependent business--fell off a cliff in September.

Why would anyone think sales of luxury homes (Toll's product) would hold up better

than vehicles? What will the cancellation rate be in September for luxury homes

which buyers signed up to purchase earlier in summer? 60%? Or perhaps 90%?

How many luxury new homes will be sold next year? How many new homes will Toll

build when inventory is still climbing and credit, income and household assets

are all disappearing like summer rain in the Mojave Desert?

But TOL has jumped from $16 to $26 recently on the fervent if fantasy-based dream

that some sort of reinflation of the housing bubble is just around the corner.

The chart reveals a huge wedge which will have to resolved up or down in a

najor way very shortly. Even as indicators like MACD and stochastics are

in visible downtrends, market Bulls have kept TOL elevated at prices which scream

"housing recovery starts in January 2009 and then booms!"

Given the dire straits of the U.S. economy, credit markets and the housing glut/

crash, it seems more likely that TOL will declare bankruptcy in 2009 than announce

a major strengthening of sales (which aren't cancelled a few weeks later). If the economic

and credit data actually start intruding on the fantasy so near and dear to the

hearts of the Bulls who have bid TOL up to "economic expansion/housing is healthy"

levels, then the wedge may be resolved with a rapid drop back to the $16 level, and then

on down to either $2 or zero.

This is not the only company which has continued to float on a fantasy-cloud of

hope and dreams for a huge recovery in the economy a few months down the road.

Meanwhile

all credible data (such as new car and truck sales and the ISM report) suggests

the economy is

sliding down an increasingly slippery slope, gaining speed every day. Why would anyone want to own a stock which

has no earnings and no hope of earnings, plus faces a good chance of insolvency

in the coming Depression? I really don't know.

Two articles recommended by frequent contributor U. Doran:

Roubini: Risk as high as ever of global meltdown

Doug Nolan's Credit Bubble Watch

We have a multitude of great Reader Comments:

Brian B.

I think your site has many great articles. My question is were do we go from here? What happens next week or month when there is another problem that surfaces; Do they ask for anther bailout and what will prevent panic in the market? I think that the panic may be starting soon. What happens next?

My response:

Nobody knows, as history only echoes, it doesn't repeat exactly. Many expect every industry and business in America to line up for their own bailout, which would cause the bond market to crash as there isn't enough cash on God's green Earth to bail out every bank, corporation, realtor, business etc. We see the auto industry already got a $25B "loan" (if unpaid, becomes a gift).

I see a depression baked in for all the reasons I have covered for the past 3 years.

Borrowing money and throwing it down ratholes will do nothing but make the problem

worse. That is my opinion but of course I could be completely wrong.

If we let the insolvent go bankrupt the problems would be cleared up much quicker

than keeping a zombie economy going.

David V.

If the American Taxpayers, are "Investing" in $700,billion in troubled assets,

if they go down the crapper, do all Americans get to write it off aginst their

personal Taxes....? Using GAP when do you take the loss...? Is it on your schedule D.....?

Kevin K.

Like you I was laughing out loud this weekend when I was reading in Barrons and the WSJ that the government will make money on the bail out.

To remind you I originated and sold CMBS loans for the past 10 years and I have not read a single mention of the bond tranches (see the link below for more info).

wikipedia-Tranche

When I try and put bond structure in to terms that regular people can understand I tell them to pretend that a pool of bonds has just three $500K homes in it with the first loss bond buyers investing 10% in equity, the B Bond buyers holding 10% second TDs and the AAA bond buyers holding the 80% 1st TDs. When a home goes through foreclosure most people understand that the equity investor and the 2nd TD holder never see another penny even if the real estate market recovers and the home triples in value.

In my example with a 7% loan coupon the three $500K homes equity guys will get about a 20% return, the second TD guys will get about a 12% return and the AAA/1st TD guys will get about a 5% return. in the past few years the banks held on to a lot of the high risk first loss bond tranches since they got to book huge returns and get huge bonuses (and with Lehman Brothers go under)...

The problem is (using my example above) if one of the three homes stops making payments the first loss guys get no interest payments, the second guys get no payments and the AAA/1st guys will be getting payments lower than a CD. If the first home is foreclosed on and sold for $400K (a 20% drop in value) the first loss bond guys have no claim to any more payments and will have no claim for even a penny at maturity, and the B piece bond guys will also never see another payment and not get a penny at maturity. If the other two loans keep paying as agreed to maturity the AAA 1st TD guys will get a sub 5% cash flow and still take a big loss at maturity.

Most people understand that a $100K second TD behind a $500K first TD on a crappy home in a crappy part of Oakland worth $400K has no value and probably never will have any value since only a fool would keep the first TD holder current (pouring good money after bad) to avoid foreclosure.

You have got to hand it to the big Wall Street bankers who have been buying (aka making legal campaign contributions) to politicians on both sides of the aisle since it looks like they will be able to dump at least some of these worthless bonds that will probably never have any value on the taxpayers...

Michael Goodfellow

From the WSJ:

China, Saudi Arabia and other big foreign holders are unlikely to take antidollar

measures precisely because they own so much U.S. debt. To the extent the dollar

declines, so does the value of those nations' holdings. Mr. Summers calls this

situation "the financial balance of terror."

But it is naive to assume that this so-called balance will protect U.S. interests

indefinitely. Senior Chinese economists have voiced growing dismay about the

outlook for the dollar, and the introduction of an additional $700 billion in

debt might drive the currency's value down further, at least in the short term.

"I think foreigners are being taken for a ride by the U.S. government," says Andy

Xie, an independent economist in Shanghai.

There's a movie called "Lock, Stock and Two Smoking Barrels". It's directed by Guy Ritchie, the same guy who did "Snatch", which I liked a lot. This is similar, but not quite as strong.

Anyway, early in the movie, one of the guys sits down at a poker table, with a big stake collected by his friends. He's the best, but the game turns out to be totally crooked. He loses all the money. Then, when he's about to get up and leave, crushed, the boss of the game tells him to stay put. And he makes him play another round, with money he doesn't have, so that he ends up not just broke, but owing the boss twice what he came in with.

China must look at this bailout the same way. They can't win, and now they can't get out of the game.

They must wonder what happens if they pony up the money and lose it all because we crash anyway. Let's hope they don't snap and decide to let it all burn now.

Freeacre

Now here's a plan worth voting for!

from Cynthia McKinney's site, Green Party candidate for President:

A Gift for a Generation: A U.S. Financial System of Our Own

Those ten points, to be taken in conjunction with the Power to the People

Committee's platform available on the campaign website at

votetruth08.com are as follows...

Dale R.

Hi Charles. Enjoy reading your blog.

I have read in the news, that voters dont understand how banks, and wall street work with the economy. This is probably true. But we do know when we are being, fleeced and blackmailed.

People who work 30 to 50 hours a week, have always been in a recession. A recession will not be new to us. Every time we get a few bucks ahead, after tax, the high cost of living will take them.

TWA

You were one of the first to see it.

Now ask the question of who owns the Federal Reserve?

Analyze the Bernanke papers to show how this just in time save was predetermined from years of planning.

How does Paulsons $500,000,000 from the GS days, the rescue of JP Morgan (from BS CDS exposure) (everyone thinks it was a Bear Sterns rescue) and the current power grab, tie together with who owns the Fed.?

Thanks for your incredible insight over the years.

Harun I.

The constant bleating about $1.2 trillion lost is completely disingenuous. The MSM is engaged in an aggressive propaganda campaign based on lies of omission.

The irrefutable fact is that if you owned the Dow and cashed it in today you would still be able to purchase the same amount of gold as in July. If you liquidated your SP 500 holdings they purchased no more Unleaded Gas than could have been purchased in 1989. If you sold your bonds today they would purchase less than they did on 9/11/08 despite the dramatic price rise yesterday. NOMINAL VALUE MEANS NOTHING. Everything, even money, is a commodity and its value is relative to the quantity and quality of another commodity for which it can be exchanged.

John D.F.

Bailout Propaganda:

First - I have to brag - my 12 year old daughter, Justina, is gifted, and is in a special public school in our school system (Duval County, Florida) for similar children.

Friday past she came home and had a bunch of questions for me - she and her class had been told by a teacher that a big spending bill was going to be passed over the weekend to "save our economy", and if it wasn't passed "it would be a disaster". I thought it interesting the school was spreading (propagating?) this propaganda.

I have been trying to explain to her in terms she can understand why our economy is in such a bad state. I told her, this bill might help or hurt the economy - I wasn't sure if anyone really knew.

Always enjoy your blog.

Paul M.

You have previously cited statistics, showing:

"Over 86 percent of the value of all stocks and mutual funds, including

pensions, was held by the top 10 percent of households. In 1998, the top

1 percent of Americans owned 47.7 percent of all stock, while the bottom

80 percent owned 4.1 percent."

Many of these stocks are overvalued today. Instead of permitting a

correction of this overvaluation, the Paulson Plan seeks to engineer a

soft landing for the wealthy, who will obviously suffer disproportionate

(to their voting strength) consequences from this correction.

The House of Representatives rejection of the Paulson Plan at least

demonstrates that Americans, intuitively, understand this formula.

I wrote to my Congressional representatives, urging them to permit

insolvent banks to fail. I hope other citizens will do likewise.

In the 1970's, as a poor law student, I switched from full-time to

part-time, and worked a day job for Crocker Bank's equipment leasing

division, as a collector and collections manager. I was back in

California for my 30-year class reunion

last month, and on my way up 280 to the Giants game that Sunday,

commented to my wife that I once worked up at the top of the hill in San

Mateo for Crocker Bank. "What's a Crocker Bank?", she replied.

I don't recall anyone getting too bent out of shape over Crocker's

demise -- they, as well as many other big financial institutions, got

carried away with Pacific Rim lending, and lost., and failed. Wells

Fargo took them over, I believe.

We have seen what happens when Third World countries take on excessive

debt, and the International Monetary Fund takes over. No social

programs, large armies and police forces and hunger in very productive

agricultural regions. Once the American future is over-mortgaged like

her residential real estate, we can stop the debate over Social

Security, health care or energy, because Job One will be debt repayment.

Just like the Third World economies I just referenced.

I have to admit that I never understood monetary policy and politics,

but I am teachable. An elementary primer I discovered this week (on a

Ron Paul oriented site), coincidentally was also a link in a Kucinich

e-mail. So I figure I must be on to something, and would like to share

it with you:

Kucinich writes:

"............

Here is a very quick explanation of the $700 billion bailout within the

context of the mechanics of our monetary and banking system:

The taxpayers loan money to the banks. But the taxpayers do not have the

money. So we have to borrow it from the banks to give it back to the

banks. But the banks do not have the money to loan to the government. So

they create it into existence (through a mechanism called fractional

reserve) and then loan it to us, at interest, so we can then give it

back to them.

Confused?

This is the system. This is the standard mechanism used to expand the

money supply on a daily basis not a special one designed only for the

"$700 billion" transaction. People will explain this to you in many

different ways, but this is what it comes down to.

The banks needed Congress' approval. Of course in this topsy turvy

world, it is the banks which set the terms of the money they are

borrowing from the taxpayers. And what do we get for this transaction?

Long term debt enslavement of our country. We get to pay back to the

banks trillions of dollars ($700 billion with compounded interest) and

the banks give us their bad debt which they cull from everywhere in the

world.

Who could turn down a deal like this? I did.

The globalization of the debt puts the United States in the position

that in order to repay the money that we borrow from the banks (for the

banks) we could be forced to accept International Monetary Fund dictates

which involve cutting health, social security benefits and all other

social spending in addition to reducing wages and exploiting our natural

resources. This inevitably leads to a loss of economic, social and

political freedom.

Under the failed $700 billion bailout plan, Wall Street's profits are

Wall Street's profits and Wall Street's losses are the taxpayers'

losses. Profits are capitalized. Losses are socialized.

We are at a teachable moment on matters of money and finance. In the

coming days and weeks, I will share with you thoughts about what can be

done to take us not just in a new direction, but in a new direction

which is just............

PS Watch the 47 minute 'Money as Debt' animated documentary in

https://video.google.com/videoplay?docid=-9050474362583451279. This is a

useful, though by no means definitive, introduction to the topic of debt

and the monetary system. Let me know what you think."

Tom N.

I stumbled across an 8/10/08 article in SFGate this morning that was supposed to be a tear-jerker about an Oakland family losing their home to foreclosure after 54 years. But then I read this part:

"Most foreclosures nowadays are homes purchased just a year or two ago with no money down. But the Gardners' home is different. Joann's parents, Johnnie Gardner, 87, and Estelle, 88, bought the two-bedroom in the Sobrante Park neighborhood in 1954 for $11,500. His salary as an electrician at the Oakland naval shipyard allowed them to make the payments.

But in recent years, Joann and her brother refinanced it several times for increasingly larger amounts.

The final refinance at the end of 2006 left the family owing $454,000. The monthly payments of $3,362 exceeded the household income of $3,144.

What happened to the money from all the refinances?

Gardner can't quite say. Some went to paying off credit cards; some was eaten up

in huge loan fees. What is clear is that the family has not made a mortgage payment

since December 2006.

Last year, a San Diego company called National Asset Direct bought the Gardners'

mortgage along with a portfolio of other distressed loans, according to Donita

Thompson, an asset manager at the company.

National Asset, which was started two years ago by a New York hedge fund,

specializes in buying distressed mortgages at a discount."

We are supposed to have sympathy backed up with tax dollars for either of these

parties???? I was so stunned at the stupidity of the Gardners that I had to watch

a video accompanying the article just to see if they sounded as stupid as their

behavior indicated. Joann Gardner didn't sound stupid; to the contrary she gave

me the impression of average or above-average intelligence.

What about the lending companies? How could they let themselves get trapped running

up the mortgage on a two-bedroom bungalow to nearly half a million where the

monthly payment was more than the entire household income?

And these are the people that Washington wants to bail out with my money? I have

two words for them: F**k off!

BTW, we have all seen multiple clips of Bush, Paulson, Bernanke, and others

over the last year saying things like "The economy is strong" or "The economic

fundamentals are sound" even when it was obvous to all serious observers that

these were lies.

There is a scene in the Oscar-winning film No Country for

Old Men where the psychopath who is doing a carjacking out on a lonely

Texas highway says to his victim, "Now hold very still" so he can place the

compressed air-powered slaughterhouse killing bolt against the man's forehead.

The man does what the psycho asks, and gets his brains blown out. This is what

Bush, Paulson, and Bernanke are asking us to do, "hold very still", while

they blow our financial brains out. But we don't have to hold still for

this -- we can run for the exits.

David S.

Shouldn't we be concerned about these financial institutions becoming too big?

Shouldn't any financial rescue include some good old fashioned, Teddy Roosevelt-style "trust-busting" ?

My response:

Trust-busting would be one approach; another would be nationalizing the biggest banks

and handing the current owners of their stock and bonds a 100% loss. Yet another

would be to let all these insolvent institutions go bankrupt, dispose of their

assets and then tightly regulate the new lenders which will inevitably arise

to fill the vacuum. I would choose the last option even though it might cause the

greatest short-term pain. Oh, and abolish the Federal Reserve, too, of course.

Albert T.

Nouriel Roubini's Global EconoMonitor

"A recent IMF study of 42 systemic banking crises across the world provides evidence

on how different crises were resolved. First of all only in 32 of the 42 cases

there was government financial intervention of any sort; in 10 cases systemic

banking crises were resolved without any government financial intervention.

Of

the 32 cases where the government recapitalized the banking system only seven

included a program of purchase of bad assets/loans (like the one proposed by the

US Treasury). In 25 other cases there was no government purchase of such toxic

assets. In 6 cases the government purchased preferred shares; in 4 cases the

government purchased common shares; in 11 cases the government purchased

subordinated debt; in 12 cases the government injected cash in the banks; in 2

cases credit was extended to the banks; and in 3 cases the government assumed

bank liabilities. Even in cases where bad assets were purchased as in Chile

dividends were suspended and all profits and recoveries had to be used to

repurchase the bad assets. Of course in most cases multiple forms of government

recapitalization of banks were used."

Roubini on the bailout very good read I think especially examples from other countries...

J.F.B.

Attached is an interesting paper from The Cato Institute written in

1999 analyzing the failure of LTCM and the Fed intervention.

(interesting how Mr. Buffett appeared in that financial crisis also.)

Failure of LTCM (Long Term Capital Management)

Don E.

"How about treating the thousands of deranged wandering our streets?"

chas., i would chastise you, but only very mildly, about throwing issues like the

peeing woman into the mix in what is otherwise always a fine try at good, sound

analytical commentary. you don't need to resort to issues that sidestep the part

of us that can weigh

information and ignite emotional flashpoints somewhere south of reason's border.

this is not good journalism.

i was a nursing shift lead in the psychiatric e.r. that serves people in your area for over a decade. the people like this woman have, indeed, fallen thru the cracks in some sense, but that does not mean they are not cared for. they are cared for as much as they will allow. having been gone from psych e.r. for over ten years i would bet there is a good chance i would know this woman by name even today. there are caring folk in the system that have a personal relationship with her and watch out for her; i guarantee you that.

mentally ill street people do not allow a lot of access; they are not easy to form relationships with and even then it will be less than stable; they will enter the system now and then when their behavior becomes too blatant or dangerous, to themselves or others, but the stay will be brief and they will soon return to their own bit of territory. seeing the cops haul away a street person is actually a good sign. it means they will go to psych e.r. and be seen too to some extent: fed, cleaned up, re clothed. the only countries i have traveled in that did not have street people were tightly controlled police states.

i would not claim that your local psych e.r. is heaven, but the majority of folk who work there can only do so if they have a basic core of kindness and empathy to draw upon. i will certainly agree that the bailout money can find better places to go than the pockets of bankers'. the street people exist in a sort of warped parallel universe that can be very harsh and cruel; they may be both right beside you and too far away to reach. they need to be dealt with as kindly as is possible by everyone who comes in contact with them - it is not always apparent what may even constitute kindness. i fear more and more of our neighbors will join this parade. not thru choice as the mentally ill on the street do. i would not lock up and "treat" these aberrant folk; however misguided we think their choices they are manifesting free choice in how they live. we cannot mandate medication; we can only try to nurture the husks of those who were once much like us as we meet them in passing.

the seeds have been planted and we may now expect a bumper crop of displaced people;

some will become mentally ill in the stress, and many will become angry; we will

have to deal with them face-to-face more and more - hopefully they won't be armed.

even were the hundreds of billions suddenly lavished upon the social net instead

of on wall st. the authorities would still not be able to handle all the misery

that is coming. we have to pitch in and do it ourselves to whatever extent we

are able. i always found a nurse's strongest suit to be, not technical skill,

but sheer kindness.

HUGE GIANT BIG FAT DISCLAIMER: Nothing on this site should be construed as investment advice

or guidance. It is not intended as investment advice or guidance, nor is it offered as such.

It is solely the opinion of the writer, who is NOT an investment counselor/professional.

All the content of this website is solely an expression of his personal interests and is

posted as free-of-charge opinion and commentary. If you seek investment advice, consult

a registered, qualified investment counselor (As with any other professional service, confirm their

track record and referrals).

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

--An anonymous comment about CHS posted on another blog.

NOTE: contributions are acknowledged in the order received. Your name and email

remain confidential and will not be given to any other individual, company or agency.

Thank you, Kevin L. ($25), for your extremely generous donation

to this site. I am greatly honored by your ongoing support and readership.

Or send him coins, stamps or quatloos via mail--please

request P.O. Box address.

Your readership is greatly appreciated with or without a donation.

For more on this subject and a wide array of other topics, please visit

my weblog.

All content, HTML coding, format design, design elements and images copyright ©

2008 Charles Hugh Smith, All rights

reserved in all media, unless otherwise credited or noted.

I would be honored if you linked this wEssay to your site, or printed a copy for your own use.