|

|

|

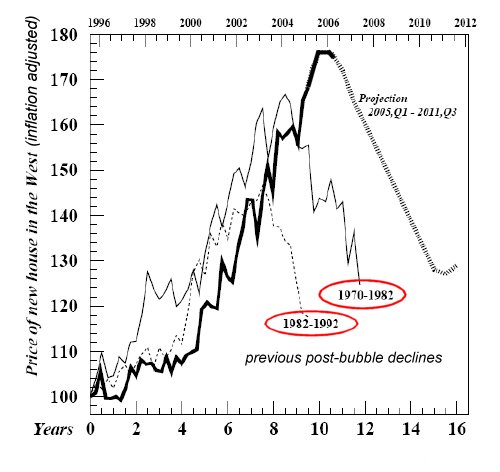

The Grand Summary: Our Empire of Debt Is Collapsing (July 28, 2008) Every once in awhile it pays to stand back and locate one's position in reality, by dead reckoning if no better tools are at hand. With all the financial legerdemain in our system--bogus unemployment and CPI numbers, Level 3 assets held safely off balance sheet, and innumerable other financial rats scurrying for cover--we have no choice but dead reckoning. And by my reckoning, our financial system is dead. Right now, Bernanke and Paulson and Congress and the rest of the power elite have the shock paddles frantically pressed to the chest of the American financial system, hitting the erratic heart of our Debt Empire with shock after shock, hoping and praying the debt bubble of the past 25 years can somehow be extended. Alas, the patient is already dead. But with reporters' noses pressed against the window a few feet away, the stalwart crew around the corpse is making a heroic show of lying: "The patient is stabilizing," "the patient is recovering nicely," and so on, and by artificially stimulating the heart to keep producing a weak but visible pulse for all to see. But rather than be reassured, we are disgusted by the lies, for we have seen the patient bloat up and sicken and then weaken unto death for years. Rather than try to describe the Empire's plight in words alone, here are some graphic illustrations for your review. Let's start with the housing bubble:

The bubble has popped, never to rise again, for several simple reasons. Most profoundly, risk has re-entered the equation. U.S. lenders were able to originate trillions in mortgages and then pass them off to Fannie Mae and Freddie Mac (who own some $6 trillion in rapidly depreciating mortgage assets) and non-U.S. investors who unfortunately believed the AAA ratings on garbage mortgage-backed securities happily bundled at immense profit by U.S. investment banks.

Game over, the debt machine is broken, patient has expired, end of story, etc. As the FDIC chart above reveals, virtually everyone in America above the poverty line bought a house in the bubble, and by their conservative estimate, 10% of recent buyers were simply unqualified to buy a house just based on income. Since there are 75 million homeowning households in the U.S., we can infer that 7.5 million homes will transfer from never-should-have-qualified buyers back to unscrupulous/ incompetent lenders. This gives us some context when we read about 1.2 million foreclosures (or whatever the number is proported to be--we all know lenders are hiding distressed mortgages left and right): only 6 million to go. And let's be clear about one thing: the entire bailout is being sold as a way to keep insolvent buyers in their homes by lowering the interest rates and loan amounts. Fair enough in theory, but if someone paid double what the house was worth and leveraged their cash 1,000 to one and only qualified for an interest-only super-low teaser-rate adjustable mortgage, then they can't make the payment regardless of what tweaks are made to the loan parameters. Next, let's recall the precarious source of the housing bubble: a zero-savings society and massive derivatives and debt. Rather than save up and then lend the accumulated capital as per the classic capitalist model, banks generated new debt with magic.

With only 1% required for reserves, $1 million became the foundation for $100 million in new mortgages, which were quickly sold to investment bankers who sold the debt and then made even more money writing derivatives based on that "risk-free" (i.e. rated AAA by the ratings agencies) debt.

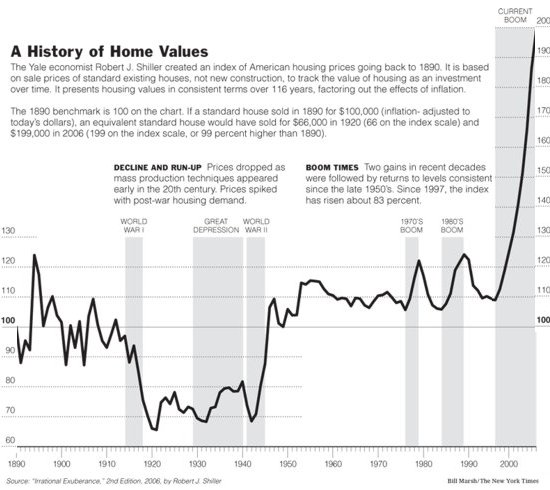

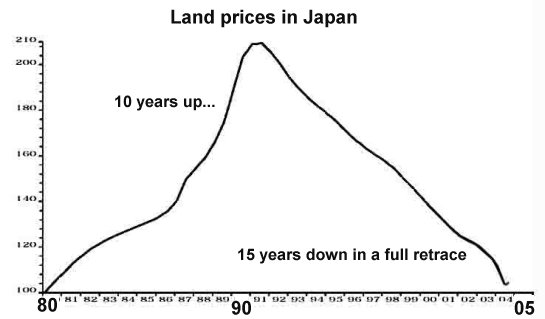

Let's also not forget that the stock market is a bubble, too, as this long-term chart clearly reveals:

Here is the once-mighty U.S. dollar, gutted by low interest rates, depreciating assets and all the other ills of an Empire of Debt:

Then there's our stunning dependence on overseas investors to soak up all our deficit-spending/debt via purchasing U.S. bonds:

It's no surprise that consumer spending has risen from a long-term average of about 67% of GDP to 72%--we borrowed $4.2 trillion in the peak years of the housing bubble and blew it on a free-spending consumer binge. (Source: Tough Love for the U.S. Economy (BusinessWeek) Needless to say, the deflation of the housing bubble and the decline in stocks has removed our ability to borrow and spend another $4-5 trillion. With that well gone dry, exactly how can consumer spending continue at this pace? Simple answer: it cannot. As if that wasn't enough, we're facing unprecedented demographic and pension/ medical care cost expansion. Here is a chart of workers-to-retirees which is based on exceedingly rosy projections of continued strong growth in productivity and employment.

It simply isn't possible to tax three workers enough to pay for one retiree in a system which charges Medicare $100,000+ for a few days in a hospital and an operation and a test or two. (This was the bill for a friend of mine's father for gallstone removal--which didn't even successfully remove the gallstones! The elderly gent got better on his own despite the "care" and eventually demanded to go home. Taxpayers picked up the $100K+ tab for virtually nothing but aggravation and a single prescription for antibiotics which could have been administered at home.) As the Empire of Debt collapses, so too will employment based on ever-more debt and borrowing, and it is easy to see the worker-retiree ratio dropping to 2-to-1 or even lower. That simply isn't sustainable. And even as healthcare costs skyrocket, we as a nation seem to be acquiring ever more chronic health problems, many related to poor diet and lifestyle choices:

Another trend is weighing on every debt-based economy: the inexorable rise of oil as Peak Oil supply and cost restraints become undeniable:

How about those limitless shale oil fields? Have you seen any photos of the landscape this leaves behind? How about how much natural gas must be burned to extract the oily goo from the rocks or sand? How about $80/barrel costs for starters, and refining, transport, overhead and profit added on to that? How about ever-hgher costs as all the energy required to make this stuff goes ever higher? Installing a wind-farm or solar collection facility isn't free; where are we, debt-laden and imprisoned by past borrowing, going to locate the $5-10 trillion we need to build an entirely new energy infrastructure? We are in the midst of a long period of below-average returns which will eventually return us to average returns--in, say, 10-15 years.

Three final charts: disposable personal income, corporate profits and bonds.

This has been a favorite chart of mine, for it illustrates how the low interest rates in the U.S. have been entirely dependent on the willingness of the Chinese banks and other non-U.S. entities (Japan and the Gulf Oil states, among others) to buy unprecendented trillions of U.S. debt.

As the dollar has tanked, these owners of U.S. debt have suffered stupendous losses; yet they've kept on buying for fear that if they stop funding the Empire of Debt their own sales to the Empire will decline. Yet when does this propping-up of the Empire become "good money tossed in after bad"? When does the U.S. contraction of consumer spending start removing some of those surplus dollars from their hands? When does domestic political pressure build to invest some of those trillions in their own nations rather than toss them in the garbage heap of U.S. debt? Bond trends are not sharply delineated like stock market trends. They are slow, saucer-shaped reversals which then endure for decades. The Empire of Debt's most reliable prop has been low interest rates, i.e. the willingness of non-U.S. players to invest their surplus dollars in U.S. debt for absurdly low rates of return. (Recall the inflation rate in Gulf Oil states is 11% and climbing. How much sense does it make to buy U.S. debt which pays 4% and which declines along with the dollar?)

I believe the evidence is already plentiful that the trend of low interest rates

has reversed and will rise for 15-24 years. (The average bond/rate cycle runs

from 16-27 years in length.) Even as the Fed desperately slashed the Fed funds rate,

mortgage rates have risen. Why?

The Empire of Debt is expiring, for a number of profound, difficult to reverse

trends:

1. interest rates are now in a 20-year uptrend; cheap borrowing is gone

2. Peak oil will raise the price of energy, regardless of its source, creating

a global tax on consumption

3. health costs continue to skyrocket as chronic health issues rise and the cost

and range of available treatments expands

4. pension and entitlement programs designed for 10 workers for every retiree

are now facing 3-to-1 or even lower worker-retiree ratios

5. the U.S. current account deficit (trade deficit) is unsustainable, as is

its debt-swollen domestic consumer spending

6. stagnant/declining wages and rising unemployment are the inevitable result

of reduced borrowing/spending by consumers and government alike.

I'm not trying to be negative: what's negative about facing reality? What's negative

and destructive is covering up reality with obfuscations, lies and fairy tales.

There is a way out, and it's called replacing profligate borrowing with savings,

and replacing mal-investment in unproductive assets (financial legerdemain and

surplus housing) with productive investments (alternative energy, society-wide

energy efficiency, true healthcare as opposed to our current "sickcare", etc.)

Political Wil' Discovers Fools Gold

I will be the last to tell you that government, just like the financial sector, is

not mis-allocating resources. It most certainly is. And regulatory agencies

like mine are no exception.

But the solution to over-allocating resources in government is somewhat more

complex than just reducing entitlements, and my role in particular is a good example.

My agency is charged with protecting and enhancing natural resources. However,

environmental laws are not regarded as 'real laws' by the regulated community.

People of means are fond of saying, I do not get permits, I hire lawyers.

Three articles by Charles Hugh Smith this year have garnered my attention. The first

was

When Belief in the System Fades which struck a harmonized note for me as a former

officer in the military reserve who had served in Iraq and recently resigned my

commission.

The next two were The Art of Survival, Taoism and the Warring States

and Where the Rubber Meets

the Road. I had really liked the Survival + theme in both articles with the

emphasis on building human relationships within a small community and strengthening

personal skills over the retreat to the isolated bunker filled with gadgets and guns.

Thank you, Peter N. ($50), for your outrageously generous

donation to this site and for your many intellectual contributions.

I am greatly honored by your support and readership.

|

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||

By any possible measure, the housing bubble reached unprecedented heights--

all based on incredibly leveraged, incredibly easy, incredibly low-rate and

incredibly risk-obscured debt.

By any possible measure, the housing bubble reached unprecedented heights--

all based on incredibly leveraged, incredibly easy, incredibly low-rate and

incredibly risk-obscured debt.

Once burned, twice shy. Well over $1 trillion in bundled mortgages were sold

in 2007; for the first 6 months of 2008, a paltry $48 billion found buyers. In other

words, the market for U.S. mortgages has fallen to near-zero. Nobody's dumb enough

to trust the ratings agencies and investment banks, and nobody's dumb enough to

"catch the falling knife," i.e. buy mortgages on properties which are in a free-fall.

Once burned, twice shy. Well over $1 trillion in bundled mortgages were sold

in 2007; for the first 6 months of 2008, a paltry $48 billion found buyers. In other

words, the market for U.S. mortgages has fallen to near-zero. Nobody's dumb enough

to trust the ratings agencies and investment banks, and nobody's dumb enough to

"catch the falling knife," i.e. buy mortgages on properties which are in a free-fall.

And as we borrow freely from the rest of the world, soaking up some 85%

of all global savings with our riotous borrow-and-spend lifestyles, guess what:

we run stupendous trade deficits, buying more than we sell to the tune of $750 -

$800 billion a year.

And as we borrow freely from the rest of the world, soaking up some 85%

of all global savings with our riotous borrow-and-spend lifestyles, guess what:

we run stupendous trade deficits, buying more than we sell to the tune of $750 -

$800 billion a year.

In basic terms, oil is becoming ever costlier by every measure: in any currency,

and even in gold. This makes perfect supply-demand sense: as demand rises, it

exceeds the supply of cheap, easy to recover oil and prices rise. Once the

easy oil is depleted (which is happening now), then the oil that's left will be

very costly to extract and process. Does the poorly-informed pundit demanding

offshore drilling have any idea of how much it costs to drill down two miles or

more from an offshore rig?

In basic terms, oil is becoming ever costlier by every measure: in any currency,

and even in gold. This makes perfect supply-demand sense: as demand rises, it

exceeds the supply of cheap, easy to recover oil and prices rise. Once the

easy oil is depleted (which is happening now), then the oil that's left will be

very costly to extract and process. Does the poorly-informed pundit demanding

offshore drilling have any idea of how much it costs to drill down two miles or

more from an offshore rig?

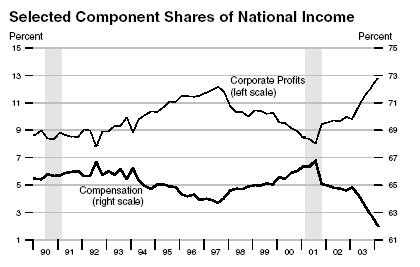

Even as all asset classes have risen in unison

(commodities, gold,stocks, real estate and bonds all rose together during the

housing bubble)--another unprecedented trend, to be sure--wages have remained

static or dropped in terms of purchasing power. Meanwhile, corporate profits

have zoomed to unprecedented levels: a staggering 13% of U.S. GDP is corporate profits.

Even as all asset classes have risen in unison

(commodities, gold,stocks, real estate and bonds all rose together during the

housing bubble)--another unprecedented trend, to be sure--wages have remained

static or dropped in terms of purchasing power. Meanwhile, corporate profits

have zoomed to unprecedented levels: a staggering 13% of U.S. GDP is corporate profits.